Derivatives Are Still Too Dangerous

Derivatives Are Still Too Dangerous

(Bloomberg Opinion) -- Financial regulators have done a lot to reform the derivatives markets that helped turn the financial crisis of 2008 into a global disaster. But their work is unfinished — and there’s even a danger that, in one way, they might have made things worse.

Derivatives are bets on the performance of something else, such as stocks, interest rates or creditworthiness. They can be useful in mitigating risks and expanding investors’ choices: A bank, for example, might use an interest-rate derivative to protect itself against rising borrowing costs, or a hedge fund might use a credit derivative to bet against a company’s bonds. But because they enable big wagers with little money down, they can quickly generate losses and cash demands large enough to destabilize the entire financial system.

For a long time, governments left the derivatives market largely to its own devices. At best, only the parties to the contracts knew who owed what to whom, or how much collateral had been posted to cover potential losses. The folly of this approach became apparent when, in the darkest days of the 2008 crisis, it emerged that a single company — insurance giant AIG — owed billions on subprime-mortgage bets to several of the world’s largest banks and didn’t have the cash to pay up. Taxpayers had to provide $182 billion to keep the company afloat and avert a broader collapse.

Since then, global regulators have reorganized the market around a time-tested institution: the clearing house. It stands between trades, keeps track of obligations, and ensures that everyone puts up enough collateral. If a customer goes bust, the clearing house is responsible for making good on debts to other customers. Globally, at least 37 percent of all credit-derivative transactions now go through such central counterparties. They’re crucial to the functioning of the entire system, allowing participants to trade without worrying about each other’s creditworthiness.

So far, so good. But what happens in a crisis? Unfortunately, clearing houses can easily go from being sources of stability to propagators of contagion. It all depends on whether they have enough resources — in the form of collateral, guarantee funds and shareholder equity — to cover any defaults or other losses. If they don’t, they’d have to turn to surviving counterparties, primarily big banks, for emergency cash infusions just when those institutions can least afford it. Worse, if that fails, they can start tearing up derivatives contracts — contracts that, in many cases, investors would be relying on to mitigate losses. Even the remote possibility of such an outcome could paralyze markets.

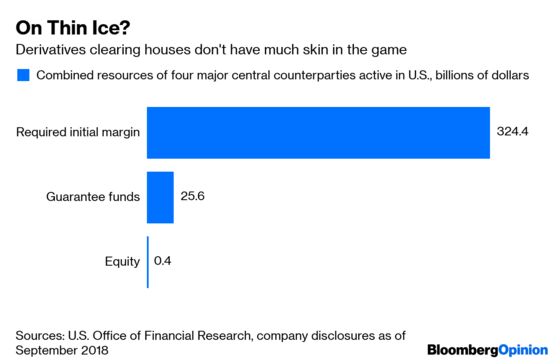

So do they have ample resources? The evidence isn’t encouraging. Once collateral (also known as margin) is depleted, there’s not much cushion. Guarantee funds, prepaid by all customers, typically amount to less than 10 percent of total collateral, and equity to less than 0.3 percent. Late last year, a single default in the Nordic power market burned through two-thirds of a Nasdaq clearing house’s guarantee fund. The thin layer of equity is particularly troubling: If the clearing houses’ owners have so little skin in the game, competing for business will tend to take precedence over ensuring that customers post adequate collateral.

To do their job properly, clearing houses must be unassailable. To that end, the Systemic Risk Council, a nonpartisan group of former government officials and finance experts, has made some useful proposals. First, clearing houses must increase their capacity to absorb losses. This could come in the form of equity, or of special bonds that would convert into equity when necessary. Also, they should contribute to a common global fund that would provide support in cases where a single member’s resources proved inadequate. This would pool some risk and give clearing houses a useful incentive to monitor each other’s financial health.

That’s not all. Regulators should conduct public stress tests of the clearing houses, just as they do with the largest banks. Flawed as they may be, the tests can at least ensure that management is considering credible worst-case scenarios. And clearing houses should provide the public with more financial information — for example, on peak margin payments to and from individual customers. If they can demonstrate that they have abundant resources to make such payments, this will give the market more confidence in their capacity to weather a crisis.

Regulators have long been aware of clearing houses’ vulnerabilities. Last year, the Financial Stability Board, established in the wake of the 2008 crisis to set global standards, indicated that it was finally ready to address them. It should do so without further delay. Otherwise a promising reform may be rendered useless, or worse, when the next crisis comes.

Editorials are written by the Bloomberg Opinion editorial board.

©2019 Bloomberg L.P.