Your Phone Could Help Make Mortgage Bond Traders Miserable

Your Phone Could Help Make Mortgage Bond Traders Miserable

(Bloomberg) -- A massive wave of homeowners now has an incentive to refinance their mortgages and they could find the process faster than it’s been in recent memory thanks to technology improvements.

Borrowers of about $1.2 trillion of home loans could save at least half a percentage point of interest by refinancing, according to data compiled by Brean Capital. That’s about five times the mortgages eligible for refinancing at the end of last year. Borrowers are benefiting from mortgage rates that have reached the lowest levels since 2016 as the Federal Reserve appears to be moving closer to easing monetary policy again.

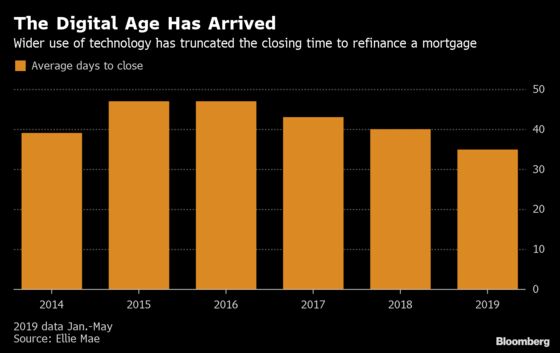

More of the mortgage application process is now happening online and on mobile phones, which means when homeowners do refinance the process may take around 35 days compared with the 47 days it took as recently as 2016, said Jonathan Corr, president and CEO of Ellie Mae Inc. Corr’s company makes software that helps streamline and automate the mortgage origination process. Some lenders are advertising closings in 21 days or less.

Key documents like the promissory note can now be signed digitally and then stored in the cloud instead of being put in a box and filed in a vast warehouse, according to Simon Moir, Chief Product Officer at eOriginal Inc., a provider of technology that offers electronic transaction management solutions. This reduces the chance it can be lost.

That’s good news for borrowers who can refinance faster than before. But it’s trouble for investors in the $7.3 trillion mortgage bond market, who will find their money getting returned to them sooner than they had expected, even compared to past times when home loan rates were falling. They will probably have to reinvest the money they get at lower yields. Investors that paid more than face value for their bonds could get particularly hurt, because they’ll get repaid at 100 cents on the dollar.

“The recent rally may have a bigger impact on July prepayments than what we would have expected to see a few years ago,” said Scott Buchta, head of fixed income strategy at Brean Capital. Even though there may be a pick-up in prepayments from borrowers that refinanced in 30 days, the majority of homeowners will take 45 days, he said.

The bond market rally that has cut the 30-year mortgage rate to 3.73% has already driven the volume of mortgages refinancing applications close to its highest level since late 2016. The steep drop in borrowing rates has increased concern over higher prepayment speeds and helped mute mortgage sector performance which has returned 0.12% less than Treasuries this year.

Lenders are doing what they can to make it easier for borrowers to refinance. With the increased use of mobile and online applications for mortgage refinancing applications, “we’ve seen cycle times reduced by 7-8 days, a good 15% to 20% drop compared to previous methods,” said Sonu Mittal, head of retail mortgage lending at Citizens Financial Group in Providence, Rhode Island.

Mortgage application technology has been steadily improving for years, with the support of Fannie Mae and Freddie Mac, the government-backed mortgage companies. Freddie Mac, for example, has been buying digital mortgages since 2005.

The more technologically advanced lenders appear to be the non-banks now, according to Buchta. But the bigger banks are likely to follow, he said.

“We haven’t even realized the full potential yet,” said Citizens Bank’s Mittal.

To contact the reporter on this story: Christopher Maloney in New York at cmaloney16@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Christopher DeReza

©2019 Bloomberg L.P.