The U.S. Economy Deserves a Lot More Credit

The U.S. Economy Deserves a Lot More Credit

(Bloomberg Opinion) -- The U.S. economy is rolling along with far better prospects for solid growth than is widely realized, despite the many distractions that abound. This suggests that the path of least resistance for the equity market is higher, even if the rise is punctuated by occasional downdrafts instigated by new political, trade or other developments. For the same reasons, interest rates are likely to work their way higher and the yield curve will continue to flatten, which shouldn’t be troubling.

Disappointing economic reports pop up all the time, such as the modest gain in first-quarter gross domestic product. But that was neither unusual nor significant. The median estimate of economists surveyed by Bloomberg is for the government to say Friday that GDP rebounded to a 4 percent rate last quarter, the fastest since 2014, on the back of strong hiring trends, consumer spending, capital goods orders and numerous other items.

These positive reports were presaged by another more forward-looking statistic on job openings that points to continued solid growth for as far ahead as we can reasonably see, which, admittedly, isn’t overly far. In fact, the Fed could determine that it needs to raise rates faster and higher than it currently projects if the data continues on its recent tear, especially in terms of the labor market.

Fed Chairman Jerome Powell suggested last week that the Fed would continue to raise policy rates gradually “for now.” Some interpreted that to suggest it might need to stop boosting rates in the near future. Perhaps. But if inflation accelerates, the Fed might quickly conclude it must step up the pace and magnitude of rate hikes to prevent faster inflation from becoming entrenched in the economy.

Like all economic statistics, monthly employment reports are subject to the normal ebbs and flows of data volatility, because the economy doesn’t grow in a straight line and estimates can be inaccurate. Hiring each month is based on randomized surveys that can vary widely from the underlying trend for one, two or even three months. Such volatility is subject to revision, but the corrective adjustments may come many months or even a full year later. It is dangerous to take each month’s data as gospel, especially when other data suggest otherwise.

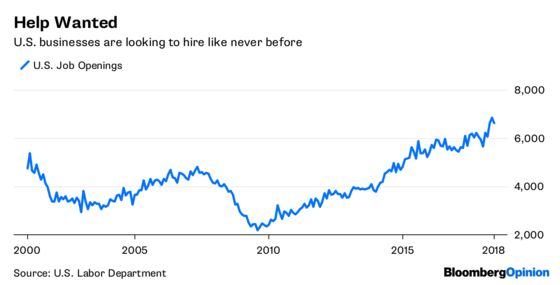

It is appropriate to suspect the expansion is on sound footing when firms are reporting rising — and record — levels of job openings, as measured by the Labor Department’s Job Openings and Labor Turnover Survey, otherwise known as the JOLTS report. Job openings data have only been available since 2001, but they are already an invaluable aid to understanding how the economy is performing. According to the most recent data, we now have more job openings, 6.6 million, than the 6.56 million reported to be unemployed. Moreover, job openings are still trending higher, a clear indication that firms are trying to hire, even if the monthly employment report suggests they aren’t finding the workers they need and the pool of unemployed keeps shrinking.

The consequences of the opposing trends in job openings and people looking for work are straightforward. As long as firms need to fill a growing number of positions, either they will succeed with positive consequences for economic growth, or they will fail, with ever greater upward pressure on labor costs and inflation. Most likely, the outcome will be some mix of the two possibilities, but only initially. Eventually, as job openings continue to grow but remain unfilled, it may become ever harder to reduce unemployment, even as efforts to hire exert greater upward pressure on inflation. The rubber band can only be stretched so far.

Some consideration has been given to the possibility that the Phillips curve must be dead, since the labor market has clearly tightened without a surge in employment costs. But the Phillips curve does not project rising labor cost pressures until unemployment declined meaningfully below the “natural rate.” However, the natural rate is not fixed. It may well have fallen over the past decade, reflecting changes in demographics and other economic variables.

In fact, after oscillating around 2 percent on a year-over-year basis from 2012 through 2014, average hourly earnings started a slow ramp beginning in early 2015, reaching 2.7 percent in June 2018. This increase occurred despite a strong headwind coming from most of the hiring being of the less-educated, lower-skilled, and therefore, lower-wage jobs pulling down the averages. The quarterly Employment Cost Index, which attempts to adjust for changes in the employment mix of workers, has accelerated from around 2 percent in 2010 to 3.2 percent most recently.

There is currently a higher level of uncertainty because of conflicts over trade policy and assorted other contentious international and domestic issues. Even so, forward-looking indicators, such as the JOLTS report, suggest that the economy remains on a solid trajectory that will continue the key trends of declining unemployment and rising labor costs, reflecting the growing scarcity of labor. Until these trends change, the expansion will continue.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Charles Lieberman is chief investment officer and founding member at Advisors Capital Management LLC. He may have a stake in the areas he writes about.

©2018 Bloomberg L.P.