Suddenly Britain's Bonds Look Like the Weakest Link for Some

Britain's Yields at Their Lowest May Have Gone Too Far for Some

(Bloomberg) -- Some of the more savvy investors are betting U.K. bonds risk falling behind after riding the global debt rally at full speed.

At least some investors are favoring a relatively bearish approach toward gilts, betting that inflation stoked by the pound’s declines will leave little room for the Bank of England to cut interest rates, even as other central banks do so.

Aberdeen Standard Investments’s James Athey is short U.K. rates via swaps, while BlueBay Asset Management’s Mark Dowding has a similar position in gilts.

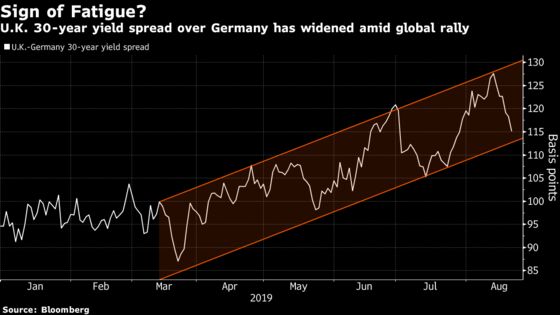

Benchmark gilt rates hit record lows and the yield curve inverted last week as trade tensions worsened the global economic outlook, sparking a worldwide capital flight into the safety of government debt. Yet the U.K. market may soon start trailing the trend given the risk that the nation’s government will step up debt sales and boost spending, according to Dowding, to shore up growth prospects ravaged by Brexit uncertainty.

“It’s not necessarily about gilt yields rising immediately, but that they will fall less than other markets such as the U.S. and Australia,” Aberdeen Standard’s Athey said. “We are increasingly pricing very bad news and so the potential for good news shocks increases.” It’s less attractive to be invested in U.K. bonds than in markets where the central bank has more scope to cut rates, he said.

The BOE’s latest economic forecasts published this month assumed a smooth Brexit and reiterated that rates will need to gradually rise to bring inflation to target. That is at odds with current U.K. money-markets pricing, which implies a reduction in early 2020. The central bank’s next policy review is on Sept. 19.

Yields on 10-year gilts slumped more than 80 basis points since the end of 2018 to a record 0.40% on Aug. 15, a day after they dropped below two-year rates for the first time since the global financial crisis. They were at 0.48% Thursday.

While global risk aversion may limit any yield rebound, the future performance of gilts may depend more on domestic politics and Brexit.

Fiscal Risk

One possibility is a snap election with higher odds of a win for the opposition Labour Party, which may favor an expansive fiscal policy that would boost yields, according to BlueBay’s Dowding, who is short 10- and 30-year gilts versus long-dated bonds of Italy and Greece.

“We think that gilts are significantly underpricing the risk of an election before the end of the year and a possible Labour coalition win,” he said, forecasting 10-year yields to rise to 1.5% by year-end on a change of government or another EU referendum, or stay around 0.5% on a disorderly Brexit.

Not everyone believes the rally is over in gilts, which still offer positive yields at a time when investors need to pay to hold most top-rated debt in Europe.

“Yields are low, but as we have seen from elsewhere, we can go lower” given the heightened uncertainty over politics and monetary policy, said Kacper Brzezniak, a portfolio manager at Allianz Global Investors. Still, predicting any one direction in gilts is difficult for now and there may be more value in positioning for a steeper 10- to 30-year yield curve, according to him.

Before the recent surge in global bonds, Banco Santander SA strategist Adam Dent had forecast the 10-year U.K. yield to be at 1.1% by the end of this quarter. While that now looks “implausible,” the rate should still end the period higher from current levels, he said.

“I find it impossible to have much conviction on bearish trades after moves like this, but chasing a further rally also seems implausible. I’m not ready to catch this falling knife yet!” Dent said.

To contact the reporters on this story: Greg Ritchie in London at gritchie10@bloomberg.net;Charlotte Ryan in London at cryan147@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Anil Varma, William Shaw

©2019 Bloomberg L.P.