GE Investors Deserve More Straight Talk

GE Investors Deserve More Straight Talk

(Bloomberg Opinion) -- If it's really out with the old at John Flannery's GE, then its arcane and vague approach to reporting earnings needs to go.

Flannery has rolled out a bold transformation plan to shrink General Electric Co.'s eight major business units to four and vanquish the bureaucracy that's been stifling the 126-year-old conglomerate. Many assumed this refresh would include a shift to reporting earnings per share on a GAAP basis, or something close to it, but Flannery's purportedly improved method of reporting GE's profit is just as disjointed as that of his predecessors. A bundle of puts and takes tends to make GE's profit look better than underlying fundamentals would suggest, with Friday's second-quarter report being the perfect example.

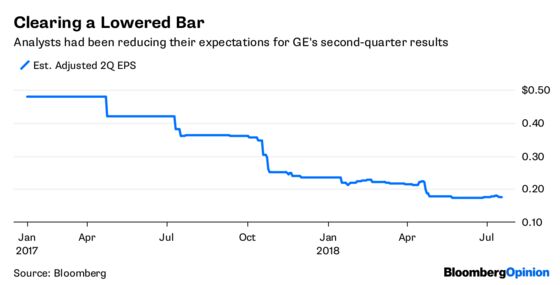

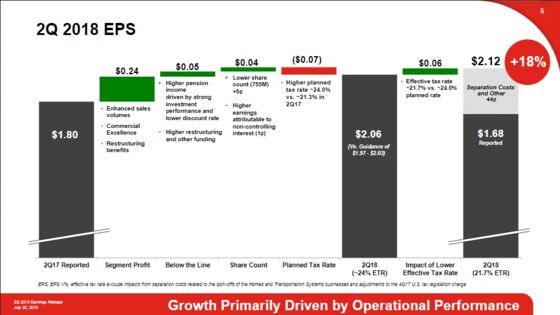

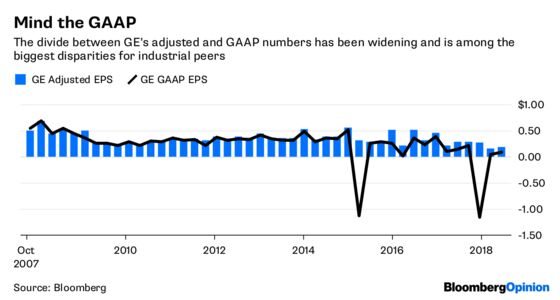

GE reported 19 cents in adjusted EPS, about a penny ahead of analysts' estimates. Even if you take GE's earnings definition at face value, this was still a beat in optical terms only. For one thing, those estimates had been coming down. And the edge was lower-quality, with analysts crediting tax benefits, lower corporate expenses and a-smaller-than-expected loss at GE Capital. Then consider that GE's adjusted second-quarter EPS is nearly 140 percent higher than the 8 cents it earned on a GAAP basis. Last quarter the gap was 300 percent.

Not all adjustments are bad: Honeywell International Inc. also reported second-quarter earnings on Friday and gave an adjusted EPS number that was 26 percent higher than the comparable GAAP metric. But Honeywell's divide largely came from backing out costs tied to the planned separation of its consumer-facing building-technologies business and its turbochargers unit. That makes sense. It's not going to do those spinoffs again next year. GE, on the other hand, backs out things like restructuring and non-operating pension costs in a manner that’s inconsistent with industrial peers. There is a good argument to be made that restructuring is an annual thing for GE, not a one-time event that temporarily clouds investors' ability to assess the underlying business.

For example, on the conference call, Flannery said an ongoing slump at the power division would likely drive the company to cut out more costs and further restructure the manufacturing footprint. So far, it's outlined $2 billion of structural cost cuts this year ($1 billion of which are in power) and a $500 million whack to corporate expenses through 2020. If there are challenges in other parts of the business, "we just have to do more," Flannery said. "The cost-out initiatives will never end." If they never end, then perhaps the associated restructuring charges should be reflected in GE's earnings.

GE does include operating pension costs in its earnings numbers, but that number doesn't reflect expenses for legacy plans that GE is still very much on the hook for in most cases, notes JPMorgan Chase & Co. analyst Steve Tusa. Following the release of the first-quarter regulatory filing, he highlighted definition-based accounting changes on pension that appear to flatter GE earnings. This is far too complicated to be beneficial for investors.

The mismatch between GE-defined earnings and reality was laid bare when the company cut its cash-flow guidance on Friday and yet maintained its adjusted EPS outlook. In what world does that make sense? Per management commentary, demand for power equipment continues to deteriorate relative to initial forecasts and it has limited visibility on the closing of orders. Meanwhile, margins at the powerhouse aviation unit showed uncharacteristic cracks and RBC analyst Deane Dray flagged a risk that GE Capital earnings may fall below the previously highlighted breakeven threshold. Tariffs pose an additional threat to profits. But magically, GE is still on track to hit the low end of its $1 to $1.07 range.

I have long argued that GE's earnings guidance was overly optimistic. The fact that GE didn't roll it back in the second quarter suggests that the bevvy of adjustments give the company enough wiggle room to still pull it off even as the underlying business falters. Either that or Flannery just didn't want to have that headline out there so soon after the big unveil of his breakup plan.

Whatever the reason, sticking with this chimerical definition undermines the thrust of a transformation that I really do believe just might work. Flannery got asked about GE's earnings adjustments on the conference call and promised an update later this year. Part of me fears GE will use a shift to GAAP reporting to provide cover for a guidance cut. But given that no one views that outlook as credible anyway, greater transparency will likely be welcomed.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.