Fed’s Bombast Prompts Pimco to Call on Bigger ECB QE Blowout

Fed’s Bombast Prompts Pimco to Call on Bigger ECB QE Blowout

(Bloomberg) -- In the battle of central-bank stimulus bazookas, the Federal Reserve is winning out.

The promise of unlimited quantitative easing spurred U.S. Treasuries higher for a third day Monday. Across the Atlantic some analysts are already calling for the European Central Bank to do more -- either by increasing its 750-billion euro ($811 billion) package or introducing other measures to help support the market as the economy spirals.

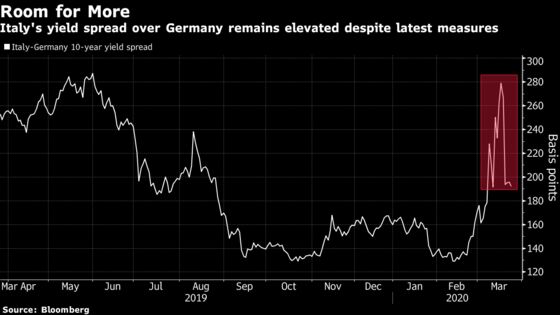

Those could range from additional QE with more assets bought, including exchange-traded funds. A measure introduced by ex-President Mario Draghi in 2012, but never used -- outright monetary transactions -- could also be used to support the most vulnerable markets, such as Italy. The policy allows the ECB to buy an unlimited amount of a nation’s bonds in return for economic reforms.

The scale of the challenge is huge. Goldman Sachs said in a note on Tuesday that it sees an economic contraction bigger than any since the formation of the euro area. They see the economy contracting 9% this year.

Here’s some views on what could be done:

Pimco: (Policy responses would normally be eye-popping)

- “These packages would have made most people’s eyes pop out in normal times,” writes money manager Nicola Mai, referring to recent fiscal and monetary packages

- “But in these times are they enough to avert a severe recession? The way we see it, they are a step in the right direction, but probably not enough”

- Worsening fiscal balances are an inevitable consequence of the crisis, and countries should have the space and freedom to respond

- An even more unconditional commitment to support sovereigns (via a sort of European sovereign yield/spread curve control) might prove of the essence, he writes, referring to possible measures the ECB could take

- “More activism in the bond-buying program could be useful, with the central bank forcefully demonstrating that it won’t allow any question marks about its ‘lender of last resort’ role to resurface”

- The ECB could also get even more creative and expand the range of assets it buys, by including for example equities, wholesale loans and banks’ bonds

ING: (Italy good OMT candidate)

- “It’s never been used before, but it’s there; unlimited front-end buying (OMT),” write strategists led by Antoine Bouvet

- They called the policy “something for the ECB to bat back to the Fed’s unlimited QE stroke,” adding that Italy is “as good a candidate as any”

- “This would open up the possibility of unlimited ECB purchases of Italian government bonds with up to three-year maturity”

Rabobank: (ESM could reduce Italy’s stigma)

- “The reality is that the Fed is now providing backstops for pretty much everything save for President Trump’s beloved Dow Jones index,” writes analyst Bas van Geffen

- The Fed’s Primary Market Corporate Credit Facility program allows the purchace of corporate bonds in the primary market, while the ECB can only do so in the secondary market

- The Fed will provide bridge financing of up to four years directly to eligible corporates

- “Despite a relatively modest size to begin with, that is arguably the ECB’s TLTRO program (without collateral?) on steroids: by bypassing the banking sector, banks’ balance sheet and regulatory requirements are no longer constraints”

- Offering such a credit line to all euro-zone members through the European Stability Mechanism could remove the stigma Italy faces

Mizuho: (ECB should buy ETFs)

- “Fed has done QE and credit easing in the right way -- one which will allow markets to understand that the Fed is always there,” says head of European rates strategy Peter Chatwell

- “QE unlimited is a stronger message than PEPP”

“The Fed’s credit easing, including ETFs, is more efficient than the Corporate Sector Purchase Program. The ECB needs to buy investment-grade corporate ETFs rather than just the bonds”

- “If the economic shutdowns need to be longer, then the fiscal packages will need to grow, hence the QE will need to grow”

Robeco: (Enough already?)

- “After misfiring initially at their scheduled ECB meeting, the ECB’s 750-billion euro PEPP and the hints of activating the OMT now looks to be the right sort of response for markets, hopefully preventing a 2011-type periphery sovereign crisis,” write strategists including Victor Verberk

- “The longer-term impact of ECB measures may be the intertwining of sovereigns and banks once again -- the so-called sovereign-bank nexus”

- “The cost of extraordinary support today will likely emerge tomorrow in the form of more directed lending and increased holdings of sovereign bonds”

©2020 Bloomberg L.P.