Corporate Bonds are Finally Waking Up to Britain's Brexit Risks

Corporate Bonds are Finally Waking Up to Britain's Brexit Risks

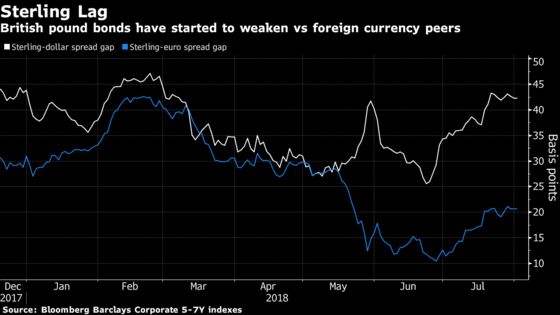

(Bloomberg) -- The U.K. credit market has begun to take notice of Brexit. Prices of corporate bonds in sterling have fallen behind similar euro and dollar securities as investors begin to price in the possibility of the U.K. crashing out of the European Union.

Investment-grade debt in pounds has failed to ride a credit rally in recent weeks, with spreads widening 3.5 basis points while comparable euro and dollar bonds tightened, data compiled by Bloomberg show, signaling investors are seeking a premium to hold sterling debt.

Concerns of a disorderly exit are growing after the U.K. government and the European Union brace for talks critical to the next stages of Brexit. The chance of the U.K. dropping out of the European Union without a deal is “uncomfortably high”, Bank of England governor Mark Carney said today, and there are just 11 weeks to go until a self-imposed deadline to get a divorce deal signed.

“Volatility in U.K. fixed income markets will soon return as the summer period ends, and the inevitable Brexit related headlines return,” said Mohammed Kazmi, portfolio manager at Union Bancaire Privee, which manages 125 billion Swiss francs ($126 billion) of assets.

The credit market is already digesting rising rates in the U.S. and the U.K., as well as the potential impact of imminent withdrawal of support from the European Central Bank. That’s added to a sense of fragility and greater sensitivity to political events.

“We believe it is increasingly prudent to follow a wait-and-see approach for sterling credit as the risk premium looks modest,” analysts at CreditSights Inc. wrote in a recent note. “There is a high likelihood of further political uncertainty driving market volatility over the months ahead.”

Supply shock

A disorderly exit would have a significant impact on U.K. borrowers such as manufacturers, but also on companies reliant on frictionless cross-border trade, such as food and beverage firms, and professional services, the CreditSights analysts wrote. A supply shock may also impact the pound, adding pressure for further rate rises and raising borrowing costs further.

Longer-dated sterling bonds may be most negatively affected by rising yields, according to Matthew Russell at M&G Investments, which manages around 350 billion pounds ($455 billion) of assets. U.K. credit has a longer duration than similar euro debt, Bloomberg Barclays benchmark index data show.

Overall for U.K. investment-grade credit, Russell calculated it would take a relatively small 34 basis-point rise in yields in wipe out returns for the next year, whereas for short-dated debt, which is less sensitive to interest-rate risk, yields would have to rise 96 basis points before returns were erased.

Sterling opportunity

Some sense opportunity amid the upcoming uncertainty. Gordon Shannon, portfolio manager at TwentyFour Asset Management, which has 13.5 billion pounds ($17.5 billion) of assets under management, has been buying some subordinated financial bonds, lured in by falls in prices.

Moreover, the U.K. credit market is seen as a safe haven by domestic investors, with inflows from retail funds this year totaling 1.7 billion pounds, according to data compiled by analysts at JPMorgan Chase & Co. That’s providing support for sterling debt, and helping encourage foreign and domestic borrowers to make forays into the market, with Goldman Sachs Group Inc. raising 1 billion pounds of bonds last month, its first public issue in the currency for more than four years.

Though their base case is for an agreement to be reached, analysts at JPMorgan estimate the probabilities of a ‘no deal’ Brexit at 20 percent. If such a scenario does emerge, “we expect domestic names to begin to price in a significantly higher risk premium”.

--With assistance from Emma Ross-Thomas.

To contact the reporter on this story: Tasos Vossos in London at tvossos@bloomberg.net

To contact the editors responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net, Tom Freke, Tasos Vossos

©2018 Bloomberg L.P.