Lehman’s Fall Cast a Long, Risky Banking Shadow

Lehman’s Fall Cast a Long, Risky Banking Shadow

(Bloomberg Opinion) -- Bloomberg Opinion marks the 10th anniversary of Lehman’s bankruptcy with a collection of columns from around the world. Read more.

Ten years after the credit crisis sparked by the collapse of Lehman Brothers Holdings Inc., many argue that a combination of lessons learned and regulations have made the banks far safer from collapse than they have ever been.

However, a growing portion of the financial ecosystem, in both size and importance, has moved into the shadows where there is neither transparency nor regulation. Oddly, this is by design in part. One of the main goals of the regulations that emerged in the wake of the financial crisis — the Dodd-Frank financial overhaul law and others — was to prevent bank failures by barring the biggest ones from the riskiest types of trading and lending, relegating that business to a tier of financial firms thought to be too small to matter.

And it worked. A decade later, that business has exploded. Worse, the market is just as opaque, and potentially destabilizing, as the ecosystem of over-the-counter derivatives that hid trillions of dollars of toxic loans in the run-up to the financial crisis.

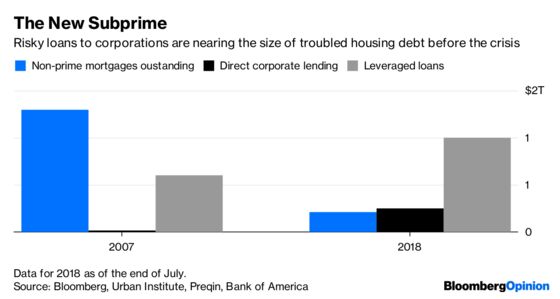

Consider direct lending, one of the hottest areas on Wall Street right now. At the end of 2007, when Lehman was still alive but coming undone like the rest of the financial sector, the total amount lent by nonbanks was small, perhaps a few billion dollars. Now, private equity, hedge funds and other specialty firms are racing to launch to vehicles that lend directly to highly leveraged, lower-credit quality companies, often to fund buyouts.

Investors, seeing double digit returns, want in. The largest players in this market — Ares Management, HPS Investment Partners, and Golub Capital — have more than $20 billion each, and single loans can top $1 billion. In all the private debt market, which includes distressed debt and special situation funds, as well as direct lending, has reached $754 billion, according to fund research firm Preqin. Direct lending is about a third of that but it is the fastest growing part, attracting $45 billion in additional investments so far this year.

That’s still much smaller than the more than $10 trillion in housing debt Americans had a decade ago. But the subprime portion of that, the main culprit in the housing crisis, was only $1.3 trillion, though that doesn’t include all the derivative investments, like synthetic CDOs, that were tied to those risky mortgages and amplified the problems. But like subprime mortgages, direct lending is just a portion of the much bigger leveraged-finance market, which includes $1 trillion in leveraged loans as well as another $1.1 trillion in high-yield debt, according an analysis earlier this year by Bank of America.

What’s more, embedded in the system is debt on top of debt. Many of these direct lending funds are leveraged at least one time, and some more. A survey last year by the Alternative Credit Council, a trade group, found that 10 percent of private debt funds were levered 1.5 times or more, and some were levered as much as 10 times. Nine percent of the managers answered “prefer not to disclose,” underscoring how little is known about this market. And that’s of funds, not of assets. That means an additional $250 billion, and possibly more, of assets in direct lending are backed by the too-big-to-fail banks, which are the primary lenders to fund companies and the ones that regulators wanted out of this segment of the loan market.

Those loans are most likely less risky than if the big banks were lending directly to levered companies. But banks themselves have trillions of dollars in commercial loans. And losses from lending to the funds could materialize at the same time the banks are facing losses in their corporate lending portfolios. What’s more, banks are required to hold less capital against loans to funds to cover losses than they are as the direct lenders — even when the end borrower is the same.

Nevertheless, managers of the large direct-lending firms say that they are more stable than when the banks were making similar loans. That’s because banks mostly fund their loans with deposits that can be withdrawn at any time. Many — though not all — of the direct-lending funds have lockups, meaning their investors can’t withdraw their money. But when there are losses, the big banks that have lent money to the funds can call those loans. And, unlike bonds, there is no public market to buy and sell the loans they have made. At times of stress, the funds will most likely have to sell their loans at deep discounts, causing large losses.

This might all be fine if the underlying loans that these direct funds make looked sound. But they increasingly don’t. The covenants that protect lenders have mostly disappeared. What’s more, a number of credit raters have warned that the loans have taken the place of bonds, meaning they could take the first losses if companies have trouble paying back their debt. On top of that, those double-digit returns that direct-lending funds are claiming are mostly a mirage, juiced by the leverage they have taken out from the banks. Data on unleveraged returns from investing in private loans are hard to come by.

Oaktree, a distressed debt investor and one of the earliest direct lenders, has recently been warning that the loans in the direct market look stretched. “It’s similar to trends we saw before the financial crisis,” said Edgar Lee, CEO of Oaktree Strategic Income Corp. and Oaktree Specialty Lending Corp. Lee says in the deals he has seen it has been more common for companies to borrow up to six times their cash flow. But that cash flow is often adjusted. On an unadjusted basis, Lee said, the leverage could be double that. But how much the average company is leveraged in the direct loan market, or how much debt the funds have piled onto those loans, and from where, is impossible for even Lee to say. These are private loans to private companies, by shadow lenders. No one really has the data to measure the size of these debt holes, or where they lead. All anyone knows is that they are far larger, and darker, than they used to be.

The financial crisis made two huge problems clear. The too-big-to-fail banks, through enhanced scrutiny and regulation, no doubt pose much less risk to the financial system than they did before the crisis. But what the crisis should have also taught us was that what you can’t see in financial markets is what can truly hurt you. The next crisis will more than likely be born in the dark. Perhaps we will learn the lesson the next time around.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2018 Bloomberg L.P.