Nestle Discipline Cements Its Lead Over Unilever

Nestle Discipline Cements Its Lead Over Unilever

(Bloomberg Opinion) -- Two consumer goods giants, two first-quarter reports that exceeded analysts’ expectations. Which is better?

Nestle SA and Unilever both have the same problem. They have to show they can grow, but at the same time improve profitability. To this end, both are reshaping their core portfolios. Nestle has an activist investor lurking in the background, while Unilever is at risk of becoming a target for one. It’s a tall order to manage all of this.

Thursday’s financial statements suggest that Nestle SA is on a firmer footing than Unilever.

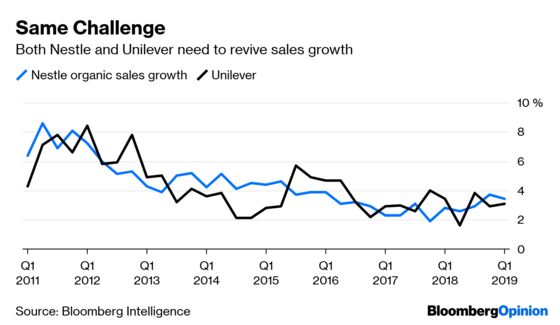

The Swiss company reported first quarter organic sales growth of 3.4 percent, beating the consensus analysts estimate for 2.8 percent. It’s a good start to Mark Schneider’s third year as chief executive officer.

Petcare was one of the key contributors to this expansion. It is one of the categories Schneider is counting on for growth, so its performance bodes well for the CEO’s strategy. It’s a similar story with the turnaround in U.S. frozen food, which had struggled to cope with changing consumer tastes.

Outside of its organic growth, Schneider’s acquisitions appear to paying off. The $7.15 billion deal to market Starbucks Corp. products is already getting coffee capsules and other goods onto supermarket shelves. More will follow as Nestle expands the brand’s geographic reach. Disposals are also continuing apace, with reviews of Nestle Skin Health and the Herter meat business set to be completed later this year.

Nestle’s expectation for improving sales and profit seems correct. The company appears to be on its way to achieving its financial goals of mid-single digit organic growth by 2020, and an operating margin of 17.5 percent to 18.5 percent.

The path looks a bit rockier for Unilever. In Chief Executive Officer Alan Jope’s debut reporting period, the company said first-quarter underlying sales growth surpassed expectations – 3.1 percent versus a 2.8 percent company-compiled estimate.

Although Unilever said it was on track to meet a 2020 target for a 20 percent operating margin, it forecast that sales growth this year would be in the lower half of its 3-5 percent range. If the revenue outlook doesn’t improve over the coming months, the company’s progress toward its goal could prove disappointing.

One issue is that, while Schneider has focused M&A on Nestle’s key categories for growth, Unilever has taken a more scatter-shot approach. Jope seems to have followed his predecessor, Paul Polman, by picking up businesses from premium cosmetics to the Vegetarian Butcher, a maker of plant based meat substitutes, to GlaxoSmithKline Plc’s Indian consumer business.

The company has made 29 acquisitions since 2015. Most of these are in beauty and personal care, and include some bets on millennial-friendly startups. Some are paying off. Seventh Generation, a natural homecare business, helped this division to generate strong sales growth in the first quarter.

But the range is broad, so there’s a risk Unilever’s portfolio becomes unwieldy. The company must also prove it is up to the task of absorbing entrepreneurial firms into its more-formal corporate culture.

Though acquisitions contributed double-digit sales growth in the first quarter, Jope must do more to show that the new brands will pull their weight. And while the 11 disposals, including the spreads division, are a good start, it should go further in offloading businesses in food, and possibly homecare.

Unilever stock rose as much as 4 percent on Thursday, whereas Nestle was up by about 1 percent. However, the Swiss company continues to command a higher valuation, indicating that investors still more faith in its strategy.

The premium to Unilever is deserved. Schneider is gradually ticking items off of his to-do list, and keeping an activist investor at bay at the same time. Unless Jope shows that he can be equally disciplined, he risks attracting an aggressive shareholder that will push for more radical change.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.