United Technologies’ Merger Clock Ticks Down

United Technologies’ Merger Clock Ticks Down

(Bloomberg Opinion) -- Timing is everything in M&A.

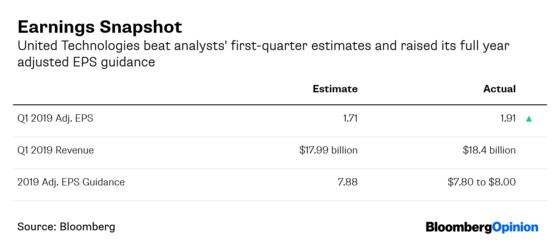

United Technologies Corp. CEO Greg Hayes said Tuesday that the window of opportunity was nearly closed for merging rather than spinning off its Carrier building-controls unit and Otis elevator division. The company has made the necessary tax filings with U.S. and Canadian authorities for the spinoffs and remains on track to have the businesses operating independently by the end of this year, with the splits expected to be completed in the first half of 2020. Attractive opportunities remain “in the long term from an M&A standpoint,” Hayes said on a call to discuss first-quarter earnings that surpassed analysts’ expectations. “But those opportunities that exist today will also exist the day that the businesses get spun off.”

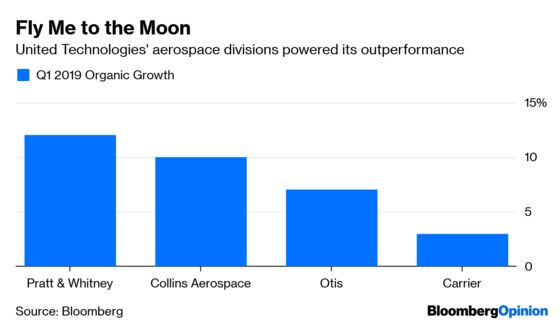

The Carrier division — which sells heating, ventilation and fire-safety products — has drawn the most speculation. Recall that Hayes had previously stipulated that any deal for Carrier would need to be tax free. That made Johnson Controls International Plc the likeliest suitor because it was roughly the right size for a so-called Reverse Morris Trust combination. Johnson Controls has its own version of a ticking clock: about $8 billion in expected post-debt reduction proceeds from a sale of its automotive battery unit. The divestiture is set to close in June, and CEO George Oliver has vowed to use the proceeds “as quickly and as efficiently as we can.” After initially saying that money could be earmarked for M&A, he indicated in February that it would be directed toward buybacks. Even so, Johnson Controls and Carrier should be able to structure a merger to end up with adjusted gross leverage below 3 times, which would keep the combined company within investment grade levels, according to Bloomberg Intelligence analyst Joel Levington.

It may be that Johnson Controls and United Technologies just couldn’t agree on the math. The onerous ownership requirements for the Reverse Morris Trust are the main reason it’s used so rarely. Hayes also wanted full value for the Carrier business, which in his mind meant a multiple of “12 times or 12.5 times” as a standalone entity. That implies a price tag of nearly $50 billion on an Ebitda basis. It’s not clear why this dynamic would get any easier should United Technologies spin off Carrier first. Takeovers of recently spun-off companies — while not impossible — can also be tricky to configure tax-wise, so the two companies may run into similar valuation and ownership debates. But time can do interesting things to companies’ sense of their own self-worth. On the flip side, a post-spinoff Carrier would also be able to expand its M&A horizons and act as the buyer. That could put the likes of Lennox International Inc. — which is likely too small for a Reverse Morris Trust — back in play.

That’s a sturdy start to stand on as it considers how to handle the rest of the breakup.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.