Americans Are Back in Asia Dollar Bond Market as Locals Struggle

Americans Are Back in Asia Bond Market as Locals Struggle

(Bloomberg) -- Asian borrowers battling to refinance their bonds amid the emerging-market slump are finding support from a block of investors that until recently were almost in danger of getting sidelined -- Americans.

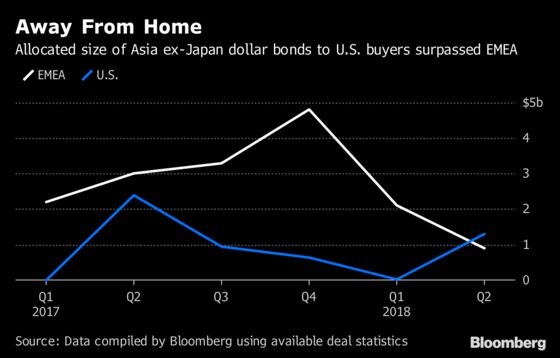

While Asians and Europeans are scaling back their purchases, Americans are the one group opening wallets wider. For example, they bought $1.3 billion of Chinese dollar bonds last quarter, up from just $23 million the previous three months. EMEA areas took less than $1 billion after $2 billion, while Asia-Pacific buyers were at $10 billion, versus $15.5 billion, according to issuance data compiled by Bloomberg where allocations were available.

Underwriters are urging issuers to take full advantage of the apparent American appetite in a market that last year saw record issuance thanks to frenzied demand from Chinese investors in particular. Banks are encouraging borrowers to look again at so-called 144A sales targeted to the U.S., compared with the Regulation S securities directed outside it.

“The recent sell-offs, and reduced Asian investor appetite for dollar bonds, should prompt issuers from the region to reconsider potential issuance in the 144A format,” said Howard Chu, head of Asia-Pacific syndicate at JPMorgan Chase & Co.

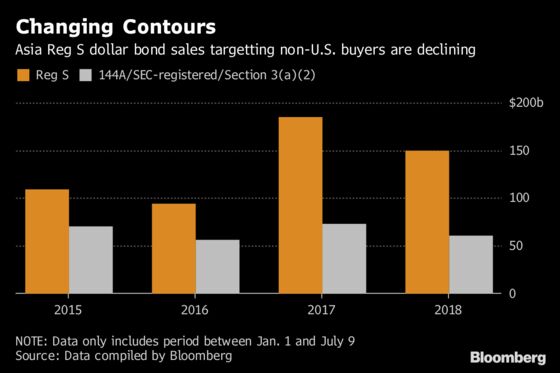

Asian dollar-bond sales in the Reg S format -- which require less stringent accounting guidelines than 144A -- have slowed to $150 billion from $185 billion the same period a year earlier. In comparison, issuance volume via the 144A route is at around $43.5 billion, data compiled by Bloomberg show.

“144A distribution offers Asian issuers access to deep pools of real money liquidity, from large institutional investors that are permanently committed to their investment markets,” said Ernst Grabowski, head of debt syndicate for Asia Pacific at Morgan Stanley.

A year ago, the market had a different narrative -- that funds outside the region might be more skittish when global conditions got rough and interest rates rose in their home bases. On the flip side, Asian buyers were seen as a more stable source of demand, with funds also more familiar with the companies selling debt. Issuance became so focused on the region that some underwriters found themselves making few trips to the U.S. any more.

Matt Brill, head of U.S. investment grade credit and senior portfolio manager at Invesco Ltd, said Chinese issuers are drumming up interest in the U.S. but the trade war could limit demand. Invesco would be looking to add names like Alibaba Group Holdings Ltd., Baidu Inc and Tencent Holdings Ltd. to its portfolio on expectations that they could be less affected by a potential trade war.

And the 144A route isn’t for everybody, given the more onerous accounting requirements. Bigger companies, such as state-owned enterprises, tend to fare better with name recognition. The budding U.S.-China trade war also could cast a cloud over some borrowers. For others, the appetite for securities from what’s still the fastest-growing region of the world could be a rich vein to tap.

“We have seen consistent demand out of the U.S. for Korean and Chinese SOE names,” said James Arnold, head of Asia Pacific debt capital markets syndicate at Citigroup Inc. in Hong Kong. “Additionally, the demand for Hong Kong corporates and the higher-quality Indian and Indonesian issuers has been consistent over recent years.” For companies with stronger credit profiles, these trends should continue, he said.

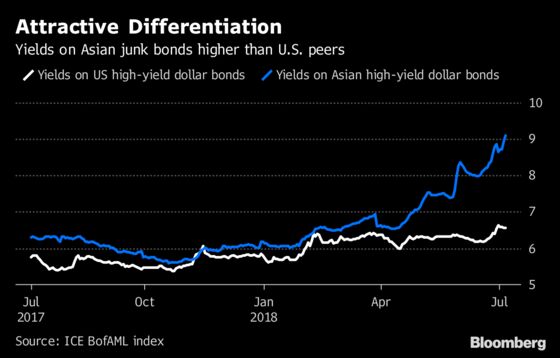

Weaker credits might still have something going for them: their yields are now getting more attractive than those available on U.S. junk-rated debt.

“U.S. investors haven’t had the opportunity” to take advantage of higher-yielding Asian dollar bonds, because most issuance has been Reg S, said Chu at JPMorgan. For “benchmark high yield names” it’s a good time to look at the U.S., he said.

--With assistance from Vildana Hajric.

To contact the reporters on this story: Carrie Hong in Hong Kong at chong61@bloomberg.net;Annie Lee in Hong Kong at olee42@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Chan Tien Hin, Christopher Anstey

©2018 Bloomberg L.P.