European Bond Markets Seen Resisting Contagion From Turkish Woes

European Bond Markets Seen Resisting Contagion From Turkish Woes

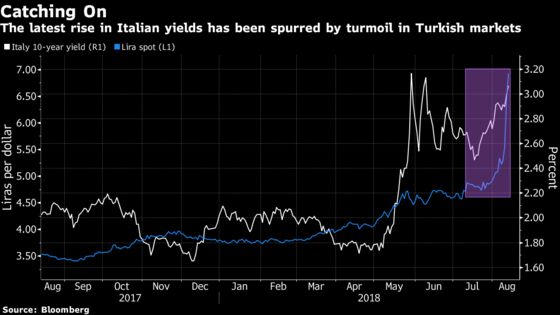

(Bloomberg) -- Fears about contagion from Turkish turmoil may be overblown for bonds in Europe.

While a slide in the lira prompted traders to shun the debt of Europe’s periphery from Portugal to Greece amid concern that banks may be exposed to Turkish assets, strategists see any spillover as limited. Politics is keeping Italy’s bonds risky, yet broader European exposure is likely to be mitigated by currency hedging and the improved health of the region’s lenders, according to Morgan Stanley and Danske Bank A/S.

“Right now markets are not differentiating a whole lot with players just trading what they can,” said Commerzbank AG’s head of fixed-rate strategy Christoph Rieger. “Fears about a systemic banking crisis should subside once visibility on banks’ exposure to Turkey improves.”

In Spain, 10-year yields also dropped after touching the highest levels since early June. Data from the Bank for International Settlements indicates Spanish banks are among the most exposed to Turkey’s market rout.

Here’s what analysts said about the risk premium in euro-area bond markets:

Morgan Stanley

- “Even though the magnitude of the exposure is not yet a concern to the ECB, it does bring markets’ attention to contagion channels across asset classes given the recent EM wobble,” wrote strategist Elaine Lin in a note to clients

- French and Spanish banks most exposed, but European institutions generally hedge against currency depreciation, which means net exposure will be smaller

- The bank is bearish on buying BTPs in medium term unless political risks de-escalate significantly, despite possibility of a short-term rally once the budget risk is out of the way

Mizuho International Plc

- “The situation in Turkey can be damaging -- through the banks and the potential economic slowdown,” says strategist Antoine Bouvet

- “If sentiment toward other EM does not improve than we should continue to see EGBs reflecting a risk premium from other markets”

- “This should allow bunds to cling onto expensive valuations, while appetite to buy the most volatile EGB market, BTPs, should remain limited”

- “After the widening of BTP spreads since May, Italian banks would be the most vulnerable to any further losses on their Turkish exposure. This is as far as direct links are concerned”

- For risk-off trades, likes BTP curve flatteners and France-Germany tighteners; if sentiment toward Turkey improves, sees the yield pick-up offered by France as becoming attractive

Danske Bank

- Spanish banking exposure to Turkey is only around two percent of total assets, while in France and Italy it is closer to 0.5 percent, say strategists Arne Lohmann Rasmussen and Aila Mihr

- The follow through to Spain will be especially limited “because the Spanish banks macro fundamentals in general have improved significantly the last couple of years”

- “BTPs are exposed in the current environment as the weak link, but it has more to do with risk sentiment impact than direct exposure to Turkey”

- Recommends buying Spanish bonds and finds two-year Italy attractive in valuations versus similar-dated Spanish and Portuguese bonds

Commerzbank

- “The banking risk seems to be concentrated in just a few names,” so unless there is a reaction in other emerging markets, fears should subside, says Rieger

- “The risk-off related FRA-OIS widening has taken 2019 expiry Euribor futures to interesting levels”

- “I don’t think the liquidity and credit situation would warrant an increase in Euribor fixings as implied by forwards”

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee, Benjamin Purvis

©2018 Bloomberg L.P.