A Rally ‘on Steroids’ Falters in Europe’s Most Indebted Markets

A Rally ‘on Steroids’ Falters in Europe’s Most Indebted Markets

(Bloomberg) -- Investors savoring a rally in Europe’s peripheral bond markets this year just got a taste of how vulnerable these heavily-indebted economies are.

Italian debt ended a streak of record-breaking gains Thursday as the country, similar to others in Europe, faced a resurgence of coronavirus cases, increasing the prospect of fresh lockdowns and more economic woe.

The sudden turn in sentiment was a rude awakening for investors who, egged on by a torrent of central bank liquidity and a historic fiscal backstop from Europe’s richer northern states, piled into Italian, Spanish and Greek bonds this year. Italian bondholders are sitting on returns of 6.9% for 2020, more than double the rate on German debt, according to Bloomberg Barclays indexes.

“Government bond investors are frogs in a boiling pot,” said Alberto Gallo, a money manager at Algebris Investments in London. “These are fake haven assets, they expose investors to significant downside.”

The list of risks that could unwind gains is long. It includes the fate of the fractious coalition government in Rome, Greece’s double-digit unemployment and simmering regional tensions in Spain.

But the securities have rallied regardless due to the European Central Bank’s unprecedented bond-buying programs and a landmark European Union decision to channel grants to the region’s governments, reducing their default risk.

“Whatever moral hazard existed before is on steroids now,” said James Athey, a money manager at Aberdeen Standard Investments, who started betting against Italian 10-year notes last month.

| Read More: |

|---|

|

Naysayers are warning bets based on policy maker support may be overdone. Citigroup Inc. said following Thursday’s selloff that investors will look to take profit, and that could drive up Italy’s yield spread over Germany. ING Groep NV agrees.

“One concern we have is that markets are already pricing a high probability of central bank easing,” said Antoine Bouvet, a strategist at ING. “We suspect a wave of profit-taking might cause a temporary re-widening in sovereign spreads ahead of the Oct. 29 ECB meeting.”

And any failure by the EU to deliver on its recovery fund could lead to a bigger pullback. BofA Global Research said markets could “reprice more meaningfully” if no progress had been made by December, given the plan was only agreed in principle.

“A proper breakdown in negotiations would easily see markets test not just 2020 but 2018 wides,” strategist including Sphia Salim wrote in a note.

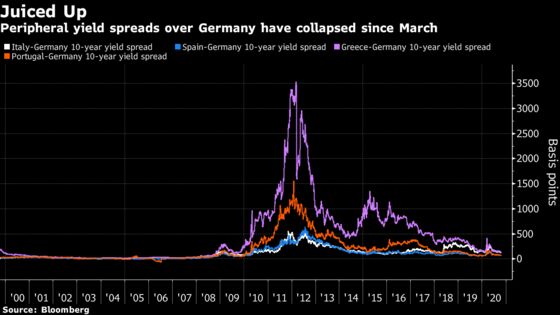

That would put the premium on Italian and Greek debt over Germany’s at more than 300 and 400 basis points respectively, compared with just under 150 basis points now. Italy’s benchmark yield dropped to a record low of 0.63% this week, down from nearly 3% during March’s turmoil.

Convergence Trade

For Patrick Armstrong, chief investment officer at Plurimi Wealth LLP, the advance in periphery bonds isn’t justified given the economic fundamentals.

The Greek government expects public debt-to-GDP will be close to 200% in 2020, while Italy’s has climbed close to 160%. The former is rated junk by Moody’s Investors Service, while the latter is just one notch above non-investment grade.

“It doesn’t make much sense when you look at debt, deficit and demographic dynamics, but that’s what QE does and is really supposed to do,” Armstrong said. “We are having no positions at all. Last time we held Italian 10-year bonds, they were yielding 2%.”

It wouldn’t be the first time investors have glossed over risks in the euro area.

For much of the euro zone’s first decade in existence, investors demanded less than a 50-basis-point premium over German bunds to hold Italian or Greek government bonds. The spread widened to more than 500 basis points for Italian securities during the euro-zone debt crisis, and well over 3,000 basis points for their Greek counterparts.

The question now is whether that great convergence trade will continue to take yields down to zero, or whether it’s run out of juice and could blow up again in the face of bondholders.

“History says that when Italy yields and spreads get down into this area, there is a pretty big asymmetry,” said Aberdeen Standard’s Athey.

©2020 Bloomberg L.P.