Morgan Stanley Goes Against the Crowd on JGBs

Morgan Stanley Goes Against the Crowd on JGBs

(Bloomberg) -- As most strategists bet that Japan’s bond traders will push the benchmark yield toward 0.2 percent in a bid to test the central bank’s newly-guided boundaries, Morgan Stanley MUFG Securities Co.’s Koichi Sugisaki is going against the crowd.

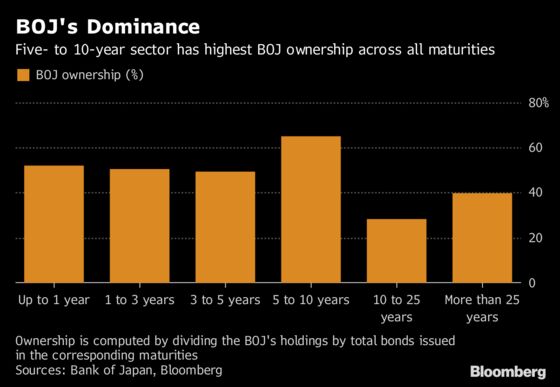

The 10-year yield will probably settle closer to 0.1 percent -- the upper end of the Bank of Japan’s previously acceptable range -- as recent market volatility settles down to less extreme levels, according to Sugisaki, who cites the surge in the central bank’s ownership of five-to-10 year debt as a key reason for the contrarian call.

“The 10-year yield of reaching 0.2 percent can’t be justified under Japan’s current negative rate policy and the fact that the BOJ is holding more JGBs in the 10-year zone than in the past," Sugisaki, a strategist at Morgan Stanley MUFG in Tokyo, said in an interview.

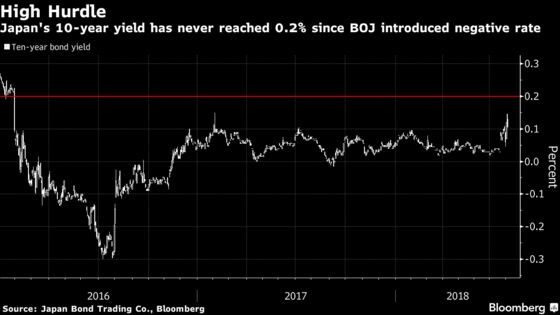

The central bank’s relentless buying of bonds has meant that it owns about 65 percent of all outstanding five-to-10 year securities -- the highest among all the maturity zones -- squeezing supply of the notes in the market. The 10-year yield hasn’t traded at 0.2 percent since January 2016, when the BOJ adopted its negative rate policy. The central bank owned just 40 percent of the above debt back then.

Volatility in Japan’s bond market has picked up as BOJ Governor Haruhiko Kuroda said last week that authorities will allow the 10-year yield to deviate as much as 0.2 percentage points either side of its zero percent target. In a test of the BOJ’s patience, traders pushed the benchmark to an 18-month high of 0.145 percent on Thursday, triggering a surprise bond-buying operation by central bank.

“Many people instantaneously and reflectively sold JGBs as they didn’t know where the fair value of the 10-year yield was after the BOJ expanded the range," Sugisaki said. But the BOJ’s bond purchase has given reassurance to the market that the central bank will act to stem the rates from climbing sharply, he said.

His views are at odds with strategists at SMBC Nikko Securities Inc. and Barclays Securities Japan Ltd., who see the possibility of the 10-year yield testing the 0.2 percent level in the near term.

“We believe the 10-year yield will likely test the upper bound of the new range in the near term, i.e., exploring the next level at which the BOJ will step in with a fixed-rate purchase operation,” Shinichiro Kadota, a senior foreign-exchange and yen-rates strategist at Barclays, wrote in a report.

However, Morgan Stanley MUFG’s Sugisaki expects the central bank to refrain from conducting a fixed-rate operation unless the yield climbs sharply in the short period, pointing to the BOJ’s policy statement where it indicated that it will act against any sharp movements in bond yields.

“A return to pre-2016 yield levels looks unlikely any time soon,” Sugisaki and Shoki Omori wrote in a report dated Aug. 3. “We find it hard to envisage the 10-year yield spending all that much time near 0.2 percent until and unless the BOJ sends some sort of clear signal that an exit from the negative interest rate policy might be imminent.”

To contact the reporters on this story: Chikafumi Hodo in Tokyo at chodo@bloomberg.net;Masaki Kondo in Singapore at mkondo3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Shikhar Balwani

©2018 Bloomberg L.P.