Agency Mortgages Face Uphill Battle in 2019 Without Fed Support

Agency Mortgages Face Uphill Battle in 2019 Without Fed Support

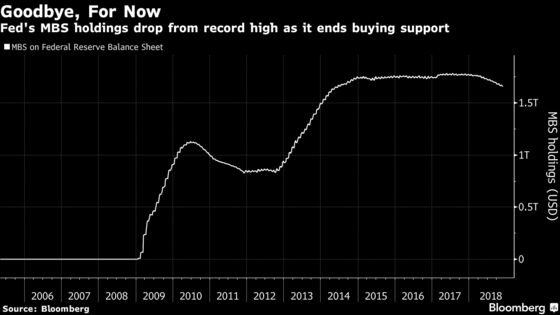

(Bloomberg) -- Agency mortgage-backed securities will need to overcome a litany of challenges next year, including the absence of Federal Reserve support, the introduction of a Uniform MBS and concerns about demand, according to a roundup of 2019 outlooks.

Wells Fargo MBS strategists led by Vipul Jain expect challenges in 2019 to be even "more daunting" than this year as net supply is likely to remain close to 2018’s projected $250 billion. Fed balance sheet runoff will add another $191 billion.

- TBA coupon rolls are likely to come under pressure as the absence of Fed buying will decrease the quality of bonds delivered to investors

- Uniform MBS, set to be introduced in June, will increase the tradable float and reduce the scarcity value for coupons across the 15-year stack

- Money managers will purchase about $266 billion as they "have largely shed their predominantly negative disposition toward MBS from the perspective of valuations through the course of this year"

- Expect "10 basis points of spread widening on an OAS basis from current levels. Carry for mortgages can offset a lot of this widening"

Morgan Stanley’s MBS strategist team led by Jay Bacow sees a dip in agency MBS net issuance to $250 billion in 2019 from $275 billion this year, with the question of demand more pertinent to the Ginnie Mae side of the ledger as banks have less regulatory need to own HQLA level 1 assets.

- Fed MBS balance sheet runoff to rise to $180 billion from $150 billion

- "Expect agency MBS to have slightly positive excess returns vs Treasuries and outperform corporate credit as net supply will continue to be high but spreads are near local wides"

JPMorgan MBS strategists led by Matthew Jozoff project agency MBS net issuance will drop to $225 billion from an expected $280 billion this year. Runoff from the Fed’s balance sheet will increase to $185 billion from about $150 billion.

- Look for option-adjusted spreads to tighten by 10 basis points in 2019, mainly due to money manager sponsorship

Nomura’s MBS strategist team led by Dhivya Krishna writes that "from a longer-term perspective, 2019’s supply-demand outlook should be very similar to 2018’s" and money managers need to add between $245 and $250 billion to balance the technicals.

- Net supply of $235 billion combined with Fed runoff of $200 billion.

- After this year’s widening, forecast any potential widening from current levels to be small

Citigroup’s MBS strategist team led by Ankur Mehta projects $230 billion in agency MBS net supply and Fed balance sheet runoff of about $173 billion.

- The net supply component should display a seasonal pattern, with a peak of about $30 billion a month seen in August and September with the remainder of the year seeing less than $20 billion a month

- Look for money managers to add about $150 billion to $200 billion next year

To contact the reporter on this story: Christopher Maloney in New York at cmaloney16@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Adam Cataldo, Rizal Tupaz

©2018 Bloomberg L.P.