Why Worry So Much About Recessions?

Why Worry So Much About Recessions?

(Bloomberg Opinion) -- As of this month, the U.S. economy has been growing for 10 straight years, tying the record for the longest expansion ever. Many people, including journalists and policy makers, see this as a great achievement.

I see nothing to celebrate. On the contrary, I think they’re measuring success the wrong way.

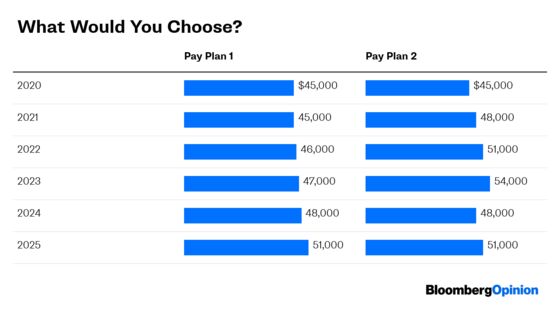

Imagine that you were offered two different pay options for the next six years:

Which would you take? Plan 1 shows consistent growth. Plan 2 is more variable, but it generates as much or more income every year. If what you want is more money, plan 2 is clearly preferable.

The same logic should hold for U.S. output per person: More is better. Yet most economic observers would choose plan 1, because it features six years of steady expansion. Plan 2, by contrast, has a terrible “recession” from 2023 to 2024, and arguably an “overheating” economy from 2021 to 2023.

This isn’t merely a theoretical point. Economy watchers often point to the absence of a recession in the past 10 years as a sign of good policy making by the Federal Reserve and others. But, as we just saw, being recession-free might not be the best outcome. On the contrary, long periods without slumps often indicate many years of poor economic performance.

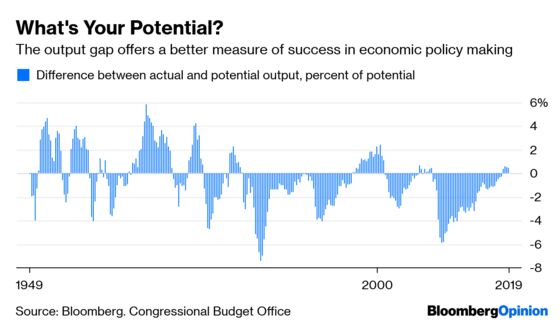

What’s a better way to keep score? One option is to use the “output gap.” It’s the percentage difference between actual output and what the nonpartisan Congressional Budget Office estimates the economy could produce if it were operating at capacity, with all able workers and capital fully engaged. A negative number means the economy isn’t meeting its full potential, while a positive number means it’s going too fast. Here’s a chart of the output gap since 1949:

The chart correctly shows that the past decade has been the worst in the past 70 years. Despite the lack of recessions, the economy has been operating well below potential for much of the period. Indeed, the output gap has been negative through almost all of the current millennium. The U.S. would actually have been better off with a decade like the 60s.

Fed officials are meeting this week to review their framework -- that is, the way they assess the economic environment and seek to manage employment and inflation through their monetary policy choices. It’s extremely important that they use the right measure to judge how well they’re doing their job. Good policy shouldn’t be about keeping output below potential to avoid possible recessions. It should be about making choices that lead to the highest possible output and employment, without unduly high inflation. Focusing more on a measure like the output gap could help them achieve that goal.

To contact the editor responsible for this story: Mark Whitehouse at mwhitehouse1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Narayana Kocherlakota is a Bloomberg Opinion columnist. He is a professor of economics at the University of Rochester and was president of the Federal Reserve Bank of Minneapolis from 2009 to 2015.

©2019 Bloomberg L.P.