Aberdeen Eyes Unrated Aussie Bonds Amid a Dearth of Issuance

Aberdeen Eyes Unrated Aussie Bonds Amid a Dearth of Issuance

(Bloomberg) -- Aberdeen Standard Investments is interested in unrated corporate debt in Australia as bond issuance has dwindled this year and yields have plunged.

Debt that isn’t graded by rating firms has featured more prominently on fund managers’ radar screens in the last six to 12 months, according to Matthew Macreadie, a Sydney-based senior investment manager of fixed income at Aberdeen Standard, which oversees $643.3 billion. Many more investor mandates are now allowing fund managers to invest in such notes as the Australian credit market looks “fairly valued to expensive,” he said.

“We need to have flexibility within our funds to allow a portion in unrated issuance to help with the lack of opportunities that we are seeing in the Australian bond market,” Macreadie said in an interview. “I’m on the lookout opportunistically for names where some credit risk may be mispriced.”

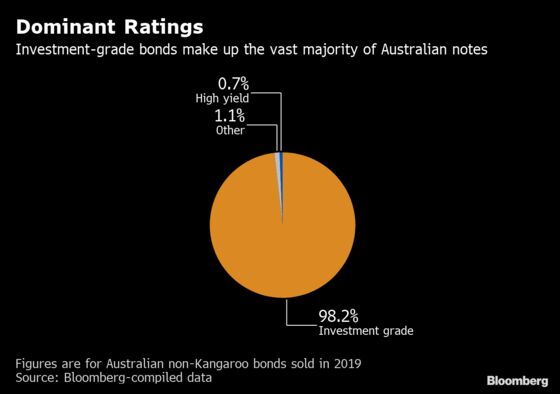

Australian government bond yields have plunged as the central bank cut interest rates to a record-low 1.25% this week to support job growth. The supply of corporate notes in the country is also tight because fewer bonds are maturing this year and so companies don’t need to refinance debt, and also because firms spent less in the lead-up to a federal election that was held in May. Australian non-Kangaroo bond sales have dropped 20% so far this year, according to Bloomberg-compiled data.

That’s forced managers like Aberdeen to look for more niche areas such as unrated debt. Some companies choose not to have a credit score because it’s expensive to get and maintain, especially if it’s a one-off issue, Macreadie said.

6-9% Yields

Among non-rated debt that Aberdeen is looking at is NEXTDC Ltd., a developer of data centers, he said. Bonds of unrated issuers typically yield from 6% to 9%, Macreadie said.

There are risks, though. Unrated corporate notes are more vulnerable to an increase in interest rates and Aberdeen wouldn’t hold more than 10% of a fund’s net asset value in them, he said.

“Everyone is reaching and grabbing for that extra spread,” with Australian and U.S. 10-year yields so low, he said. “There is a bit of a sweet spot in the market for these unrated borrowers now while interest rates are low, but as they rise, they are not going to be able to get the same level of demand.’’

More broadly, Aberdeen is overweight in financial firms’ debt in Australia, including the major banks, as it doesn’t expect a big property-market downturn. It also likes toll roads, airports and ports because of attractive cash flows.

“While there’s been volatility, we haven’t seen credit spreads widen to a point where we are worried about an extreme sell-off in credit,” Macreadie said. “It hasn’t gotten to that point where we think we should be short credit and generally it pays over the long run to have an overweight to credit.”

To contact the reporter on this story: Andreea Papuc in Sydney at apapuc1@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, ;Andrew Monahan at amonahan@bloomberg.net, Ken McCallum, Finbarr Flynn

©2019 Bloomberg L.P.