Honey, I Shrunk Apple’s Profit Margins

(Bloomberg Opinion) -- Apple Inc. has been a profit geyser well before it was valued at the $1 trillion milestone the company reached on Thursday. Even Warren Buffett is impressed. “It is an unbelievable company,” the legendary investor and Apple stockholder said in May as he marveled that Apple earns almost twice as much as the second-most profitable company in the U.S.

Buffett is right. Apple reported $68 billion in profit before taxes and non-operating items in the last year. In distant second place is JPMorgan Chase & Co. with $39 billion in operating profit.

But this isn’t another tale of Apple’s impossible-to-believe profit power, because Apple isn’t the powerhouse that it used to be.

Apple is now a tale of incredibly shrinking profit margins. Apple generates less profit from each dollar of sales than it did in 2010, when it was worth one-quarter as much. Investors most likely won’t care as long as Apple keeps growing and as long as it continues to churn out eye-popping earnings on an absolute basis. But the slimming margins are a potential warning sign as Apple hits the $1 trillion mark, which reflects investor expectations of fat profits for years to come.

The biggest reason for the profit margin diet is Apple’s spending. Its operating costs have increased at twice the rate of revenue in the last five years, and the company doesn’t detail why. Growth is coming from different sources, too, notably iPhone price increases and sales of ancillary products. Those changes are giving Apple a fundamentally different financial look, and investors haven’t yet been forced to confront how much this altered Apple should be worth.

Even relative to other corporate titans, Apple has lost a step. Five years ago, Apple ranked 40th among companies in the S&P 500 Index by its annual operating profit margins, according to Bloomberg data. Now the company stands 113th. Apple is squeezing lower profits per dollar than the energy drink company Monster Beverage.

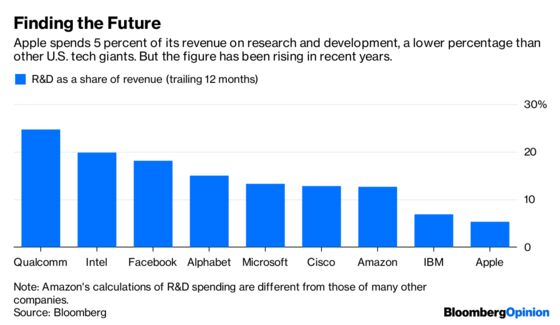

Five years ago, Apple was spending about $4 billion a year on research and development, or about 3 percent of its sales. On a percentage basis, that was far lower than other U.S. technology companies. In the last 12 months, Apple’s R&D spending amounted to 5.3 percent of its sales. While that’s still low by tech superstar standards, it’s a significant shift for Apple.

Steve Jobs once said that “innovation has nothing to do with how many R&D dollars you have.” Now it seems as if Apple is putting its foot on the R&D gas, hoping it will result in more innovation.

It’s true that technology investors want and expect technology companies to invest in the future. The U.S. technology titans are in an arms race, battling with engineer hiring and capital spending to build their capabilities in artificial intelligence, driverless cars, cloud computing and other areas they consider crucial to maintain and extend their dominance. In 2015, the investor Carl Icahn wrote that Apple’s rising R&D spending "should signal to investors that Apple plans to aggressively pursue" growth opportunities.

The problem is, it’s tough for outsiders to assess whether Apple’s climbing R&D spending is being put to good use. The company is notoriously, mostly understandably secretive about what it’s cooking up in its gadget labs. In the past, Apple has developed crucial innovations in-house, both highly visible ones like iPhones and iPads and less-celebrated innovations such as Apple's line of self-developed computer chips. Now the company may be splurging on areas such as health care, transportation, new forms of computing and more. It’s always tough to assess the return on R&D investment, and it’s doubly hard for Apple.

Apple’s rising research-and-development tab isn’t a problem now, and it may never be. The company has found clever ways to keep boosting its revenue even as smartphone sales stall across the industry. Apple’s profits and cash flow continue to pile up, and they are the envy of the corporate world.

When a company stumbles, however, spending that once seemed like the standard cost of doing business can come under a microscope. When an activist investor came after Qualcomm a few years ago, it questioned whether the chipmaker should cut its R&D spending to improve profits. If Apple hits a growth wall in coming years, it’s not hard to imagine the company facing similar calls to justify its climbing research-and-development bills.

There’s a disconnect between the investment narrative about Apple and its profit reality. Wall Street has been excited about the growing share of company revenue coming from its services segment, which includes app sales and Apple Music subscriptions. Those are billed as higher-margin businesses, but because of Apple’s spending the company’s margins have actually been decreasing. Even as investors stare at those 12 zeros in Apple’s market value, it’s tough to argue that the company deserves an even richer valuation, as long as those margins stay squeezed.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2018 Bloomberg L.P.