Biggest U.S. Premium Over Europe Since '80s Fails to Help Dollar

Biggest U.S. Premium Over Europe Since '80s Fails to Help Dollar

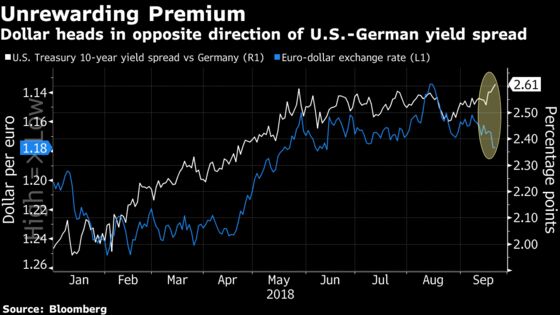

(Bloomberg) -- Not since the 1980s have U.S. Treasuries had such handsome yield premiums over their German counterparts. Yet none of that widening advantage in recent weeks has helped the dollar, in a disconnect that’s catching analysts’ attention.

Prospects for central bank tightening, emergent inflation and solid growth have boosted government bond yields across developed markets this month -- but particularly in the U.S., where the 10-year spread over German bunds now exceeds 2.6 percentage points. Wider gaps were only seen in the late 1970s and 1980s, when American inflation averaged 3 percentage points higher than in Germany (versus little difference now), Commerzbank AG says.

Part of the dollar’s recent weakness has been explained by a resumption of demand for risky assets, with China declaring that it won’t devalue the yuan and some fund managers saying it’s time to dive back into the likes of Argentina and Turkey. The risk-on sentiment has undermined demand for the greenback as a haven. That could also explain why the yen, another haven asset, has been the only major currency to drop against the dollar this month.

But when it comes to the dollar’s retreat against the rest of the key developed-market currencies, some are reading a deeper underlying challenge: diminished appetite for U.S. assets as American fiscal and current-account deficits widen.

“Widening dollar-supportive yield differentials should be seen in the context of rising capital import needs. We believe the current yield compensation offered by the U.S. is no longer adequate to attract sufficient foreign funds to cover U.S. capital-import needs,” Morgan Stanley currency strategists led by Hans Redeker wrote in a Sept. 20 note. “The dollar has to decline to attract international funds to the U.S.”

Indeed, private domestic investors have had to take up a bigger share of U.S. debt as the Federal Reserve draws down its holdings through the unwinding of quantitative easing. U.S. Treasury data show the smallest share of overseas holdings since 2003.

Some analysts say there’s nothing sinister about the dollar’s retreat against European currencies -- it may just be a reflection of traders increasingly anticipating monetary-policy normalization on the continent, and the currently high hedging costs associated with buying Treasuries.

“That’s a backstory that we need to keep an eye on,” Gavin Friend, a senior markets strategist at National Australia Bank in London, says of the rotation from foreign to domestic buyers of Treasuries. He highlighted in a podcast this week, though, that policy makers in other developed markets are growing confident their own economies are picking up steam. That means “it’s getting to the time to wind back slowly on some of their very accommodative monetary policies.”

Among the recent shifts across the G-10 currencies:

- Norway’s central bank hiked interest rates on Thursday for the first time in seven years

- Inflation in the United Kingdom rose 2.7 percent year-on-year in August, above the market estimate and the Bank of England’s 2 percent target

- New Zealand reported gross domestic product of 2.8 percent for the second quarter which beat analysts’ expectations, lifting the Kiwi dollar

- Sweden’s Riksbank has primed the market to expect interest rates, giving a boost to the krona

- The European Central Bank gave further forward guidance as it tapers asset purchases

The link between the dollar and Treasury yields could reassert itself as the Fed’s next moves become clearer, said Maoko Ishikawa, a currency strategist at JPMorgan Chase & Co. in Tokyo. “Once people have started pricing in next year’s hikes, we might see some stronger correlations at the end of this year.”

Deficit Dynamics

Yet the prospect of the twin American deficits diminishing the appeal of higher-yielding Treasuries looms large in the minds of some, given the historic anomaly between an expanding economy and widening fiscal borrowing.

Louis Gave, a founding partner of Gavekal Research in Hong Kong, sees one of three scenarios for the recent pick-up in U.S. yields. The first two: accelerating growth and rising inflationary pressures.

“The final explanation is that investors are starting to worry about U.S. deficits and debt,” which “certainly explains why the dollar has failed to break out on the upside” lately, Gave wrote in a note Friday. “Needless to say, of the three scenarios, the third might well have both the highest odds, and the least-attractive long-term investment consequences.”

To contact the reporters on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net;Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Anil Varma

©2018 Bloomberg L.P.