Draghi's View of Summer to Set the Mood for Markets at ECB Meet

Draghi's View of Summer to Set the Mood for Markets at ECB Meet

(Bloomberg) -- A holiday recovery for the euro may depend on European Central Bank President Mario Draghi’s definition of “summer.”

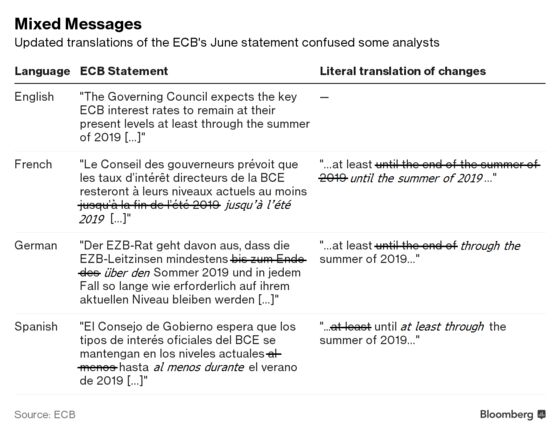

Market uncertainty over when the ECB will lift its deposit rate rests on the translation of the statement wording from its June gathering, which suggested the first hike since 2011 would not come until at least the end of summer next year. Yet in other languages such as French and German, it hinted it could come in June or July.

With money-market pricing suggesting traders don’t expect a deposit rate increase from minus 0.4 percent until at least December next year, any hint of sooner from Draghi at Thursday’s ECB meeting could boost the euro and depress government bonds. Investors will also focus on any comments surrounding a potential shift in reinvestments after the bank’s asset-purchase program ends this year.

“The translation issue is really the only significant issue this time around,” said Ned Rumpeltin, head of foreign-exchange strategy at Toronto-Dominion Bank. “All else being equal, any comments or clarifications we get this week from Draghi that have the net effect of pulling the timing of the ECB’s first rate hike forward should be a near-term positive for the euro.”

Here’s what analysts are expecting from the ECB’s July meeting:

Credit Agricole

- Market pricing for the first 15bps increase in the deposit rate in 2020 is “quite late,” says strategist Valentin Marinov

- There is a “risk that as Draghi reiterates the calendar guidance that rates will remain low through the summer of 2019, this would be perceived as implying an earlier move than priced in at present”

- Forecasts euro at $1.21 by year-end, though Thursday’s meeting may not move the currency meaningfully either way

Toronto-Dominion

- “The main item of contention we foresee -- the translation differences between the English and other language versions of last month’s statement -- could produce some intraday volatility in rates and FX markets during the session,” write strategists including Jacqui Douglas

- Euro likely to stay rangebound between $1.1510 and $1.1850, though sees the recent rally in bunds as overdone; recommends a short position in 10y bund real yields and 5s30s bund steepeners

- “Disappointment around any discussions of "operation twist" could support a steeper curve in our view”

BofAML

- “The ECB meeting could challenge the short positions in the very front-end and some of the flatteners in the very long-end initiated in anticipation of 2019 QE twist,” write strategists including Sphia Salim

- Still, “Draghi will present the exact timing of the rates lift-off next year and the intricacies of the reinvestment strategy as high-class problems, to be addressed at a later stage”

- Sees downside risks in the euro near-term with U.S. economic data remaining stronger than that in the euro zone; forecasts EUR/USD at $1.12 by the end of the third quarter

ABN Amro

- “Given that no rate hikes are priced in any case for the coming year, we do not expect to see a big impact on the short end from any ECB repricing,” writes strategist Nick Kounis

- Expects the ECB to raise its deposit rate by 10bps in December of next year, reflecting the likelihood that core inflation will undershoot the central bank’s forecasts

- “We should see 2s5s and 2s10s flattening over the next few months, while 10s30s should steepen”

--With assistance from Anooja Debnath and Carolynn Look.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee, Keith Jenkins

©2018 Bloomberg L.P.