Washington Nationals Win Fans in the Bond Market

Washington Nationals Win Fans in the Bond Market

(Bloomberg Opinion) -- The Washington Nationals may be having a down year by their current standards, but investors who bought their stadium bonds are winning more than ever.

The team is in third place in the National League East after finishing the past six seasons in either first or second. It’s been a dramatic turnaround for the former Montreal Expos, who played their first season in the U.S. capital in 2005 and failed to post a winning record until 2012. In the midst of that mediocre stretch, the District of Columbia issued $510 million in ballpark revenue bonds in May 2006.

At that time, the debt was rated BBB by S&P Global Ratings, just two steps above speculative grade. Analysts said the pledged tax revenue stream was highly dependent on stadium events. Or, as Bloomberg’s municipal-bond guru Joe Mysak put it in his column: Paying stadium bonds is easier if you score more runs. In offering documents, a revenue study made the assumption that “the future owner(s) of the team will strive to maintain a competitive ball club.”

Well, the Nationals have done more than just that, with winning records in each of the last six seasons. S&P has taken notice, raising its rating on the D.C. stadium bonds this week to A-, following an earlier upgrade in March 2016. Moody’s Investors Service has also boosted the debt since it was issued. That’s a boon for investors like Franklin Resources, which, according to Bloomberg data, has held about $29 million of the bonds since 2009, before the team’s fortunes changed. Invesco appears to have purchased about $31 million of the securities.

The backdrop of all this, of course, is that public funding for stadiums has become an anathema in recent years. Consider my Bloomberg Opinion colleague Barry Ritholtz’s column from last month, for instance:

Your tax dollars are being wasted, on an enormous scale, by uncompetitive socialist enterprises that ignore the basic rules of economics.

I refer, of course, to the practice of politicians who give taxpayer dollars to subsidize the business of sports by paying for the construction and/or renovation of stadiums and arenas. These exercises in crony capitalism make no sense whatsoever. There has never been a decent reason to subsidize these successful businesses, which rarely produce a real return on the public’s investment. Nor is civic pride a justification.

The way D.C. arranged to back the ballpark bonds is tame in comparison to some of the worst stadium deals. According to S&P, funds come from four sources: rent from the Nationals franchise; stadium taxes on tickets, food, beverages and parking; a utility tax; and a fee levied on businesses in the district that have $5 million or more in annual gross receipts. Largely, it comes down to the team’s performance and whether fans fill the seats.

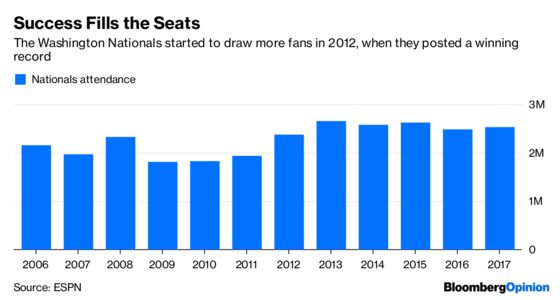

It’s clear that winning solves that issue, too. While attendance remained below 2 million from 2009 to 2011, it jumped to 2.37 million in 2012, when the Nationals went 98-64 and finished first in their division. The team has gone on to average 2.57 million fans per year from 2013 to 2017.

Not all sports financing happens to coincide with a team’s turnaround. As Bloomberg News’s Amanda Albright reported earlier this week, ice rink projects are responsible for some of the rare defaults in the $3.8 trillion muni market precisely because they often depend on ticket sales and rental revenue to repay their debts. The Atlanta Braves have been known to rope small towns into bidding wars for their minor-league franchises. Sometimes, the cities pledge to cover shortfalls with their general fund revenue. That’s led to credit downgrades, not upgrades.

The upward trajectory of the ballpark bonds’ ratings, then, should be viewed in isolation, rather than as a verdict on stadium financing as a whole. As Mysak wrote in 2006, consultants concocted a chart of ballpark-related sales growth that “might be termed the ‘happily ever after’ projections.” Basically, that proceeds increase at a steady pace year after year.

Well, sometimes happily ever after comes true. “We base the upgrade on a track record of strong and stable revenues, well in excess of debt service, providing flexibility to prepay existing principal and resulting in improved coverage levels,” S&P analyst Timothy Barrett wrote in a July 31 report.

Indeed, a good chunk of the debt has already matured or D.C. has taken it out. More will be called at 100 cents on the dollar in a month (the securities are selected by lottery, according to Bloomberg). Even so, a smattering of bonds changed hands over the past two weeks at a price above par, speaking to investor demand.

The Nationals, meanwhile, enter the home stretch of the season five games behind the division-leading Philadelphia Phillies, and a similar distance from the top of the NL wild-card race. They’ve won twice this week at home, including a dominant 25-4 victory over the New York Mets that set a new team scoring record.

That kind of scoring will certainly keep the bond payments flowing.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.