Fed Needs Rate Cuts to Plug Repo Black Hole, Credit Suisse Says

Fed Needs Rate Cuts to Plug Repo Black Hole, Credit Suisse Says

(Bloomberg) --

The Federal Reserve needs to cut rates further to address a looming funding squeeze in U.S. money markets being fueled by foreign central bank demand for its reverse repurchase agreements, according to Credit Suisse Group AG.

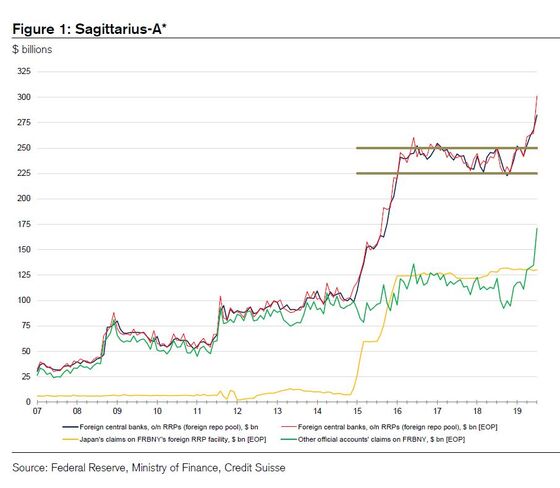

Usage of the foreign repo pool -- where central banks invest cash with the New York Fed at rates comparable to money-market repo rates -- is close to $100 billion so far this year, driven by haven flows, strategist Zoltan Pozsar wrote in a research note Wednesday. It could hit $200 billion by year-end, exacerbating a glut in collateral caused by $800 billion in Treasury supply and driving up short-term funding costs.

Pressure caused by this “supermassive black hole” would seep into the foreign exchange forward, cross-currency basis and Libor-OIS markets, according to the note.

“Because inflows into the facility sterilize reserves and add collateral to the financial system, they worsen the collateral surplus,” Pozsar wrote. “When banks are at their intraday liquidity limits it means that every penny that flows into the facility makes it harder for banks to fund dealers.”

Rate Shopping

Thanks to the trade war and inverted U.S. yield curve, central banks attempting to weaken their currencies are making use of the RRP pool rather than buying Treasuries as they did in the past, Pozsar said. “Central banks are rate shopping and an uncapped foreign RRP facility is what enables that.”

A series of rate cuts to steepen the U.S. yield curve and incentivize them to switch back to currency-hedged Treasuries would help solve the problem, rather than a technical fix, such as a standing repo facility or asset purchases that could lead to Treasury monetization, according to Pozsar.

What is required is rate cuts “aggressive enough to re-steepen the curve so that dealer inventories can clear” Pozsar said. “Monetizing record deficits is likely not what this FOMC wants to be remembered for.”

Investors fully expect another rate cut at the Fed’s Sept. 17-18 meeting and further easing this year. A big clue could come from Chairman Jerome Powell when he speaks on Friday at the Kansas City Fed’s annual policy retreat in Jackson Hole, Wyoming.

To contact the reporter on this story: Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Cormac Mullen, Joanna Ossinger

©2019 Bloomberg L.P.