A Once-Booming Options Strategy on Wall Street Is Misfiring

A Once-Booming Options Strategy on Wall Street Is Misfiring

(Bloomberg) -- The shuttering of a $75 million fund this week by Russell Investments will have bypassed many investors, but its demise is the latest sign of trouble for a once-hot Wall Street derivatives strategy.

The Seattle-based investment firm is liquidating a fund that follows what’s known as call overwriting, an options-selling strategy that critics warn may have become too popular for its own good.

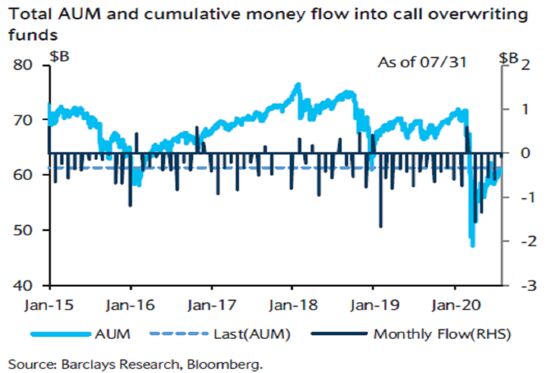

Some $60 billion is invested in options-based mutual funds, many in call overwriting strategies, according to Barclays Plc estimates. The worry is that an army of investors deploying the approach are exhausting premiums, making it among a slew of complex strategies now struggling to keep pace with the historic U.S. stock rally.

Russell began the liquidation this week and aims to distribute the fund’s assets “as promptly as possible” after Sept. 17, according to a filing. Spokespersons for the firm didn’t respond to an emailed request for comment.

The fund, which managed more than $100 million before the pandemic-induced selloff, holds primarily medium- and large-cap stocks and sells index call options. The latter generates income, but the fund’s gains are capped if shares rise high enough for the options to be exercised.

Like other short-term options-writing strategies, the Russell fund has struggled to capture the upside of U.S. stocks while suffering most of the drawdowns. The fund slumped 30% in March amid the Covid-19 selloff, modestly outperforming the S&P 500 Index’s 34% decline. However, the equity benchmark has surged 49% since then, compared with the Russell fund’s 23% rise.

The Russell strategy aims “to deliver similar long-term returns with lower volatility and reduced losses in down markets,” compared with “traditional U.S. equity investing,” according to a marketing document.

The product is edging out its benchmark this year, but lagging the S&P 500 Index by 14 percentage points. All told, since its 2012 inception, the fund has gained 33% versus the S&P’s 132%.

Lagging Strategy

Call overwriting funds flowered after the financial crisis as declining bond yields made investors desperate for income. QVR Advisors estimates that at the peaks in 2017 and 2019, institutions every month sold $800 million of vega, a measure of volatility exposure.

But critics say the selling has suppressed implied stock volatility, hitting the return potential of the trade. After a strong run from 1990 to 2009, the benchmark call-writing gauge has badly trailed the S&P 500 Index over the last decade. Call overwriting funds have suffered almost uninterrupted outflows over the past year, according to Barclays.

“For much of the past 10 years, upside volatility has been fairly depressed as markets have marched higher, so it hasn’t been a great trade,” said Chris Murphy of Susquehanna.

Selling options seeks to take advantage of the volatility risk premium, or tendency for realized swings to come in lower than what’s implied in prices of the derivatives. However, data over the past two decades show the premium has become badly eroded over time as big institutional players such as pension funds have piled in.

“The outperformance from 1990-2009 that most likely drove massive amounts of AUM to these strategies helps to understand why they have struggled since,” Dominick Paoloni and Pat Hennessy of IPS Strategic Capital wrote in a report last year. “Selling premium hasn’t been nearly as attractive since 2009.”

©2020 Bloomberg L.P.