Value Stocks Come Roaring Back From the Dead

Value Stocks Come Roaring Back From the Dead

(Bloomberg) -- Cheap equities are in vogue at long last -- lending a helping hand to stock markets hit by the recent trials and tribulations of tech companies.

If economic growth and strong earnings redress its undervaluation, the investing style may rebound in earnest -- signaling there’s more juice left in the aging bull market.

But there’s a problem. Few can agree whether last week’s outperformance in the U.S. and Europe was a head fake or a sign of things to come.

In the bullish corner are the likes of JPMorgan Chase & Co.’s Marko Kolanovic and Dennis DeBusschere at Evercore ISI. They argue value has the potential to pick up the slack, as cracks emerge in momentum equities thanks to earnings disappointments from companies such as Facebook Inc. and Netflix Inc.

“Despite ebbing trade tensions, the economic backdrop remained positive last week supporting the continued outperformance of value,” DeBusschere, head of portfolio strategy, wrote in a Monday note. The sharp shift suggests a "meaningful rotation" out of momentum and into value is on the way, he said.

A market-neutral version of U.S. value outperformed momentum by 0.5 percentage points last week, the most in four months, data compiled by Bloomberg show. Meanwhile, momentum in Europe has declined 1 percent compared to a 0.1 percent value gain over the past week.

Still, one week of gains a trend does not make, particularly when you consider financials have the largest weighting in U.S. value. The recent bounce coincided with a steepening of the Treasury yield curve, which tends to boost net interest margins for banks. But that’s a situation few see enduring.

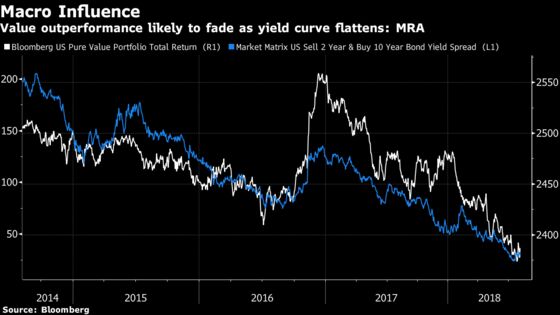

“We see a stronger macro case for the yield curve to continue its flattening trend which is likely to be a headwind for further value out performance if this relationship holds,” Mayank Seksaria, chief macro strategist at Macro Risk Advisors, wrote in a note.

On Monday the shift looked poised to slow, as U.S. momentum erased some of its losses while value was little changed. Morgan Stanley, for its part, sees room for cheap shares to power ahead, even as it warns the risks for a broad S&P correction have risen.

Over the past 15 years, the price-to-earnings gap between value and growth stocks has only been higher four percent of the time, according to data compiled by the bank.

Depressed valuations boost the appeal of value -- and the high price of growth leaves the group acutely vulnerable. Since the latter prices-in strong future earnings, signs the business cycle might be turning is decidedly problematic for the allocation strategy.

“Rising valuation dispersion suggests a better backdrop for value investing,” strategists headed by Matthew Garman wrote in a note.

To contact the reporter on this story: Dani Burger in London at dburger7@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.