ECB Will Find It Hard to Match Intent With Action on Banks' Woes

ECB Gets Markets Excited About Tiering, But It's Complicated

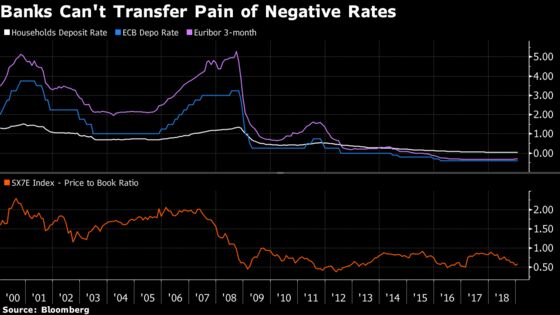

(Bloomberg) -- The risk that the European Central Bank will lose the ability to increase interest rates during the current business cycle is a challenge for bank profitability. The cumulative adverse effect of the ECB’s negative deposit rate is part of the reason why euro-area banks are trading at a low price-to-book ratio, but there is no easy solution.

Recent comments from ECB officials on mitigating the side effects of negative rates have got markets excited about the central bank potentially tiering rates by applying a zero rate to all, or some, excess reserves as opposed to the negative deposit rate. If it took such a step, investors may see it as a signal that policy rates will stay low for longer and give officials the scope to cut rates, further exacerbating the erosion of bank profitability in the long term.

However, the idea of tiering to ease pressure on bank earnings is limited given the potential savings may only amount to 7.3 billion euros (about 6 percent of euro-area bank profits), the annual cost of the 1.83 trillion euros of excess liquidity parked at the ECB. As a large share of that excess liquidity is from core countries, particularly Germany, any gain will be skewed toward them and certain banks within those nations.

Also, should the economic downturn significantly worsen, the extra boost to earnings will be more than wiped out as demand for loans will deteriorate.

- The key problem is that banks can’t apply negative rates to retail deposits as clients would withdraw funds and hold cash, with the gross nominal return of cash being zero; banks ultimately need Euribor to move back into positive territory

- As the impact of tiering is likely to be small, the ECB will likely continue to focus on its new TLTRO program for now to the benefit of banks in peripheral countries who have high borrowing needs and less deposits compared to banks in core countries; officials will want to prevent the design of the new loans signaling rates will be on hold for years

- Eonia forwards currently price the state-contingent element of forward guidance (“for as long as necessary”) as a 10bps hike by March 2021 and NIRP exit by late 2022

- The trade-off between helping the banking system while not indicating lower for longer rates in a limited policy space and avoiding criticism related to skew of who benefits from this will be extremely tricky to pull off

- NOTE: Tanvir Sandhu is a global interest-rate and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

To contact the reporter on this story: Tanvir Sandhu in London at tsandhu17@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Scott Hamilton

©2019 Bloomberg L.P.