One Big Argument for Dollar Strength: It's Expensive to Short

Even If You Want to Short the Dollar, It's Going to Cost You

(Bloomberg) -- Investors who want to bet against the dollar’s unexpected strength are hitting a costly roadblock.

The case for a weaker greenback goes like this: The Federal Reserve has shifted to a wait-and-see approach on rate hikes, while signs of stabilizing growth in China and the prospect of easing trade tensions could boost confidence in the global economy.

But as strong as that argument may be, it’s done little to dent the dollar, which hit a 2019 high Thursday on signs the U.S. economy is doing better than the rest of the world. But there’s another big reason for dollar strength, and it boils down at least in part to market mechanics.

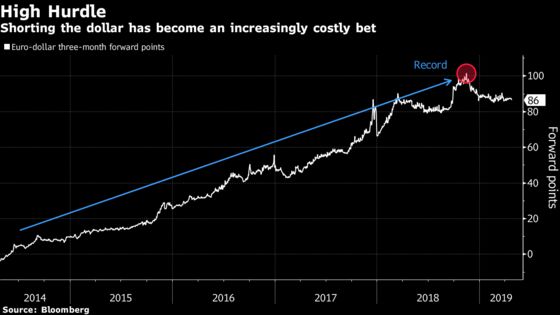

Short-term interest rates -- which determine the price of currency futures contracts, or forwards -- are much higher in the U.S. than in Europe and Japan. For example, the three-month London interbank offered rate for dollars is 2.58 percent, almost 300 basis points above the comparable rate for euros. The difference has almost doubled in the past two years, raising the cost of shorting the greenback for fund managers.

“While the dollar is expensive in a historical context, we are resisting the temptation to go short,” said Columbia Threadneedle’s Gene Tannuzzo, a manager of the $4.5 billion Columbia Strategic Income Fund. “The yield advantage is meaningful, which affects the hedging and shorting cost versus the euro.”

The situation could persist for years. Even with expectations building for a Fed rate cut, the gulf between U.S. and European yields has proved difficult to whittle down as the European Central Bank also mulls stimulus options. That’s led to a steady creep higher in currency forwards, as seen in euro-dollar three-month forward points, which hit a record high last year.

And for that reason, Minneapolis, Minnesota-based Tannuzzo is buying euro-denominated corporate debt -- and hedging the currency exposure back into dollars.

Invesco Advisers Inc. has taken on a similar mindset. The money manager is hedging purchases of European corporate bonds, removing the need to short the U.S. currency.

“If we’re outright short dollar, we’d be paying the forward points, so it’s something you have to take into account,” said Noelle Corum, a portfolio manager at Invesco based in Atlanta. “If you hold it for too long, it’ll eat into your bottom line.”

Even though she expects the greenback to weaken by 5 percent this year on better growth in China and Europe, Corum said the cost to short the currency is a hurdle.

The Bloomberg dollar index, fueled in part by recent strength in U.S. stocks and bonds, on Thursday climbed as much as 0.3 percent to a level unseen since December, before slipping to trade little changed on the day.

Exacerbating the situation is low volatility, which has made carry trades -- borrowing in lower-yielding currencies such as the euro to invest in higher-yielding markets, like the U.S. -- all the more attractive. So traders are likely to steer clear of bearish dollar bets until there’s a meaningful rebound in global growth, according to Jefferies LLC.

“Given that it costs money to be short dollars, it deters people from doing it unless they feel a move that’s bigger than that carry cost is imminent,” said Brad Bechtel, global head of foreign-exchange. “In a low vol world where carry becomes important, the last thing you want to do is be short the dollar when you can be short cheaper alternatives like the yen, Swiss franc or euro.”

To contact the reporter on this story: Katherine Greifeld in New York at kgreifeld@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Randall Jensen, Mark Tannenbaum

©2019 Bloomberg L.P.