Canopy Shares Slide as Analysts Surprised by Revenue Decline

Canopy Shares Tumble as Analysts Surprised by Declining Revenue

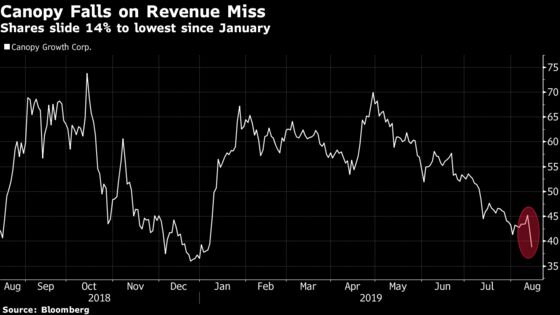

(Bloomberg) -- Canopy Growth Corp. shares tumbled as much as 14% to the lowest since January after the pot producer reported revenue that missed the lowest analyst estimate and appeared to lose its first-place share of the Canadian market.

Canopy also posted a decline in recreational cannabis revenue and took an C$8 million writedown to account for potential reimbursements to its wholesale customers for unsold product. Analysts agree that it was a broadly disappointing quarter, but say the one bright spot is Canopy’s large harvest and growing inventory, which could position it well to compete as new derivative products such as edibles are legalized in Canada later this year.

Here’s what analysts are saying:

Canaccord Genuity, Matt Bottomley

Results were “well under our expectations as the company posted its second quarter of sequentially lower net cannabis revenues.” Most notably, it appears that Canopy lost its first-place share of the Canadian market to Aurora Cannabis.

Gross recreational cannabis revenues fell 11.4% from the prior quarter due to a “very surprising shift” in sales of oils and softgels, which tumbled to C$200,000 from C$36.5 million.

One positive note is Canopy’s C$394 million of inventory on hand, including C$93 million of finished products, “which we believe likely positions the company well to compete in the Cannabis 2.0 market once additional derivative products are implemented later this year.”

Maintains speculative buy rating, C$70 price target.

William O’Neil & Co., Andrew Kessner

The amount of cannabis harvested, which grew 183% from the prior quarter, is “the most positive aspect of Q1’s results, as this production capacity puts the company in a strong position to compete in the market for vapor products, beverages, and edibles when those products become legal to sell in late Q4.”

However, Kessner notes that Canopy posted no organic international sales growth and domestic sales declined “despite a substantial uptick (we estimate +55%) for the broader Canadian recreational cannabis market during the quarter.”

In addition, Canopy’s C$1.2 billion non-cash loss on the extinguishment of warrants held by Constellation Brands Inc. was “surely jarring to some investors.”

BMO Capital Markets, Tamy Chen

“Canopy may have had a suboptimal inventory mix relative to rec consumer demand,” and sales should improve somewhat going forward. However, Canopy’s focus on building an inventory of cannabis beverages prompts caution, “as we believe the initial uptake for beverages may be muted by limited in-store shelf space.”

“In addition, we believe margins and cash flows could further deteriorate” as Canopy spends to manufacture more costly derivative products like beverages. Weak gross margins in the quarter already point to “significant challenges” at Canopy’s greenhouses and the costly procurement of third-party supply

Maintains market perform rating, C$60 price target.

Eight Capital, Graeme Kreindler

Canopy harvested 40,960 kilograms of cannabis in the quarter, the largest quarterly harvest to date of any Canadian pot producer, which “alone could service the vast majority of quarterly demand in the Canadian market in its existing form.”

“We expect to receive more detail on the upcoming conference call as to whether a majority of this product will be stockpiled ahead of the derivative market, or whether WEED expects to aggressively price product to grow its market share position.”

Believes Canopy will minimize its spending on strategic investments and acquisitions until a full-time CEO is in place.

Maintains buy rating, C$70 price target.

To contact the reporter on this story: Kristine Owram in Toronto at kowram@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Will Daley, Scott Schnipper

©2019 Bloomberg L.P.