Italy's Credibility in Doubt as Pimco, Aberdeen Dodge Bonds

Italy's Credibility in Doubt as Pimco, Aberdeen Dodge Bonds

(Bloomberg) -- The bond market is taking the Italian government’s promise to respect the European Union’s fiscal rules with a pinch of salt.

Even if Rome projects a deficit within the bloc’s 3 percent limit in budget proposals due before Thursday, investors will be combing through the details to see if that is supported by underlying growth assumptions. Pacific Investment Management Co. and Aberdeen Standard Investments are staying either short or underweight on Italy’s debt, while Societe Generale SA recommends investors position for a sell-off over the next two weeks, after this month’s rally.

“The devil will need to be in the detail,” said James Athey, a money manager at Aberdeen. “There may have to be heroic growth or revenue collection assumptions in there.”

While reassuring rhetoric from the Five Star Movement-League coalition helped Italian 10-year yields drop by around 40 basis points this month, there are signs of growing rifts within government about what the spending priorities should be. Five Star chief Luigi Di Maio has insisted room should be made for his party’s pledges on basic income, putting him at odds with League leader Matteo Salvini and Finance Minister Giovanni Tria.

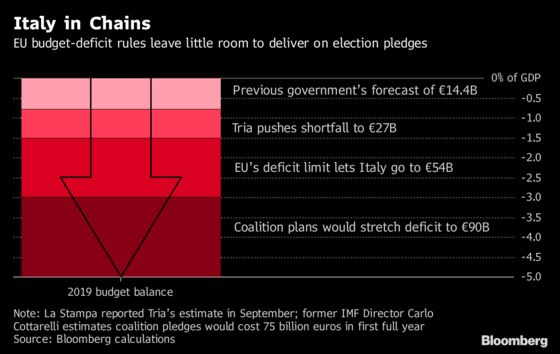

Italy’s La Repubblica newspaper reported at the weekend that Five Star seeks a deficit of 2.6 percent of the size of the economy, while Tria refuses to go higher than 2 percent and Salvini is not opposed to a level above 1.6 percent. Di Maio said Monday that provisions for the citizen’s income would be in the budget law.

A market-friendly deficit projection, most likely below 2 percent of gross domestic product, may prompt a rally in Italian bonds in the short term, but the troubling debt dynamics still remain and volatility will stay elevated, according to Pimco money manager Andrew Balls. Italy’s debt currently stands at over 130 percent of GDP.

“You should have more risk premium in Italy,” Balls told Bloomberg Television. “The longer-term issues are quite serious and so as a long-term investor you should be very careful on Italy. And you don’t get paid that much -- you can buy a U.S. Treasury for a similar yield.”

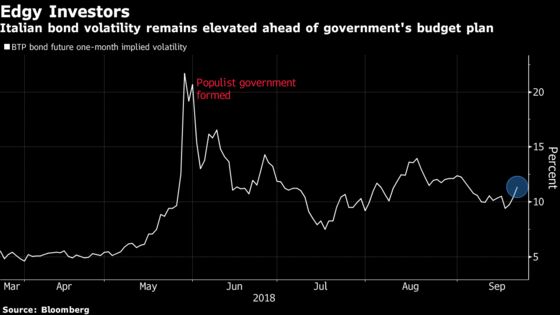

Italy’s 10-year bond yield rose 12 basis points to 2.95 percent, with the spread over their German peers at 243 basis points. The yield surged as high as 3.44 percent in late May amid the political imbroglio around forming a populist government.

It’s not only investors who will be scrutinizing the government’s spending plans. The EU will give its verdict on the budget by Nov. 30, potentially setting the stage for further conflict between the bloc and its fourth-largest economy. Furthermore, credit rating agencies S&P Global Ratings and Moody’s Investors Service are due to review Italy’s ratings in the next couple of months. Moody’s has kept the nation on a negative watch.

“If the present government hangs onto power, and if the budget deficit is announced at 1.8 percent and even viewed as such by the EC, we still see Moody’s downgrading Italy,” Societe Generale strategists led by Ciaran O’Hagan wrote in a note. Such a “budget outcome would be the best we can hope for at present, but it would still not be good enough to keep the agencies from acting.”

--With assistance from Zoe Schneeweiss.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Anil Varma, Neil Chatterjee

©2018 Bloomberg L.P.