Mortgage Trade Volume May Increase Regardless of FHFA Reform

Mortgage Trade Volume May Increase Regardless of FHFA Reform

(Bloomberg) -- The primary goal of the Federal Housing Finance Agency’s impending introduction of a Uniform MBS in June of 2019 is to boost mortgage trade liquidity, but that’s probably going to happen anyway.

It is likely -- UMBS or no UMBS -- that trade volume in mortgages will rise as the central bank continues to wind down its balance sheet, releasing more debt back into the channels of trading. This is already being seen year-to-date, according to Finra Trace data.

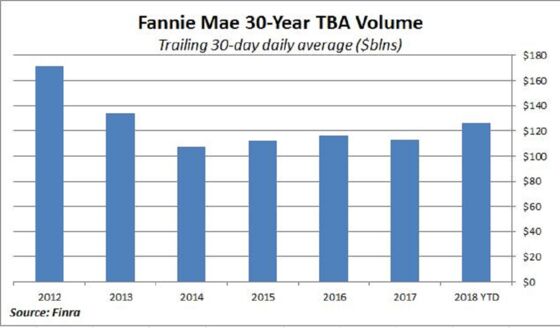

The Fed’s MBS holdings have dropped to $1.725 trillion from a high of $1.783 trillion in May of 2017, according to data compiled by Bloomberg. As more mortgage debt has been available to trade, volume has ticked backed up. The trailing 30-day average of daily Fannie Mae 30-year TBA trading has risen to $126.6 billion year-to-date, its highest level since 2013.

Granted, this volume is still 26 percent below 2012’s $171.3 billion average before the Fed started buying. Trading volume plunged the following year as the Fed began to purchase about $556 billion worth of agency MBS. The quantitative easing program grew to be so large that by May 2016 the Fed holdings of the 30-year outstanding MBS universe totaled 41 percent of Fannie Mae, 40 percent of Freddie Mac and 30 percent of Ginnie Mae II.

As more MBS are released back into the wild (consensus is for about $150 to $160 billion this year) private investors will need to absorb this roll off, which may pressure yields higher. Yet, in the long-run this may benefit those who need to borrow to purchase a home.

The logic goes: greater trade volume reduces liquidity risk, lowering the yield on MBS, and that should help American home buyers borrow at a lower mortgage rate.

To contact the reporter on this story: Christopher Maloney in New York at cmaloney16@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Tom Freke

©2018 Bloomberg L.P.