Long End No Oasis Despite Flattest Canada Curve in a Decade

Long End No Oasis Despite Flattest Canada Curve in a Decade

(Bloomberg) -- If there ever was a time for corporate Canada to be more adventurous in the bond market, it’s now.

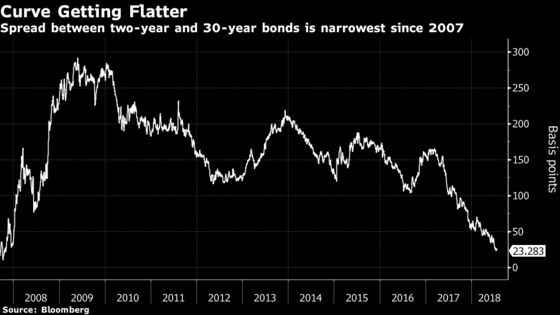

Yields on 30-year government debt have plunged to more than a decade-low relative to the short end in the wake of the Bank of Canada’s latest interest rate hike. That means there’s plenty of opportunity for issuers to lock in low borrowing costs for longer, especially since demand for long-term debt is “absolutely huge,” as central bank Governor Stephen Poloz said last week.

Yet corporate issuance of long-term bonds is lower this year than in 2017, even though the spread between two-year and 30-year bonds was more than 75 basis points wider a year ago and bond sales across all maturities are heading for a record this year.

“There is an old expression: ‘Feed the ducks when they are quacking,”’ said Jeff Herold, who oversees C$2 billion ($1.52 billion) as chief executive officer of Toronto-based J. Zechner Associates.

Two-year government bonds yielded about 1.94 percent on Thursday, while 30-years traded about 2.17 percent, leaving the difference between the two at 23 basis points. That matches a decade low reached last week after the Bank of Canada raised its benchmark interest rate to 1.5 percent.

Banks, Autos

At this time last year, when the central bank was only starting to tighten monetary policy, the spread was more than 100 basis points. While yields on Canada’s 30-year bonds fell eight basis points in the past 12 months, two-year yields have risen 69 basis points, increasing the relative attractiveness of longer bonds from the issuer’s perspective.

“In spite of a flatter yield curve, we have not experienced an increase in corporate issuance at the longer end in Canada,” said Marc St-Onge, managing director and global head of debt capital markets at Canadian Imperial Bank of Commerce. “We expect to see more domestic corporate issuance in the long end as conditions remain favorable.”

CIBC was the sole lead on Canada’s largest 30-year corporate bond this year, C$800 million of securities issued by TransCanada Corp. in June. But issuance of bonds of 30 years or longer has totaled C$4.6 billion this year, compared with C$5.9 billion in the same period a year ago, according to data compiled by Bloomberg.

Total corporate bond issuance is at C$67.2 billion year-to-date, the highest since at least 2007 when Bloomberg started tracking the data, and on course to beat last year’s record of almost C$110 billion for the full year.

Speculation is brewing investors’ obsession with corporate debt is reaching an end game after years of heavy issuance. The average spread between Canadian corporate debt and its government benchmark reached 115 basis points on Wednesday, the highest in more than a year, according to a Bloomberg Barclays index. Corporate bonds have returned just 0.7 percent this year, on track for the worst return since 2008, though bonds maturing in 10 years and longer have outperformed the return of the broader market.

CIBC’s St-Onge attributes the drop in long-term supply to more bond transactions from the automobile sector and banks, which traditionally finance themselves in the shorter parts of the curve.

Yet demand is there for the taking. Pension funds and other asset managers are buying up long-term bonds in oversubscribed deals as trade tensions make equities more risky, Poloz said last week, after raising interest rates by 25 basis points for the fourth time in the past year.

To contact the reporter on this story: Maciej Onoszko in Toronto at monoszko@bloomberg.net

To contact the editors responsible for this story: Jacqueline Thorpe at jthorpe23@bloomberg.net, ;Christopher DeReza at cdereza1@bloomberg.net, Christopher Maloney

©2018 Bloomberg L.P.