Puerto Rico’s Biggest Bond Challenge Is Yet to Come

Puerto Rico’s Biggest Bond Challenge Is Yet to Come

(Bloomberg Opinion) -- Puerto Rico has been gradually moving along with its debt-restructuring efforts for months. On Wednesday, the beleaguered commonwealth took a big leap forward, announcing a deal with its sales-tax bondholders.

Make no mistake: This is a significant step. Investors in the bonds, known by the Spanish acronym Cofina, have more money at stake than any of the other groups of creditors that have come to an agreement with Puerto Rico. According to Governor Ricardo Rossello, the deal would save the commonwealth $17.5 billion in interest payments over the life of the securities. While that sounds like a victory, bondholders come out quite nicely, too. Owners of senior Cofinas, with the highest claim on sales taxes, would recoup 93 percent of their investment, while subordinated securities get a 56 percent recovery.

That’s way better than what the market was indicating (the bonds soared in price Thursday). And for the senior Cofinas, which traded at less than 40 cents on the dollar at the start of the year, it’s an even bigger windfall than what Moody’s Investors Service thought way back in July 2015. The credit rater set the expected recovery rate at 65 percent to 80 percent.

Nothing is easy when it comes to Puerto Rico. By all accounts, this was a hard-fought compromise. It’s the second significant deal for the island in as many weeks, following an agreement with its power company’s bondholders in late July.

But the most-scrutinized deal for the commonwealth — and the $3.8 trillion municipal market as a whole — is still to come.

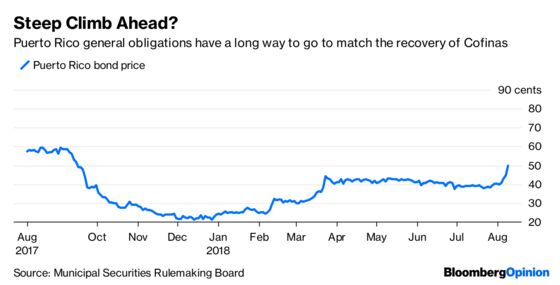

The fate of Puerto Rico’s roughly $18 billion general-obligation bonds, backed by the island’s full faith and credit, remains firmly in limbo. In theory, because Cofina securities will now have the first right to 53.65 percent of collected sales taxes, that should free up cash for G.O. debt. Court documents filed in June essentially said as much, adding that the extra funds could also cover essential services.

It’s telling, though, that Puerto Rico’s benchmark general-obligation bond is still trading at 50 cents. On the one hand, that’s the highest price since Hurricane Maria devastated the island more than 10 months ago. But for debt that’s perceived to have at least equal standing to senior Cofinas, it has an awfully long way to go to catch up to the announced recovery rate.

It speaks to the uncertainty around what a general-obligation pledge means in times of deep distress. In Detroit, holders of “unlimited-tax” G.O. debt received 74 cents, while “limited-tax” G.O. bonds recovered 34 percent. There really isn’t a robust playbook.

Many investors in Puerto Rico counted on two things. First, the commonwealth’s constitution, which guaranteed G.O. payments before all else. But in reality, elected officials were always going to provide essential services to its citizens before accommodating Wall Street. Second, that the territory couldn’t file for bankruptcy protection and potentially cram down a debt deal. That didn’t last, either.

The past year of ultra-depressed prices gives Puerto Rico an advantage. My Bloomberg Opinion colleague Joe Nocera wrote recently about Aurelius Capital Management LLP, which owns $558 million of Puerto Rico’s general obligation bonds and wants to get paid in full. But would Mark Brodsky — or any investor, for that matter — really quibble with a 93 percent recovery, like the senior Cofinas? Remember, the benchmark debt was issued in March 2014 at precisely 93 cents on the dollar.

General obligations have always had one chief flaw: there’s no clear revenue steam for investors to point to and claim as their own. By contrast, Cofina investors will have a senior lien on the agreed upon portion of sales taxes. A term sheet from Citigroup Inc. projects that revenue will cover debt service more than 2.6 times over, placing the bonds in a similar tier as double-A rated issuers like the Massachusetts School Building Authority and Utah Transit Authority.

The G.O. investors are going to want a similar deal, with all the legally enforceable structures they can get. Because for all the talk of recovery rates, Puerto Rico has a massive recovery of its own ahead. The commonwealth just now conceded that Hurricane Maria killed more than 1,400 people on the island last year, far greater than the 64 in the official death toll. Add that to the mass population exodus that was already taking place, and there’s no guarantee that projections about the commonwealth’s future will pan out.

In that sense, it seems comparatively easy to dole out various revenue streams. But judging how much Puerto Rico’s full faith and credit is worth, after the constitutional guarantee was all but eviscerated? That will be the biggest challenge yet.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.