Bank Stocks Sink as Earnings Hurt by Loan Woes, Fed Punishment

Loan Woes and Fed Punishment Hurt Bank Earnings, Sinking Stocks

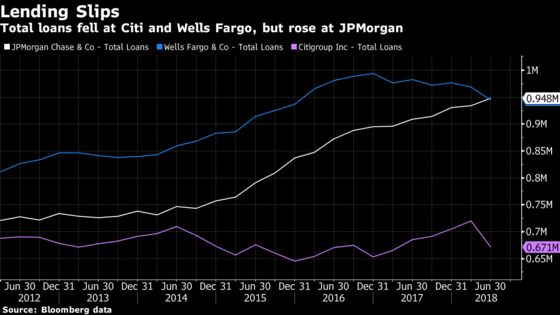

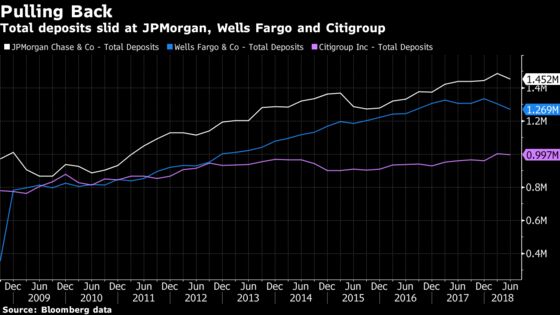

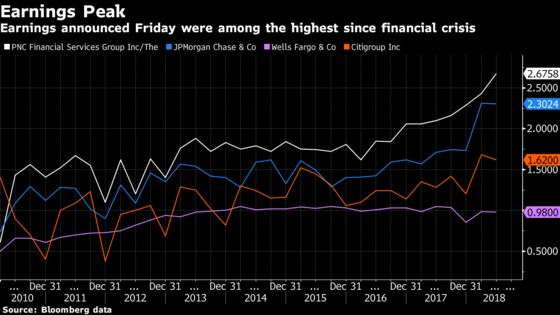

(Bloomberg) -- U.S. bank stocks are hurting after disappointing second-quarter results from Wells Fargo and Citigroup, and as JPMorgan’s earnings beat wasn’t enough to boost investor confidence. Analysts are zeroing in on sliding loans and deposits, while Wells Fargo was also hurt by the Federal Reserve’s asset cap.

The KBW bank index is down as much as 1.9 percent, the most intraday since June 25, led by a decline of as much as 3.3 percent in Citigroup, the most since May 29, and a slide of as much as 4.3 percent in Wells Fargo, the most since March 22. JPMorgan was little changed after dropping as much as 1.6 percent. Bank of America and Goldman Sachs -- which report next week -- are also down.

“JPMorgan had a solid quarter, as expected, though investors may have wanted more from the bank, and its peers, to support a strong rally from here,” Bloomberg Intelligence analyst Alison Williams says.

Here’s a sample of analyst commentary:

On JPMorgan’s results:

Goldman, Richard Ramsden

JPMorgan’s quarter was “good enough on strong capital markets and credit,” analyst Ramsden writes. Net interest income and net interest margin both missed expectations, likely due to higher liability costs driven by higher long-term debt yields, though deposit costs increased only 10 basis points.

Loan growth of 4 percent was in line with expectations and Goldman’s 2018 forecast for 4 percent loan growth, and was below management guidance of about 6 percent, as industry volumes have fallen. “As with other banks reporting thus far this quarter, credit concerns remain a non-event.”

Morgan Stanley, Betsy Graseck

JPMorgan had a “strong quarter,” with a beat on trading. CEO Jamie Dimon’s comments in the earnings statement “suggest a solid environment both in the U.S. and internationally, in contrast to recent investor sentiment.” The results have positive read-across for other investment banks and for super-regional bank loan growth, but are in-line for trust banks and cards and are negative for mortgages.

Evercore ISI, Glenn Schorr

The quarter hit on the “familiar JPM themes” of good organic growth and interest income, alongside tame credit and great capital return. Still, the report showed a hit to card interchange income and lower mortgage income.

“This should be a positive start to bank earnings after a tough couple of months for the stocks as people fear potential implications of the flatter curve, but note that eyes will also be on expenses, deposit and loan betas, and competition/loan growth rolling forward.”

