Lyft Confirms What We Know and What We Don’t

Lyft Confirms What We Know and What We Don’t

(Bloomberg Opinion) -- Lyft Inc. on Friday gave the public its first look at its financial statements and vision for the future of transportation. While the specific figures may have been a surprise, the general trend was not: Lyft is growing rapidly and its losses are huge, although the company is showing improvement there.

Readers will naturally have two questions: How will Lyft do in its initial public offering? And will it capture a large and lasting share of what the company says is $1.2 trillion in U.S. spending on personal transportation?

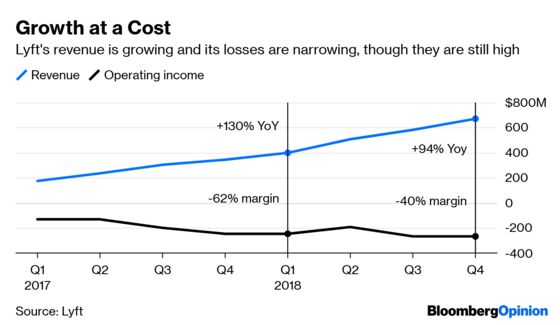

I suspect the answer to the first question is that Lyft’s IPO will do fine. Investors are hungry for growth, and Lyft’s revenue — the money it takes in from on-demand rides after paying the drivers — doubled to $2.2 billion in 2018. That growth rate is appealing, and stock buyers will most likely shrug off the bonfire that in the most recent three months amounted to an operating loss of 40 cents for each dollar of revenue. Growth is what matters now, and Lyft has it in spades.

As for the ultimate size and viability of Lyft in the transportation industry, there’s only a string of question marks — and that goes quadruple for the larger, more sprawling Uber Technologies Inc., which will also seek to go public soon. Before I read Lyft’s offering document, my biggest question was whether ride-hailing would be a financially viable business. After reading the filing, I was left wondering whether demand will ever be very large for this whole industry.

For Lyft lovers, there is plenty to be excited about in the company’s IPO document. And for pessimists, there are plenty of items that deserve frowning face emojis.

Optimists can point to the fast rate of growth, which has outpaced the rate of cost increases. The negative 40 percent operating margin was a drastic improvement from a negative 76 percent margin in early 2017. The company seems to be getting better efficiencies from some its spending, and that kind of operating leverage may eventually allow Lyft to generate tidy profits.

On the pessimistic side, I was surprised at the scale of Lyft’s costs for items like insurance, credit-card payments and expenses to run its technology systems. Those costs eat up more than half of Lyft’s reported revenue, and it shows that on-demand rides may never have the type of high-margin profits that investors love in internet and software companies. This is a company that doesn’t have to spend to produce a physical product yet has the gross margins of a clothing retailer.

And so far, the number of Lyft users is relatively small. The company said 18.6 million people in the fourth quarter took at least one ride in Lyft’s cars, scooters or other transportation provided through its smartphone app. The growth in the number of riders is slowing significantly. The rate of increase was 7 percent in the fourth quarter compared with the prior three months, and 21 percent in early 2017. For the optimists, that is just more opportunity for growth. But for comparison, about the same number of people bought a smartwatch in the fourth quarter, and that’s a bigger commitment than taking a Lyft once every three months. The growth rate of smartwatch sales was also faster than the rate of increase in active Lyft riders.

The company in its IPO pitch is stressing the size of the transportation market in the U.S., including personal car ownership, public transit and corporate and university shuttle services. It’s clear Lyft wants investors to see it as a future substitute for owning cars, and in that context, Lyft has a huge runway.

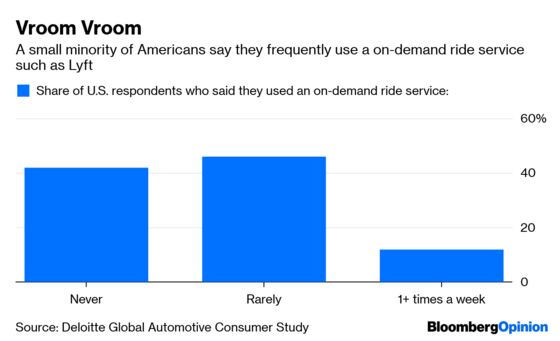

But for me, this is the biggest unknown about Uber and Lyft: How big is this market? About 12 percent of people in a recent Deloitte survey said they use on-demand ride services such as Lyft at least once a week. That number decreased from an earlier survey. That relatively small share is either good news — Lyft and Uber have a large untapped market particularly outside of big cities — or a sign that even with the oodles of money that Lyft and Uber spend on subsidizing fares and marketing to attract drivers, the natural demand for on-demand rides isn’t that big.

Broadly, Lyft and Uber are the first big test of a defining trend of the last decade in technology: Startups that created consumer demand for a product with heavy subsidies provided by investors.

If you’ve taken a Lyft or Uber ride recently, thank your local venture capital investor. Uber and Lyft would not exist without the nearly free and endless capital available in the last decade for young companies to create novel businesses — on-demand rides, restaurant food delivered at the push of a smartphone button, rented scooters on every street corner, low-cost video entertainment and rented office space.

Consumers have embraced those and other new services because they are genuinely useful. They may also be a mirage fueled by cheap capital that made those innovations possible at an affordable price to the masses. We may not know for sure for years, and Lyft’s IPO filing pours gasoline on that fiery debate rather than douses it.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.