Deep in the CLO Machine, One Manager Sees a Warning Light

Deep in the CLO Machine, One Manager Sees a Warning Light Flash

(Bloomberg) -- Jim Schaeffer has found a glitch in his supply chain -- and reckons it could be an early warning sign that demand in the red-hot leveraged loan market is set to cool.

The deputy chief investment officer at Aegon Asset Management was collecting loans to create his firm’s next collateralized loan obligation. These are typically stored with a third party, which holds them on its books until there’s enough to bundle into a transaction. Yet when Schaeffer called on his usual warehouse providers, they were not keen to take on more exposure.

“The market of warehouse providers is not as receptive,” said Schaeffer, who helps oversee $103 billion of fixed-income assets. “That pause by warehouse providers is an indication that CLO demand could slow, which could impact the strong technicals we have experienced.”

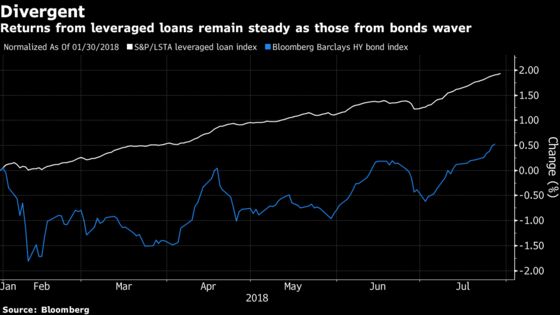

The technicals he’s referring to are in one of Wall Street’s hottest corners, the leveraged loan market. Issuance of these securities has been on a tear in 2018, in part fueled by the record rate of creation of CLOs, and so far the market has shown few signs of slowing. Even as U.S. rates rise and assets globally have been rattled by the threat of protectionism, the S&P/LSTA Leveraged Loan Price Index has declined just 0.2 percent over the past six months.

The question facing investors is whether Schaeffer’s supply-chain worry represents a temporary bottleneck -- perhaps caused by a flood of issuance in the thriving market -- or signifies a deeper shift in sentiment.

Growing Scrutiny

Leveraged loans are coming under increased scrutiny as investors ask how durable returns will be once growth slows and defaults start to pick up, how easy it will be to exit illiquid securities, and how steep a haircut they may have to take on any loans that sour.

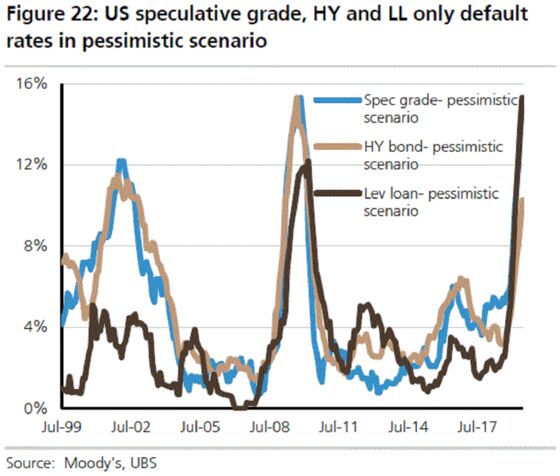

UBS Group AG and JPMorgan Chase & Co. are among those expressing uneasiness about how the assets will perform in the next default wave. In the worst case, UBS sees losses eclipsing those on bonds -- even though loans often rank above bonds in the pecking order of repayments.

JPMorgan strategists are puzzling over why loans are still attractive to investors who are bracing for tighter credit and a growth slowdown.

“While this makes sense for investors looking to insulate themselves from market volatility and higher rates, we think it’s a strange investment for those that genuinely worry about the end of the cycle and rising default risk,” strategists including Daniel Lamy wrote in a July 13 note.

Nonetheless demand remains robust, with $13 billion flowing to loan mutual funds and ETFs so far this year even as investors yanked cash from corporate bonds. New CLO issuance reached a first-half record of about $70 billion, and the likes of Wells Fargo expect the full-year tally to reach $150 billion, further supporting new loan issuance.

As a result of this demand, many of the safeguards typically offered investors by leveraged loans have been eroded. Moody’s Investors Service this month described the current level of protection as “distressingly weak.”

That may mean lower recovery rates than in previous default cycles, according to UBS. While the bank’s strategists don’t see trouble in the near term, they warn 100 basis points of Federal Reserve rate hikes through 2019 would expose “funding vulnerabilities.” They’re staying attuned to signs of weaker interest-coverage ratios that would point to stretched debt-servicing abilities.

Meanwhile, the booming supply has helped pivot the market in favor of buyers in recent months. A slew of borrowers have shelved refinancing efforts in the face of a swift change in sentiment among investors, who now appear ready to push back on opportunistic deals.

Triggers for the 2008 meltdown could be found in early signs warehouse providers -- anchor investors including banks or hedge funds -- were losing their appetite, Pimco portfolio manager Beth MacLean wrote in a 2014 report.

Whether or not that kind of sell-off is set to be replayed, Aegon’s Schaeffer sees the combination of deteriorating protection terms, an aging business cycle and now ebbing appetite from warehouses as reasons to lighten his firm’s exposure.

“In the first half of the year, we liked loans more than high-yield bonds, but in the second half we have some preference to high-yield bonds,” he said. “Although we do not think it will occur in the next year, these aggressive structures are sowing the seeds for the next defaults.”

--With assistance from Lisa Lee.

To contact the reporters on this story: Cecile Gutscher in London at cgutscher@bloomberg.net;Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.