Keefe, Bruyette & Woods, Brian Kleinhanzl

“Overall, results were above our expectations and the only area that missed was the tax rate,” with strength seen in trading, investment banking and average loan growth.

“Expectations were high and JPM managed to beat high expectations but a margin miss tempers the upside today.”

Oppenheimer, Chris Kotowski

“Versus our expectations, pre-provision earnings were slightly lower than expected,” at $12 billion versus an estimated $12.1 billion. However, that was “more than offset by a somewhat lower loan loss provision,” $1.2 billion versus an estimated $1.5 billion.

“When you look at the year-on-year comparisons, everything looks excellent,” with loans and interest income rising. “Despite all the bears’ hand-wringing about rising deposit betas, the benefit of rising rates is clear.”

On Citigroup’s results:

Morgan Stanley, Betsy Graseck

Citigroup’s EPS beat on provisions, while revenue missed, with debt underwriting, trading and other revenues all weaker. Within trading, FICC declined 6 percent versus the prior year, versus Morgan Stanley’s estimate of a 5 percent drop.

“Stock reaction (down 2.7 percent this morning) seems overdone, especially given miss was on lower multiple capital markets related revenue.”

Atlantic Equities, John Heagerty

“The numbers were reassuring without being spectacular. ... Overall, both revenues and costs were in line with consensus. The beat was primarily driven by lower provisions and a 1pp lower tax rate.”

Heagerty noted that while credit-card revenue only grew 1 percent from the prior year, the important point is that credit quality is still solid and net income in the Global Consumer Banking segment climbed 14 percent.

Evercore ISI, Glenn Schorr

Overall, Citigroup reported a “pretty decent quarter” that felt like a “1-nil win.” Schorr highlighted solid growth in loans and the North American consumer segment, better profitability, improvement in Mexico, a lower share count, and continued expense control. Issues included flat consumer banking deposits, flat cards revenue, and higher North America consumer credit costs.

“Expenses were flat, tax rates are lower and shares are down a whopping 8 percent vs last year so Citi looks on track to hit their targets as earnings are ramping double-digits.” While revenue and loan growth “isn’t huge” at about 3 percent, “it is pretty broad based across regions and products and we’re seeing momentum in accrual type businesses like TTS and the Private Bank.” Schorr adds that “equities flexed its muscles again on better engagement with investor clients.”

On Wells Fargo’s results:

Morgan Stanley, Betsy Graseck

The Fed’s consent order puts “a drag on results,” Graseck writes in a note. Average loan balances fell 0.7 percent in quarter versus Graseck’s forecast of 0.1 percent growth. Graseck also flags weaker mortgage fee income, higher deposit betas and better credit.

Goldman, Richard Ramsden

“A noisy quarter, but improving NII trends drive a core beat.” Goldman remains “positive around the forward trajectory for earnings,” given flat cumulative deposit betas, with quarterly outperformance versus peers; securities yield of 3.28 percent, up 12 basis points from last year, even with hit from tax overhaul on FTE muni NII; and, a “much larger-than-expected capital return announcement post-2018 CCAR.”

Sandler O’Neill, R. Scott Siefer

Wells Fargo’s core EPS trailed estimates, with misses on fees for mortgages and expenses. Negatives include average loans dropping 2.9 percent in the quarter, versus and expectation of “flattish,” and higher-than-expected expenses. Siefer sees the firm’s higher net interest margin as a positive, and says credit trends “were very strong.”

“As long as some of these elevated costs indeed prove transitory (which would allow the company to meet its cost targets), there should be further opportunity for costs to come out of the system” Siefer writes. “We do not believe the trends are anywhere near as bad” as this quarter’s 98 cents per share “headline would imply. So we could see the shares clawing back from some opening weakness.”

Piper, Kevin Barker

Wells Fargo’s quarter showed “lots of noise, but appears to be a slight operating beat,” after adjustments. “All things considered, we thought the quarter was decent given NIM showed significant expansion and operating expenses were better. We note fee income was weak across most line items.”

--With assistance from Joelle Kruczek and Gilbert Xu.

To contact the reporters on this story: Felice Maranz in New York at fmaranz@bloomberg.net;Lily Katz in New York at lkatz31@bloomberg.net;Austin Weinstein in New York at aweinstein18@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Dave Liedtka, Richard Richtmyer

©2018 Bloomberg L.P.