Company Defaults Elusive as Credit Market Fragility in Focus

Company Defaults Elusive as Credit Market Worries Stack Up

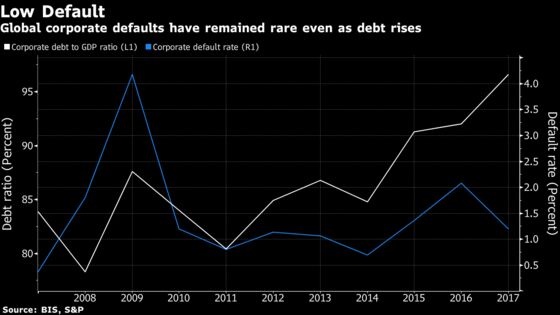

(Bloomberg) -- Amid rising rates, ballooning debt levels and widening spreads there’s one statistic that gives comfort to credit investors: default rates.

Insulated by cheap money from the QE era and bolstered by cash on their balance sheets, it remains rare for companies in Europe and the U.S. to miss debt payments. Among higher-risk speculative-grade firms the default rate fell to 2.9 percent last quarter, and may drop further to 2.1 percent by year-end, according to Moody’s Investors Service. And only one investment-grade firm has defaulted since 2012, data from Standard & Poor’s Global Ratings show.

“Default rates are on the floor,” said Fraser Lundie, co-head of credit at Hermes Investment Management. “Fundamentals still broadly stack up.”

But default rates aren’t the only thing credit investors care about. Spreads have widened to levels not seen for more than a year as concerns grow of overheating in the U.S. market, trade disputes, rising rates, inflation and the end of the European Central Bank’s bond-buying program.

“It’s really been death by a thousand cuts this year,” said Eoin Walsh, portfolio manager at TwentyFour Asset Management, which oversees 13.5 billion pounds ($17.7 billion). “Many little factors are having an impact.”

Steady economic growth and pre-planning has let companies lock in low rates while central banks supported markets. And a ninth straight year of global economic growth is aiding earnings by encouraging consumer spending and business investment. The global economy may expand 3.9 percent in 2018, according to the International Monetary Fund. The U.S. and euro area may both expand more than 2 percent, it said.

Alongside the macro support, companies’ debt-servicing costs have also declined, aided by central-bank easing. Average coupons in both euro investment-grade and high-yield credit have fallen to record lows because companies have replaced old high-coupon debt with cheaper bonds.

Fragile Markets

Looking ahead, investors are bracing themselves for tougher conditions. North America is the area of greatest concern, according to a survey by the International Association of Credit Portfolio Managers, with 66% of respondents expecting defaults to climb over the next year. The group pointed to higher U.S. interest rates and inflation as driving factors.

The biggest impact of the imminent end of QE and rising rates in the U.S. is more fragile markets in Europe, leading to more caution about credit quality, analysts at Bank of America Merrill Lynch wrote in a client note. “The obvious consequences of this are soggy markets, higher new issue premiums, and less spread compression as ‘crowding’ into higher-beta parts of the market fades.”

The credit market may also be downplaying the potential impact of tariffs, analysts at UBS Group AG wrote in a July 24 report. They say investors should be cautious about sectors including tech, industrials, metals and mining. Higher corporate leverage may also lead to an increase in stress among non-cyclical industries such as consumer staples and healthcare, the analysts including Bhanu Baweja wrote.

The end of loose monetary policies may also boost defaults in emerging markets next year, according to Abdul Kadir Hussain, the head of fixed income at Arqaam Capital, a Dubai-based investment bank.

Cheap Debt

Still, even companies with recent troubles are able to raise relatively cheap debt. Phone and cable company Altice Europe NV expanded a euro and dollar bond sale to $2.9 billion earlier this month, extending the maturity of its borrowings, less than a year after investors were dumping its bonds and stock amid concerns about debt levels.

Corporate borrowers can also use cashpiles built up during years of super-low rates to ride out any looming credit squeeze. Those bulging cash holdings are one reason why euro investment-grade corporate bond sales have tumbled about 27 percent this year, even with European borrowing costs still only at about 1 percent.

“Corporates have had it so good for so long, they’re exhausted,” Suki Mann, founder of creditmarketdaily.com wrote in a client note. “They’re also hoarding copious levels of balance sheet liquidity and know that they can still print if need be -- and at still close to historically low funding levels.”

--With assistance from Emma Haslett.

To contact the reporter on this story: Tasos Vossos in London at tvossos@bloomberg.net

To contact the editors responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net, Neil Denslow

©2018 Bloomberg L.P.