America's Libor Alternative Is Gaining Traction on Wall Street

America's Libor Alternative Is Gaining Traction on Wall Street

(Bloomberg) -- After some early struggles, America’s Libor alternative appears to be finding its footing.

Since the debut of the Secured Overnight Financing Rate almost six months ago, futures have launched in Chicago, swaps are being cleared in London and about half-a-dozen issuers have sold debt linked to the nascent benchmark. Measured against the Alternative Reference Rates Committee’s transition plan, efforts to develop SOFR as a viable replacement for the scandal-tainted London interbank offered rate appear to be proceeding ahead of schedule.

That’s not to say it doesn’t have a long way to go. Volumes and open interest in derivatives products indicate the market is still highly illiquid. And firms remain hesitant to commit resources to SOFR when there’s a chance Libor’s administrator and the panel banks that determine its setting could keep it alive past 2021, when global regulators intend to sound its death knell. Yet it’s a far cry from April, when two weeks after SOFR’s introduction the Federal Reserve Bank of New York disclosed it had made errors calculating the rate, an inauspicious start for a benchmark racing against time to gain traction.

“It’s encouraging as the progress has been faster than I had anticipated, especially the number of SOFR floater issues that have come to market,” said Mark Cabana, head of U.S. short-term rates strategy at Bank of America Corp. in New York. “What is less encouraging has been the still very limited liquidity in the derivatives market.”

Here’s the state of play as SOFR’s quest for credibility continues:

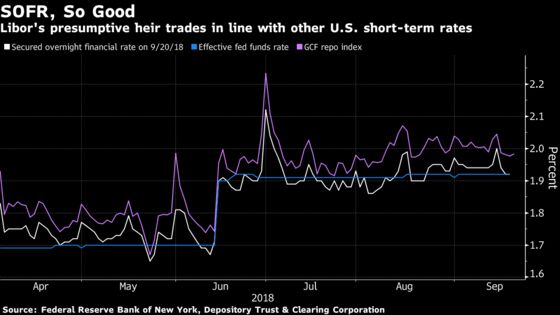

The Benchmark

Since the initial miscalculations, SOFR has largely printed in line with expectations. It sets daily based on overnight repurchase agreement transactions secured by Treasuries. So far, it’s been below the GCF repo rate and close to the effective fed funds rate, the Fed’s target benchmark. Repo transaction volumes underlying SOFR remain robust, averaging about $779 billion daily since the benchmark’s launch, New York Fed data show.

Yet one concern is that SOFR has proven more volatile than Libor, given that it’s more susceptible to price swings tied to Treasury-bill issuance, as well as month- and quarter-end supply variations.

SOFR jumped five basis points on Sept. 17 as the Treasury’s coupon auction settlements pushed underlying repo rates higher. At the end of June, the reference rate spiked 19 basis points -- to 2.12 percent -- as dealers curtailed lending activity in the repo market to shore up balance sheets. Three-month dollar Libor, in contrast, has only moved by more than 2 basis points once since SOFR’s debut.

SOFR set at 1.92 percent Friday, unchanged from the previous session.

Futures & Swaps

While trading in futures tied to SOFR has steadily increased since their debut in May, volumes and open interest remain well below alternative interest-rate contracts. Average daily volume for SOFR futures was 6,092 contracts in August, CME Group Inc. data show, a fraction of the 159,071 seen in fed funds futures. And open interest of 30,181 contracts is less than 2 percent of that in fed funds.

Trading in SOFR-linked swaps also remains tepid. Since LCH Ltd. began clearing the first SOFR swaps in July, only about 20 trades have occurred, most no longer than 1- or 2-years. The majority of transactions have been either SOFR-fed funds basis swaps, overnight indexed swaps or SOFR-Libor basis swaps, according to JPMorgan Chase & Co. strategists Joshua Younger and Munier Salem, citing Swaps Data Repository activity.

Still, ARRC Chair Sandra O’Connor said there’s sufficient trading volume for the committee to establish an indicative term structure, which should help the market transition to the new reference rate.

“We already have enough depth to produce the indicative” rate, O’Connor said.

Credit Markets

Issuers running the gamut from government agencies and supranational institutions to banks and municipalities have issued more than $9 billion of debt tied to the new benchmark over the past two months.

Date | Issuer | Size | Tenor | Price |

| July 26 | Fannie Mae | $2.5b, $2b, $1.5b | 6, 12, 18 months | SOFR +8, +12, +16 |

| Aug. 14 | World Bank | $1b | 2 years | SOFR +22 |

| Aug. 20 | Credit Suisse | $100m | 6 months | SOFR +35 |

| Aug. 22 | Sheffield (Barclays) | $525m | 3 months | SOFR +35 |

| Aug. 30 | MetLife | $1b | 2 years | SOFR +57 |

| Sept. 18 | Wells Fargo | $1b | 1.5 years | SOFR +48 |

| Sept. 20 | Triborough Bridge & Tunnel Authority | $107.3m | 13.5 yrs, with man. 1 yr tender | SOFR *(0.67) +43 |

| Sept. 20 | Wells Fargo | $125m | 1 year | SOFR +35 |

The deals have priced cheap relative to where Libor-equivalent financing would have been, given the relative lack of secondary-market trading for SOFR-linked products and increased liquidity risk, Bank of America’s Cabana said.

“Some issuers have done pretty well by adopting SOFR, but let’s not get over our skis here,” said Jerome Schneider, head of the short-term and funding desk at Pacific Investment Management Co. “There’s a larger investor base that has to be convinced that SOFR can be used for longer-dated issues, which will ultimately determine the level of success.”

Future Fed Benchmark?

Ultimately, the entity that may provide the biggest push to develop a robust SOFR market is the Fed, especially should it decide to adopt the benchmark as its target rate instead of fed funds.

Cabana sees it as a possibility as officials revisit their policy framework. Activity in the fed funds market has dwindled since the financial crisis, while repo trading underpinning SOFR is deeper, has a broader set of market participants, and is more resilient to regulatory changes, he said.

“All of those are very strong cases for the Fed to consider SOFR,” Cabana said. “It would help facilitate the transition away from Libor.”

--With assistance from Danielle Moran.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby, Mark Tannenbaum

©2018 Bloomberg L.P.