Comcast Breaches Pain Barrier to Top Fox for Sky

Comcast Breaches Pain Barrier to Top Fox for Sky

(Bloomberg Opinion) -- Comcast Corp.'s victory over Rupert Murdoch's 21st Century Fox Inc. in the battle for satellite broadcaster Sky Plc has been dearly won. A trophy asset has commanded a trophy price. Yet it's still unclear whether the cable and entertainment giant led by Brian Roberts can secure a clean deal.

Saturday saw Comcast outbid Fox in a regulated auction by offering about 30 billion pounds ($40 billion) for Sky. The 17.28 pounds-a-share offer will now be put to the U.K. group’s shareholders — including Fox itself, which already owns 39 percent.

Comcast had to put clear water between its offer and what it thought Fox, backed by partner Walt Disney Co., might bid. With a big stake, Fox needed only to win over a few shareholders to get to a 50 percent controlling position. It submitted 15.67 pounds a share.

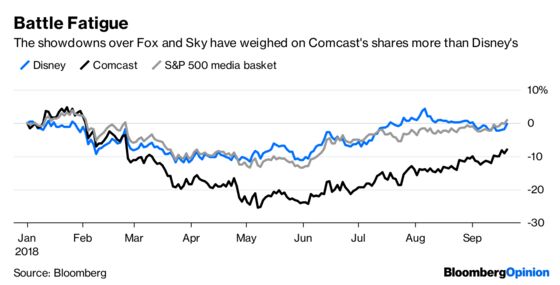

Even so, the winning price is jaw-dropping. The risk of overpaying for Sky in a deal that may not even result in full ownership has unnerved Roberts' investors since his ambition emerged in February. A failed attempt to stop Disney's acquisition of Fox's entertainment business left Sky looking like a more necessary consolidation prize.

Shareholders are used to the splashy deals for Hollywood studios and popular TV content that have punctuated the U.S. mergers and acquisition market this year. But the strategic logic of owning Sky is clear. The company offers Comcast 23 million households in a European pay-TV market that is less mature than in the U.S., where Netflix has been gobbling up subscribers. And Sky has shown it can fight back against the streamers.

Can Roberts get Fox (and Disney) to sell its Sky holding to his bid? Logic suggests it should be a seller at Comcast's considerably more generous price. But Fox and Disney might see the blocking stake as leverage over Comcast to force other deals — for example, Comcast's 30 percent share of the Hulu video service, in which Disney and Fox are also partners. Whether that prospect is worth more than $16 billion of cash from selling the stake is another matter. Fox said Saturday evening that it’s mulling its options.

Roberts has his work cut out making this pay. The offer values Sky at $48 billion including assumed net debt, or 15 times the expected Ebitda for its current fiscal year. That compares with a valuation multiple of just 8 times for Comcast. Unless Comcast can magic up higher synergies than previously stated, or Sky performs vastly better than envisaged, earning reasonable returns is going to take more than three years. That goes against the indications Comcast gave when it first came forward with a far lower opening bid. Moreover, it's not certain those synergies can be extracted if Comcast doesn't get to full control.

The stretching of Comcast's balance sheet closes off other acquisition opportunities. Net debt will exceed 3 times this year's estimated Ebitda if Comcast shells out for 100 percent.

Roberts's biggest achievement is to have prevented Fox, and suitor Disney, from owning Sky. That is meaningful: There is simply no comparable growth platform for either Comcast or Disney. Buying Sky would have given Disney an instant strategy for going global and building a direct-to-consumer business.

The only clear winners are Sky's shareholders. The U.K. takeover regulator has certainly protected their interest, as is its job. That said, Britons may have to get used to seeing top U.K. companies fall to foreign offers, given how sterling’s weakness since the Brexit referendum has made them more affordable.

Roberts has got a deal that was almost impossible to contemplate scarcely 10 months ago. There is only one Sky and control will be his. But he has pushed shareholders through the pain barrier to get it.

—With assistance from Bloomberg Opinion’s Tara Lachapelle

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2018 Bloomberg L.P.