Fed Could Avert an Inverted Yield Curve. But It Won’t.

Fed Could Avert an Inverted Yield Curve. But It Won’t.

(Bloomberg Opinion) -- Listen to Federal Reserve Chairman Jerome Powell talk about the U.S. yield curve, and you’d come away thinking the leader of the world’s most influential central bank is powerless when it comes to stubbornly low long-term interest rates.

That’s not entirely correct.

It’s true that the Fed’s interest-rate hikes primarily boost short-term Treasury yields, while longer-term debt is more sensitive to bond traders’ outlook for growth and inflation. That’s the reason an inverted curve is such a reliable indicator of an impending recession — as officials increasingly tighten policy, the outlook for the economy grows dimmer. In a sense, there’s only so much the Fed can do to lift 10- and 30-year yields.

But it could certainly be doing more than it is now, if policy makers were truly trying to avoid an inverted yield curve.

It comes down to the central bank’s other monetary policy tool: its balance sheet. Part of the Fed’s normalization process involves letting its debt holdings mature and only reinvesting the proceeds if they exceed monthly caps, currently at $24 billion for Treasuries and $16 billion for mortgage-backed securities. Some investors have speculated that this runoff would reintroduce term premium into the market. That’s not happening.

Why not? Well, for one thing, the Fed is still buying a good chunk of Treasuries. In May, it gobbled up $4.1 billion of 30-year bonds, or about 20 percent of the $21.1 billion total issued by the Treasury. The auction size only gets reported as $17 billion, in fact, because that’s the amount that goes to non-Fed investors. Around the same time, it added more than $6 billion of 10-year notes, while $25 billion went elsewhere.

Imagine if asset managers, foreign investors, individuals, pension funds and primary dealers had to absorb that much more long-duration debt. They’d certainly demand a larger premium, which would steepen the yield curve and swiftly solve Powell’s conundrum.

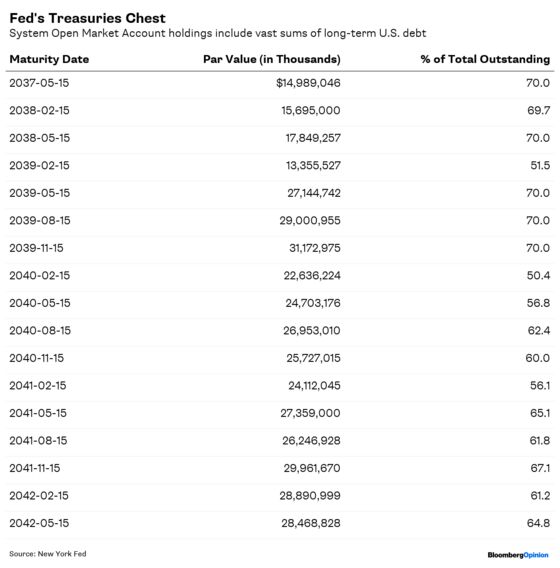

And it’s not just new purchases. Take a look through the Fed’s holdings, and you’ll see that the central bank holds more than half (and as much as 70 percent) of some Treasury bonds that mature from 2037 to 2042. That’s almost half a trillion dollars of firepower that officials are choosing not to deploy to steepen the yield curve. If they really wanted to, they could effectively carry out a reverse Operation Twist by selling those long bonds and purchasing shorter-dated maturities.

Indeed, with the story of global synchronized growth unraveling quickly, it’s little wonder benchmark 10-year Treasury yields remain locked near their 2018 average. The comparable yield on German bunds fell to an 11-month low in late May, and at 0.32 percent is still less than half of what it was in February.

Now, the movement in the bund market does little to guide the Fed in deciding whether to proceed with its path of rate hikes, which would virtually guarantee an inverted Treasury curve. The spread between 5- and 30-year U.S. yields fell below 20 basis points on Tuesday for the first time since July 2007. The segment from 2 to 10 years isn’t far behind.

In theory, this would be as good a time as any for the Fed to inject more long bonds into the hands of private investors. And yet it’s extraordinarily unlikely to do so. For one, officials could credibly argue that the U.S. Treasury is going to need to boost auction sizes even more in the months ahead to cover a widening federal budget deficit. That might be enough to elevate the term premium without the central bank tinkering with its long-term holdings.

But what’s more likely is the Fed is simply afraid of losing control. As Powell has said, the move higher in short-term rates makes perfect sense because central bankers effectively dictate those. But the fate of long-term yields is in the hands of bond traders. For all the talk of the Treasury term premium, it’s still ultimately an abstract figure derived from a model.

The only way to stop the flattening trend, in that case, is for the Fed to hit the brakes on raising short-term rates. But, as I wrote last week after the release of the central bank’s June meeting minutes, it doesn’t seem likely to do that, even with investors on edge.

That means even with the yield curve as close to zero as it’s been in a decade, it probably doesn’t pay for traders to fight the flattener.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.