Wall Street’s Latest Retail Product Pays Off Even if the Yield Curve Inverts

Wall Street’s Latest Retail Product Pays Off Even if the Yield Curve Inverts

(Bloomberg) -- Wall Street is pulling out all the stops to encourage retail investors to bet on the shape of the world’s largest debt market with their latest product.

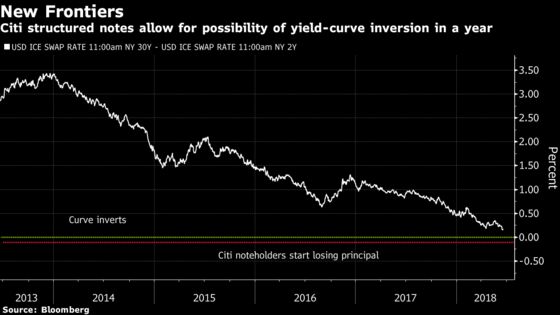

Citigroup Inc.’s one-year structured note provides a cushion for a looming inversion in the yield curve -- a sign investment banks are adjusting to a foreboding bond dynamic that has preceded the majority of U.S. recessions in recent decades.

In what appears to be a first for structured “steepener” products from a large U.S. issuer, holders of the $2.1 million notes sold late last month can redeem their full principal even if the curve starts to invert.

Typically, such a scenario would spark instant capital losses for investors in these types of securities, which allow high-net-worth individuals to make aggressive bets on the trajectory of U.S. interest rates.

The Treasury market remains decidedly flat, with the spread between two- and 30-year bonds at around 40 basis points, the kind of level last seen in 2007.

Strategists warn outright inversion is in the cards, with the Federal Reserve’s hiking cycle lifting short-end rates while muted inflation and strong demand anchor the long end.

With the Citi notes, the 30-year constant maturity swap rate can sink as much as 10 basis points below the two-year rate before holders start incurring losses. The products pay a coupon and return full principal as long as the spread remains greater than that level.

Flatter Future

Deutsche Bank AG sold similar notes in June but holders sacrificed principal as soon as short-term rates climbed above long-term ones.

Investment banks have issued steepener products in droves in recent years. Lenders may be able to offset some of the interest-rate risk they incur elsewhere in their businesses by selling such securities.

In normal circumstances, the higher longer-term yields are compared with short-term, the larger the coupon. After the curve turned the flattest in more than a decade, those notes have become somewhat less appealing, with coupons dropping to below 1 percent in some cases, decimating their value.

--With assistance from Sid Verma.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.