Steinhoff Africa Seeks to Limit Pepkor Share Plan Damage

Steinhoff Africa Seeks to Limit Damage From Pepkor Share Plan

(Bloomberg) -- Steinhoff Africa Retail Ltd. will be advised by the end of next month how much it may need to pay to settle a controversial management-incentive plan devised by a company formerly owned by South African billionaire Christo Wiese.

The operator of clothing chains including Pep and Ackermans disappointed investors in May when it booked 500 million rand ($37 million) in charges related to the arrangement, a hangover from when the company was still part of scandal-hit retailer Steinhoff International Holdings NV. The plan was put together in 2011 by Wiese’s pan-African Pepkor Holdings Ltd., which was bought by Steinhoff in 2015 and now makes up the bulk of Steinhoff Africa.

STAR, as the company is also known, hired Cape Town-based law firm Bowmans to investigate to what extent the retailer is liable for the deal, which allowed 44 Pepkor managers to take out loans to invest in the business that were guaranteed by the company. It expects to receive the findings in six weeks at the latest, according to Chairman Jayendra Naidoo.

Mitigate Risks

“So far, we’re just saying there’s a risk and we’ve taken a provision,” Naidoo said by phone. “Our stance is clear: to recover the loans and find a sensible way to mitigate the risks. We are mindful of the fact that not everybody is in a position to afford to pay those loans.”

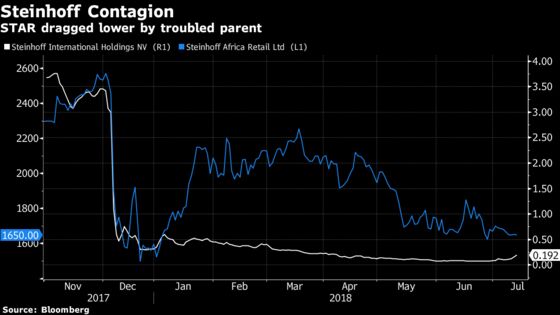

The potential writedown is among the latest challenges for STAR in what’s been an eventful first 10 months as a listed company. The stock plunged when Steinhoff, which holds a 71 percent stake, reported a hole in its accounts in December, even though STAR’s own financials were given the all-clear. More recently, investor confidence has been eroded by an unseemly spat between STAR management and the founders of Tekkie Town, a South African shoe chain that Steinhoff bought two years ago.

STAR shares rose 0.9 percent to 16.64 rand at the close in Johannesburg on Friday, paring its decline since the Steinhoff financial crisis erupted to 32 percent.

Pepkor’s incentive plan was conceived because, as a closely held business, its executives couldn’t buy shares on the open market and therefore couldn’t participate in the growth of the retailer. To resolve the matter, a company called Business Ventures Investments 1499 was formed in which managers could invest, and that in turn bought a stake in Pepkor.

Some managers bought into BVI with their own money, while others took loans from Pepkor’s finance arm and FirstRand Ltd.’s Rand Merchant Bank. The RMB debt was guaranteed by Pepkor.

‘First Prize’

Wiese, 76, stands by the thinking behind the plan even though he is no longer involved with STAR.

“For me, first prize is to have top executives exposed as much as possible to the fortunes of the company,” Wiese said by phone. “It makes me relaxed that my management and my shareholders are on the same side of the fence. We swim together, we sink together.”’

When Steinhoff bought Pepkor it also acquired the clothing retailer’s liabilities, including the management-incentives loan guarantee. The Pepkor shares that BVI had accumulated were converted into Steinhoff shares, which subsequently crashed when the accounting scandal erupted late last year. That meant some managers wouldn’t be able to use the stock to pay back the loans, triggering the guarantees now held by STAR.

The structure of the deal amounts to “gambling with shareholder money,” said Theo Botha, a STAR investor and corporate-governance activist. Furthermore, stockholders weren’t informed of the risk in a timely manner, he added. With BVI holding 43.2 million shares in Steinhoff and BVI’s outstanding debt to the bank being about 440 million rand, by mid-December the loan was no longer covered by Steinhoff shares, which were trading below 10 rand a piece.

Why the BVI guarantee was not disclosed sooner and why the Steinhoff shares were not converted into STAR stock are “fair questions” that are being looked into, Naidoo said. He added that since December STAR has been trying to clear the bigger problems created by its close link to Steinhoff, such as refinancing loans owed to the parent in order to be financially independent, and only recently started looking at secondary issues.

“There was very little disclosure, if any,” Botha said. “Why should we pick up this bill on a new company? The executive management must bail themselves out.”

To contact the reporter on this story: Janice Kew in Johannesburg at jkew4@bloomberg.net

To contact the editors responsible for this story: Eric Pfanner at epfanner1@bloomberg.net, ;Antony Sguazzin at asguazzin@bloomberg.net, John Bowker, John J. Edwards III

©2018 Bloomberg L.P.