American Credit Scores Hit a New High

American Credit Scores Hit a New High

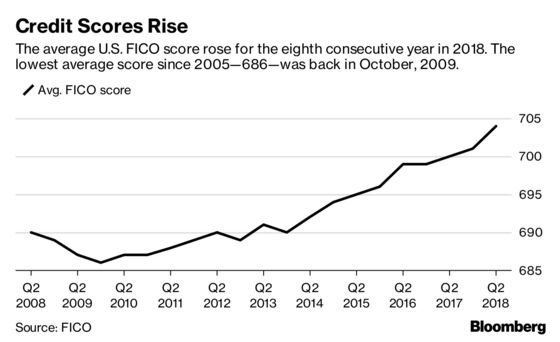

(Bloomberg) -- Almost a decade after the average FICO score hit a low of 686 in the aftermath of the Great Recession, the number is at its highest point ever, 704. The new record marks an eight-year streak of increases, trailing America’s recovery from its financial near-death experience.

Fueling the rise is the fact that fewer consumers have truly horrible scores (less than 550) that could drag the average down. In the last year, the percentage of Americans with one or more collection accounts on their file has fallen to 23 percent from 25.8 percent. Since payment history makes up 35 percent of a FICO score, the drop in delinquencies has more people moving on up into the 650 to 699 range.

At the other end of the spectrum, more Americans have ascended to the “super-prime” club. Consumers with FICO scores of 800 or more are almost 22 percent of the FICO score population, up from 20.6 percent a year ago. That same reading was closer to 18 percent during the worst of the financial crisis, said Ethan Dornhelm, vice president of scores and analytics at FICO.

A good credit score can save a consumer a lot of money, earning them lower interest rates on loans. The range for FICO, and of rival product VantageScore, is 350 to 850. Dornhelm said the key thresholds are about 680 and 620—minimum scores required by the mortgage industry (to get a good rate) and government-sponsored lenders (Fannie Mae and Freddie Mac), respectively.

Demographically, the new credit score high is the product of conscientious baby boomers and Generation Xers. The 18-to-29-year-old crowd has an average score of 659; Americans in their thirties come in at 677; those in their forties are at 690; while fiftysomethings reached 713. Americans in their sixties, meanwhile, are flying high with an average FICO score of 747.

To be fair, scores for all generations have risen and older people have a longer history on which FICO can base their number. Moreover, people in their twenties and thirties are often buried under a mountain of debt, thanks to the college loan industrial complex. On this last point, it’s worth noting that fintech firm Lending Tree recently reported that America’s $1.5 trillion-plus student debt load is second only to housing-related loans.

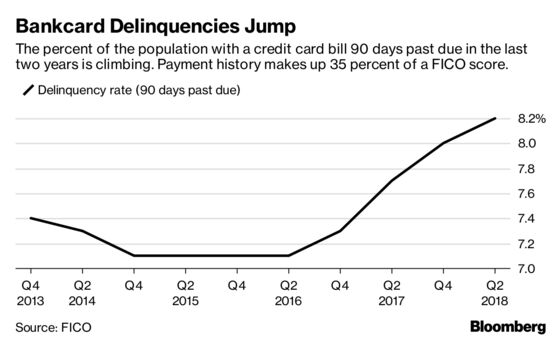

The FICO report, published Monday, had one dark spot. The percentage of the company’s score population with bankcard accounts more than 90 days past due is 8.2 percent, up from 7.7 percent in April 2017. But even this, Dornhelm said, may be a consequence of the overall upswing. “Some of that may be a reflection that lenders started loosening underwriting criteria a bit, so [they] are bringing in a near-prime population that is more likely to default,” said Dornhelm. He added that banks likely baked that into their pricing.

The new record comes on the heels of other signs consumers are finally shrugging off a recession hangover, despite stubbornly stagnant wages that haven’t matched mushrooming corporate revenue. Consumer confidence is at its loftiest level in 17 years, unemployment is near a 50-year low and household wealth—fueled largely by those who own stocks or property—rose by $2.19 trillion to hit a record $106.9 trillion in the second quarter.

That’s fueling household spending, which accounts for roughly 70 percent of the U.S. economy. Consulting firm Deloitte LLP anticipates a record holiday shopping season, forecasting sales of about $1.1 trillion from November through January.

Which brings us to some sobering figures that may augur a brand-new hangover down the line.

- Americans are borrowing more than ever, with mortgage balances growing at a rate that Lending Tree warns is in line with pre-housing bubble levels.

- The ratio of personal savings to disposable personal income is falling, from 7.4 percent in February to 6.7 percent in June.

- Auto lending, widely feared to be the next subprime lending crisis, has climbed steadily since the Great Recession ended, and consumers are taking longer to repay those loans.

- Total household debt hit a record $13.3 trillion in the second quarter, according to the Federal Reserve Bank of New York.

In fact, this marks the sixteenth consecutive quarter household debt rose, breaking the previous record of $12.68 trillion. The old record, coincidentally, was reached exactly 10 years ago, during that decidedly unpleasant third quarter of 2008.

To contact the editor responsible for this story: David Rovella at drovella@bloomberg.net

©2018 Bloomberg L.P.