Volatility Is Back in Japan's Bonds as Traders Confront Kuroda

Volatility Is Back in Japan's Bonds as Traders Confront Kuroda

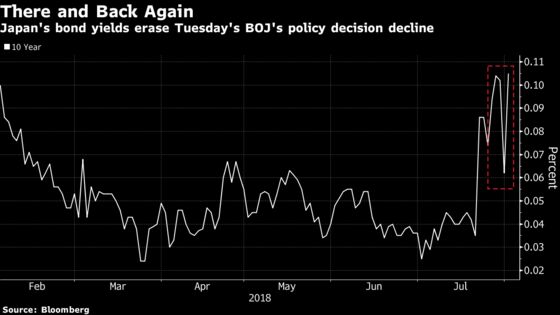

(Bloomberg) -- The day after Haruhiko Kuroda pledged to allow greater swings in Japan’s giant bond market while pushing back against rapid increases, traders are putting him to the test.

Moves in 10-year government debt futures were so extreme on Wednesday -- a drop of as much as 0.5 percent, the most in almost two years -- that they triggered an emergency margin call from the clearing house. In the cash market, the yield on benchmark securities rose 6 basis points to an 18-month high of 0.12 percent. And as of 2:45 p.m. in Tokyo, the Bank of Japan hadn’t announced a fixed-rate bond-buying operation that would help to cap yields.

The return of volatility is a welcome sight to traders in Japan, where unprecedented easing has created a market that’s heavily distorted by the central bank’s influence. Kuroda acknowledged that criticism on Tuesday and said that the BOJ will double the range allowed for the benchmark under its yield-curve control policy, signaling a tolerance for the yield to climb to about 0.2 percent. For global investors, that risks stoking higher borrowing costs across other debt markets, with 10-year Treasury yields edging closer to 3 percent on Wednesday.

“Markets are testing to see at which rate the BOJ will conduct a fixed-rate operation,” said Shinji Hiramatsu, general manager at the fixed-income investment department of Sompo Japan Nipponkoa Asset Management Co. in Tokyo. “If markets continue to try and push the 10-year yield to 0.15 percent, the BOJ would have to step in.”

Tuesday’s policy adjustments, made to help the BOJ sustain its monetary easing with its inflation target still far away, were seen giving Japan’s moribund debt market more breathing room. Traders are waiting to see how the central bank implements its changes through the conduct of fixed-rate operations whenever yields threaten to breach its control.

International bond traders are closely watching the rise in yields, given that Japanese investors hold $2.4 trillion of overseas debt. Speculation over BOJ policy helped shake Treasuries out of a tight trading range earlier in July, and the policy tweaks drove global yields lower Tuesday.

The slump in bond futures also triggered an emergency margin call by the Japan Securities Clearing Corp. As volatility increases, the chance of losses in a given asset are perceived to rise, so a clearing house may increase the collateral required by investors in order to continue trading.

BOJ Operations

The BOJ offered to buy an unlimited amount of bonds at a fixed rate three times in the week to July 30 as the 10-year yield rose to 0.11 percent. It bought a record 1.6 trillion yen ($14.3 billion) of 10-year debt at 0.1 percent at the last operation.

The policy tweaks suggest the BOJ may conduct fixed-rate operations at a higher yield level in the future, said Akio Kato, general manager of trading at Mitsubishi UFJ Kokusai Asset Management Co. in Tokyo. But he said it was unlikely for both bond traders and the central bank to immediately and sharply guide the level higher.

“With a clear nod from Kuroda, markets will naturally see 0.2 percent as an upper limit to the 10-year yield,” said Nobuyasu Atago, chief economist at Okasan Securities Co. and a former BOJ official. “Markets will test how high the yield could rise and what action the BOJ would take.”

Curve Impact

While the BOJ suggested it paid some consideration to the difficulties expressed by financial institutions, it made clear it is reinforcing its easy policy by introducing “forward guidance.” By explicitly citing it took into account uncertainties such as the effects of the consumption tax hike scheduled for October 2019, the central bank’s current policy bias will be maintained through 2019, Atago said.

That may shed light on where market players form a consensus for the benchmark yield.

“It will be a battle to see where the 10-year yield will settle,” said Satoshi Shimamura, head of rates and markets for investment strategy at MassMutual Life Insurance Co. “Allowing yields to swing puts them under upward pressure while the downside is now seen as zero. With 0.2 percent likely a top, the core 10-year yield may be around 0.10 percent.”

Higher yields may help steepen the curve and help mitigate pain for financial institutions suffering from dwindling income from securities holdings and lending due to ultra-low rates, but the new forward guidance could moderate the curve’s steepness, Shimamura said.

The spread between 10 and 20 year yields is usually around 50 to 55 basis points, so if the 10-year yield rises to around 0.2 percent at most, the maximum for 20-year yield would be around 0.75 percent, he said. A similar spread between 20 and 30 year yields is about 20 basis points, which would put the 30-year’s upper end around 0.95 percent, he added.

“If 30-year, and by extension 40-year yields approach 1 percent, some investors will be lured and the curve will flatten,” Shimamura said. “Steepening pressure is not so strong.”

To contact the reporter on this story: Chikako Mogi in Tokyo at cmogi@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen, Shikhar Balwani

©2018 Bloomberg L.P.