Big Pharma Has to Bet Big on M&A. Investors Don’t.

Big Pharma Has to Bet Big on M&A. Investors Don’t.

(Bloomberg Opinion) -- AbbVie Inc.’s $63 billion purchase of Botox maker Allergan Inc. is the third super-sized drug deal announced in the past 14 months, and the second just this year after Bristol-Myers’s Squibb Co.’s even bigger $74 billion purchase of Celgene Corp. These huge combinations are no fluke: In the last decade, the biopharmaceutical industry has pursued more $40 billion-plus transactions than any other sector, according to data compiled by Bloomberg.

These big deals happen for a reason. Drug development is difficult, unpredictable and time consuming; even when the billions pharmaceutical companies spend on R&D or strategic purchases and partnerships bear fruit with top-sellers, those blockbusters still face the prospect of expiring patents and an eventual decline in sales. That pressures drugmakers into bigger acquisitions, in spite of their mixed track record and inherently risky and complicated nature. In AbbVie's case, the company needs to find a replacement for its $19 billion-a-year arthritis drug Humira, while Bristol-Myers is too dependent on two key drugs.

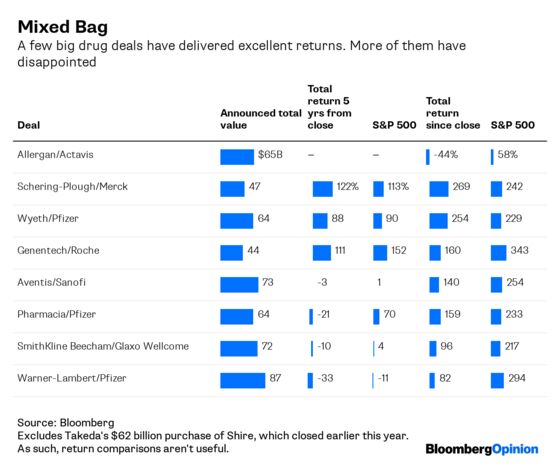

If pharma giants can’t keep themselves from making big and risky M&A bets, that doesn’t mean investors have to follow suit, or that they’d get much of an edge from doing so. While big pharma deals have resulted in longer-term gains for very patient investors in many cases, the returns don’t look as good compared to the broader market. Of the eight biopharma deals worth more than $40 billion that closed in the last 20 years, only one delivered better returns than the S&P 500 five years after it closed: Merck & Co.’s $47 billion acquisition of Schering-Plough Corp. in 2009 :

That deal is arguably something of an accidental winner. Long-term success didn’t come from any of the products Merck targeted in the merger; instead, an afterthought of an antibody that was initially set to be sold off became Keytruda, a cancer drug that’s projected to generate $15 billion in sales in 2021.

Investors shouldn’t count on buried pipeline treasure to bail out the latest crop of big drug acquisitions. A better bet? Try an index fund.

Not included in the group is Takeda Pharmaceutical Co.'s $62 billion purchase of Shire Plc, which closed in January, making return comparisons lessuseful.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.