As Bets on an Argentina Default Grow, IMF Is Last Bastion of Hope

As Bets on an Argentina Default Grow, IMF Is Last Bastion of Hope

(Bloomberg) -- Terms of Trade is a daily newsletter that untangles a world embroiled in trade wars. Sign up here.

Argentina investors scorched by one of the worst sell-offs in the history of emerging markets are banking on the International Monetary Fund to buy the country some time.

IMF officials are visiting Buenos Aires and will give their recommendation within weeks on whether to disburse another $5.3 billion to the country from a record bailout approved in 2018. Their decision could determine whether Argentina enters a chaotic default in the next few months or if the government gets more breathing room to shore up its finances and potentially seek a negotiated restructuring.

Argentina needs the money badly, and quickly. Foreign-currency reserves have plummeted more than $10 billion in the past month as policy makers sought to shore up the peso in the wake of a stunning loss in a primary for the market-friendly government coalition. A refusal by the IMF could trigger a flood of capital out of the country, undercut the currency further and trigger a default within a year.

“There is no way that the IMF would be ready to simply throw in the towel,” said Thierry Larose, a Zurich-based senior portfolio manager at Vontobel. “Stopping the disbursement of the next tranches of the IMF program would inevitably put at risk” repayments on the existing loan.

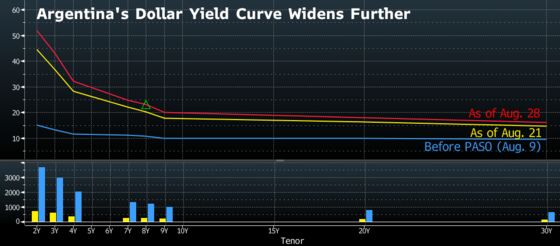

That optimism didn’t stop Argentina’s century bonds from falling to 44 cents on the dollar Wednesday, and some euro-denominated notes traded below 40 cents. Over the longer term, swaps traders see an 89% chance of default within the next five years.

But there’s still some degree of confidence Argentina will be able to survive a year without missing a payment -- 12-month swap contracts show just a 48% chance of non-payment.

Financing Gap

Without the loan disbursement and cut off from global money markets, it’s hard to make the numbers square for Argentina.

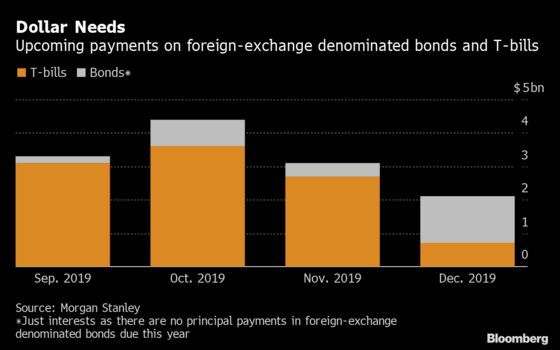

Morgan Stanley estimates the the South American nation needs $12.9 billion for repayments on Treasury bills and bonds in the last four months of the year. State-owned enterprises are expected to roll-over some of that debt.

Meanwhile, the nation’s dollar buffers are withering. Foreign exchange reserves have fallen to $57.5 billion after a landslide victory for the opposition in Aug. 9 primaries roiled the markets, sending stocks tumbling along with the peso and bonds.

Capital Economics estimates that net reserves -- which exclude deposits at commercial banks -- are currently at $19 billion, down from $30 billion in mid-April. That only covers a quarter of Argentina’s gross external financing needs of $100 billion, which includes debt maturing over the next year plus the current account deficit.

Foreign Reserves

Argentine officials must convince the IMF that the debt is sustainable and that it has decent prospects of access to private capital. During the last review on the program, the IMF concluded that it was sustainable “but not with a high probability.”

It’s not clear when the IMF board will make a final decision on the latest disbursement.

During their visit, officials have scheduled meetings with government figures as well as aides to Alberto Fernandez, the left-of-center politician looking to unseat President Mauricio Macri in October’s vote. Fernandez has given mixed messages about his stance toward the IMF, indicating he’d like the flow of funds to continue while also complaining that so far the money has done little excect finance capital flight.

“If they don’t disburse, the government will need to use international reserves to repay peso debt, and monetary transfers to make peso payments,” said Carolina Gialdi, a senior fixed-income strategist at BTG Pactual Argentina in Buenos Aires. “For the market it increases further front-end risks.”

Gialdi expects Argentina will get the next disbursement. The IMF has already transferred $44 billion to the country since the $56 billion rescue program started in June 2018.

That is one of the reasons why investors are betting the IMF won’t throw in the towel -- with so much money already committed, it would be hard to give up now. Repayments aren’t scheduled to begin until 2021.

It’s “the old saying about if I owe you $1,000 it’s my problem, but if I owe you $1 million, it’s your problem,” said Edwin Gutierrez, the London-based head of emerging-market sovereign debt at Aberdeen Asset Management. “They can’t send Argentina over the tipping point.”

To contact the reporter on this story: Aline Oyamada in Sao Paulo at aoyamada3@bloomberg.net

To contact the editors responsible for this story: Julia Leite at jleite3@bloomberg.net, Philip Sanders, Brendan Walsh

©2019 Bloomberg L.P.