3M and Roper Are Captains of Their Fate on Asset Sales

3M and Roper Are Captains of Their Fate on Asset Sales

(Bloomberg Opinion) -- 3M Co. and Roper Technologies Inc. have some things in common: Both have new CEOs, both have labyrinthine structures that they’re trying to rectify with “realignments,” and both seem likely to announce more divestitures in the coming months.

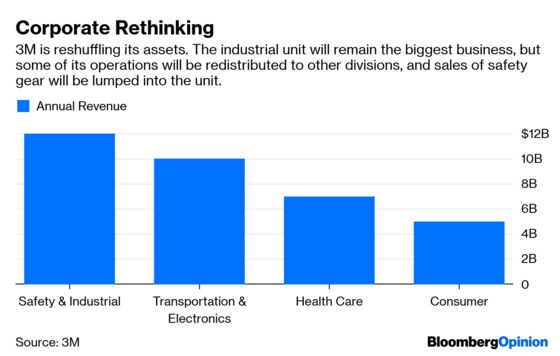

3M said on Monday that it would shrink its five operating segments to four. The idea is to organize 3M’s businesses based on the type of customer they serve, rather than just a rote labeling by market. One of the more interesting outcomes is that 3M’s automotive exposure will be spread across three segments: sales to body shops will be part of a new “Safety & Industrial” unit; sales to manufacturers will fall into the “Transportation & Electronics” division; and sales to retail shops will be part of the “Consumer” unit. The auto market has been a particular pressure point for 3M of late amid slowing global production, and it’s one reason new CEO Michael Roman has had to walk back guidance four times in a year. Other changes correct obvious mismatches: films used to make graphics and reflective sheeting used for license plates will be sold alongside electronic-display materials for smartphones, rather than worker-safety gear. Purification tools will be moved out of the industrial unit and into 3M’s health-care business.

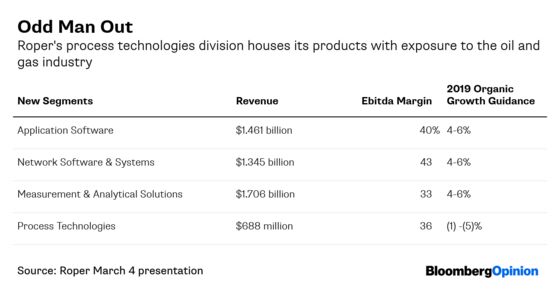

The results of a similar portfolio review at Roper were announced earlier this month by CEO Neil Hunn, who began it more than a year ago when he was chief operating officer. Under the leadership of longtime CEO Brian Jellison, who died last year, Roper had shifted the center of gravity for its businesses away from fluid-testing equipment and oil and gas pumps to high-margin specialty software and services. Its organizational structure hadn’t kept pace: water meter-reading products and toll tags were sold out of the same division as software for legal firms. So Roper started from scratch and reordered its operations based on their underlying business model. All the application software will be in one unit, the company’s employee-badge reader products, tolling-system technology and construction industry software platform are in another and the legacy hardware-focused operations are split between a division focused on measurement tools and one hawking pumps, valves, compressors and controls.

Roper and 3M have announced their fair share of divestitures, but both have been relatively immune from the breakup fever working its way through the rest of the industrial sector. In 3M’s case, its myriad businesses are connected by science and shared materials; the company sells Scotch tape to consumers, high-bond tape for the automotive industry and specialty solar tape for the energy sector. At the end of the day, they are all adhesives. Roper operates almost like a private equity firm, with a highly decentralized structure that allows its business heads to stay nimble. But this does make for some odd pairings, and the decision to recalibrate the two companies based on go-to-market strategies and business models suggests the traditional ties that have bound these businesses together aren’t unbreakable. In some ways, the reshuffling of the deck shows just how mismatched the cards were in the first place.

A full-blown breakup of 3M would be tricky given patent protection considerations, but the company has been willing to divest assets that underperform or no longer make sense. Roman has experience here, having previously served as vice president of business development. 3M last year sold its optical fiber and telecommunications cabling assets to Corning Inc. for $900 million. Asked about 3M’s portfolio at a Barclays Plc conference in February, Roman agreed that there could be some pruning in the health-care and consumer units akin to what the company has done elsewhere and said it could also review parts of its industrial business.

At Roper, the reorganization makes the legacy pump and valve operations look even more marginalized. The so-called Process Technologies division will account for 13 percent of overall sales, the lowest share of the primary units, and the company is expecting as much as a 5 percent slump in organic revenue for those operations in 2019. Jellison justified keeping the oil and gas products because Roper’s decentralized structure and operating rigor had helped shield them from steep profit swings in economic downturns. But as investors have seen with General Electric Co., picking up the baton for a visionary conglomerate builder isn’t the easiest job, and Hunn will want to make his own mark on Roper. Already, he has announced the $225 million sale of scientific imaging assets to Teledyne Technologies Inc., completing a wind-down of that business that was kick-started by the $925 million divesture of Roper’s Gatan electron-microscope instrumentation operations to Thermo Fisher Scientific Inc. announced last June. Divestitures raise money for acquisitions: Roper announced late Monday that it would acquire British visual-effects company Foundry Visionmongers Ltd. for 410 million pounds ($543 million). The business fits with Roper’s increasing focus on niche software, but it’s quite expensive at more than seven times Foundry’s expected revenue over the first year of ownership.

Not all portfolio changes have to come amid activist investor pressure or out of a sense of desperation. Roper and 3M are two companies that look poised for a shake-up, but they have an opportunity to do it on their own terms.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.