A Brainard Fed May Mean Lower for Longer: Wall Street Reacts

A Brainard Fed May Mean Lower for Longer: Wall Street Reacts

(Bloomberg) -- The biggest signal yet that Federal Reserve Governor Lael Brainard is a major contender to replace Jerome Powell as Fed chair has triggered a wave of speculation over how financial markets would react if President Joe Biden announced her as his nominee.

Bloomberg News reported on Monday that Brainard was interviewed for the top job at the U.S. central bank when she visited the White House last week. The longest wait for the announcement in the modern era had already spurred uncertainty that Powell -- long thought to be heading for reappointment -- will win another four years when his current term ends in February.

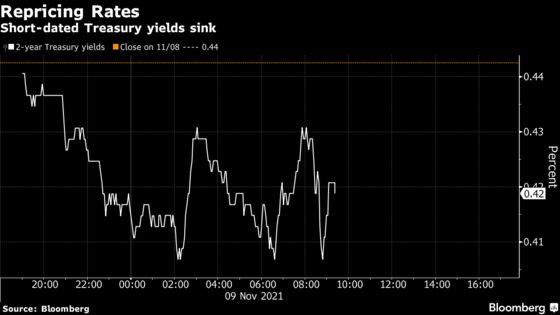

Treasury yields sank following the report as investors debated whether Brainard -- generally seen as more dovish on monetary policy than Powell -- would follow through on the Fed’s latest asset-purchase tapering timeline or hold off on raising interest rates for a longer period than currently anticipated.

The following are some thoughts from market participants of potential market reactions in the case of a Biden nomination of Brainard for Fed chair.

Lower for Longer

A Brainard appointment would be more bullish for the bond market, said BMO strategist Ian Lyngen. That’s because she would likely keep rates lower for longer and be less aggressive when eventually hiking, he said.

“She was always considered the ‘go-to’ replacement in the event Biden doesn’t renominate Powell,” he wrote in a note. “That said, it’s safe to assume that any candidate the administration would favor over Powell would be more dovish; hence the belly-led rally seen during the overnight session,” he said, referring to medium-term Treasury securities such as five-year notes.

Inflation Expectations

Brainard, if anything “seems more dovish, less inclined to raise interest rates quickly,” said Brian Nick, chief investment strategist at Nuveen. “If there’s any risk that she’s going to be the choice over Powell, what we’re seeing in the bond market -- lower rates, higher inflation expectations, lower real interest rates -- that squares with my understanding of what she’d be bringing to the table.”

Quick Test

“We don’t think that that event will cause significant volatility,” said Emily Roland, co-chief investment strategist at John Hancock Investment Management. At the same time, with several Fed board appointments now set to be filled, and with the pandemic economy’s evolution, the central bank could soon face a testing period, she said.

“We’ve seen with Powell that sometimes it takes a little bit of runway to get that communication just right,” she said in a Bloomberg Television interview with Alix Steel. “And that could be a challenge as we have a more junior group of Federal Reserve officials into next year at a time that the economy is slowing and inflationary pressures potentially need to be snuffed out more quickly.”

Hawkish Surprise

Sebastien Galy, senior macro strategist at Nordea Investment Funds, anticipates two phases of reaction. First, he sees equities reacting positively -- especially growth stocks, which tend to be more interest-rate sensitive. The shorter end of the Treasuries yield curve could flatten, he also said -- that is, the yield gap between shorter term notes such as two-year securities and slightly longer-dated ones such as five-year notes could shrink as the scale of expected Fed tightening in coming years diminishes.

“However, I expect the market to then become quite surprised by her turning more hawkish to anchor inflation expectations among households and corporates -- though that should take a few weeks,” Galy said.

2022 Election

Peter Boockvar, chief investment officer at Bleakley Advisory Group, predicted that Brainard -- a Democrat -- would hold the Fed back from raising interest rates until after the November 2022 midterm congressional elections, when Democratic control of both chambers will be up for grabs. The quantitative easing program may still run off as currently scheduled by June, however, he said.

“I’ll make a call that if she is Fed chair, maybe they’ll finish QE in June but they won’t raise rates until after the midterm elections,” Boockvar said in a note. “This all said, both Powell and Brainard are doves, so the eventual approach won’t be that much different with respect to monetary policy.”

Turbulent Time

Whether it’s Brainard or Powell, the next eight months or so -- when the Fed will be zeroing out its bond purchase program -- are going to be really uncomfortable for investors, said Lauren Goodwin, economist and portfolio strategist at New York Life Investments.

“The markets are not convinced by the Fed’s messaging that it will complete its taper before considering rate liftoff,” she said. “If we have a few more months of strong inflation prints, which I think most investors expect, then the narrative around the Fed’s patient approach will prompt rate volatility.”

Bigger, Later?

It would take time to understand what the implications are of Brainard at the helm of a reshaped Fed board, according to Phil Orlando, chief equity market strategist and head of client portfolio management at Federated Hermes. First question: would the new team follow through with tapering asset purchases and raising rates over the next two years, he said.

“If the answer to that is no -- and we believe the Fed is already behind the curve in terms of this inflation issue -- does that raise the raise the prospect of a potential need for a more Volcker-esque policy response somewhere down the road?,” he said in an interview with Bloomberg Television, referring to the rapid monetary tightening overseen by former Fed Chair Paul Volcker in the early 1980s to whip inflation. “We don’t know the answer to that, but I think the market is going to have to come to grips with that question once we know who the players are.”

Continuity Factor

There are many institutional forces that bear on Fed decision making and provide continuity, including the role of regional district banks and the influence of the central bank’s staff, said Michael Feroli, JPMorgan Chase & Co. chief U.S. economist.

“Since Brainard is considered a dove, at the margin one might expect to see inflation breakevens move higher,” Feroli said, referring to the yield premium of regular Treasuries over those linked to consumer prices. “With the important caveat that you never want to make too much of one day’s price action, the fact that the curve is flatter after yesterday’s Brainard news suggests the market also appreciates the continuity in Fed policy making.”

©2021 Bloomberg L.P.