The Global Credit Market Has Good News About the U.S. Economy

Global debt markets are flashing a bullish signal on America’s economic trajectory.

(Bloomberg) -- Global debt markets are flashing a bullish signal on America’s economic trajectory, leaving Europe and emerging markets in the dust.

Money managers in America Inc. debt are shrugging off late-cycle angst and the trade-war fallout thanks to an upswing in earnings -- while the rest of the world struggles for traction.

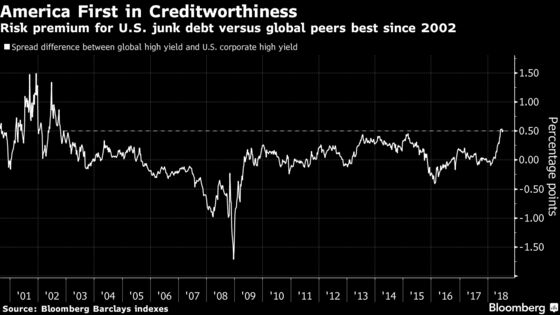

The premium to hold high-yield dollar bonds around the globe versus U.S.-listed corporate peers has widened to levels last notched back in 2002, according to data compiled by Bloomberg. In other words, rarely has U.S. debt looked in such good shape relative to peers in the $2.4 trillion market.

“I think this tells us that the U.S. economy is in better shape, that default risks are low still and that refinancing risks are comfortable,” despite Federal Reserve interest-rate increases, said Chris Iggo, chief investment officer for fixed income at AXA Investment Managers.

The rising premium for global debt over U.S. counterparts is the latest sign of America’s economic divergence, along with soaring short-term Treasury yields, dollar strength and corporate profit growth.

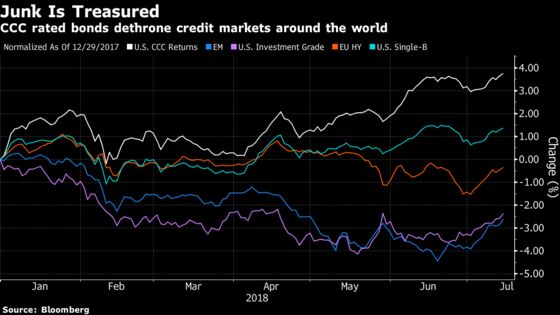

Spreads for the lowest-rated U.S. high-yield bonds fell to a four-year low last week to become one of the best-performing segments in the global credit landscape so far this year.

“The key reason why U.S. high yield is diverging from the rest of the world is that the U.S. economy is accelerating while the ROW economy is decelerating,” said Srinivas Thiruvadanthai, research director at the Jerome Levy Forecasting Center.

It all constitutes a shift in the global credit cycle from just two years ago, when a revival of the growth story in the euro area and developing economies began to curb spreads relative to U.S. peers. Today, the earnings cycle is boosting the health of American companies’ balance sheets, even as outflows hit the asset class.

All-in yields for U.S. junk have remained relatively stable since February’s tumult in risk assets, after which the Fed has delivered two rate hikes. Junk bonds are seen as more likely to hold their value in a rising rate environment because of their lower relative duration risk.

Policy normalization by the U.S. central bank is a testament to the continued strength of the domestic economy, with a rising risk-free rate helping to cap premiums for U.S. lower-rated issuers. Over the same stretch, all-in yields for global junk debt in dollars have risen by 50 basis points.

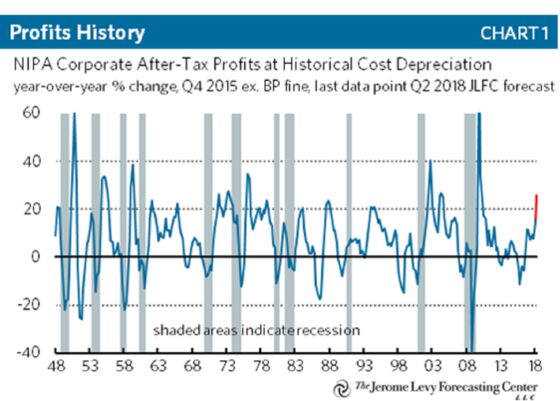

One measure of corporate profits that best tracks operating margins for S&P 500 companies suggests U.S. earnings are in the midst of “an unprecedented acceleration this late in the cycle,” according to Thiruvadanthai.

“Better earnings mean improvement in interest-coverage and debt-service ratios. Little wonder that U.S. high yield is performing well,” said the analyst.

U.S. Outperforms

The U.S. tax overhaul may offer further ballast for junk-debt investors, by curbing the deductibility of interest expenses, which increases the incentive for companies to delever.

“High-yield investors are also turning more positive on the impact of tax reform, with a higher share now expecting leverage to decline,” Hans Mikkelsen, Bank of America’s head of U.S. high grade credit strategy, wrote in a note.

With a net 11 percent projecting weaker balance sheets over the next six months, money managers hold “strikingly optimistic assessments of fundamentals given the late stage of the credit cycle,” he said.

There’s a contrarian signal here too. U.S. speculative-grade bonds haven’t priced in external risks like trade frictions, while emerging-market bond prices are looking more attractive.

“If there is good news on trade there could be a strong risk rally and the higher beta parts of that will be EM,” said Iggo.

All told, the relentless flattening of the Treasury curve is likely exaggerating near-term threats to the U.S. expansion, if credit markets are anything to go by.

And there’s a message for President Donald Trump in bond performance: domestic America can survive the brewing conflict in global commerce.

Inward-looking high-yield companies, at least, should escape without too much impact, said David Ader, chief macro strategist at Informa Financial Intelligence. “It actually is a comment -- dare I suggest -- that would make Trump smile as it implies how dependent the rest of the world is on the U.S.,” he said.

--With assistance from Gowri Gurumurthy.

To contact the reporters on this story: Sid Verma in London at sverma100@bloomberg.net;Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Cecile Gutscher

©2018 Bloomberg L.P.