ADVERTISEMENT

Bearish Euro Duration Proxies May Mitigate Pyramid of Risks

Bearish German Duration Proxies May Mitigate Pyramid of Risks

22 Aug 2018, 08:27 PM IST

(Bloomberg) -- German bunds’ stability and tight trading range is highlighting a sense of balance in the market. While duration has been supported given the negative macro backdrop, investors should be vigilant of signs of extreme pessimism and valuations.

- Payer spreads on 10y rates may be effective for those who expect to see a limited sell-off and wish to remain protected in a rally given that downside risks cloud the outlook

- EGB supply should push yields higher with gross issuance starting to increase as volumes rise from summer lows, while safety demand decreases with EM and BTPs stabilizing for now

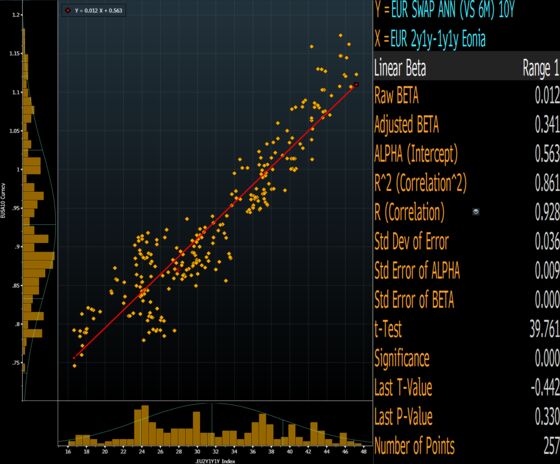

- Path to higher 10y yields is highly dependent on rate expectations high beta of 2y1y-1y1y slope to duration

- Benign ECB rate-hike expectations have pushed Euribors close to the highs seen in May and provide attractive risk-reward to any positive swing in sentiment via put spreads (see more here from Aug. 16)

- End-of-year forward rate for German 10y yield is only 6bps higher than spot, with the current yield having declined 32bps relative to what forwards were pricing at the end of last year

- Whether future rates go beyond current forwards is clearly dependent upon the pyramid of risks -- trade-war fears impacting on the capex cycle, EM stagflationary and contagion risks, Italy fragility -- as well as end-of-cycle U.S. pricing and negative spillover of restrictive Fed hikes to credit/stocks

- Short-dated EUR rates volatility has collapsed due to low delivered vol, low conviction levels and the predictable and cautious ECB approach, with program sellers harvesting residual gamma carry

- Italy remains a top global-risk factor with EUR 5y gamma having outperformed on the vol grid during the May ~20-sigma BTP sell-off (listed outperformed OTC equivalents given higher beta to risk-off)

- Indicates belly vol funded via 30y vol maybe an effective hedge against any BTP risk-off event, as well as Schatz swap-spread wideners which exhibit a positive convex profile to deterioration in risk sentiment and low-cost FRA/OIS wideners against debt crisis

- NOTE: Tanvir Sandhu is a global interest-rate and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

©2018 Bloomberg L.P.