Bond Traders Are Jittery, But Fed Shows No Fear

Bond Traders Are Jittery, But Fed Shows No Fear

(Bloomberg Opinion) -- If bond traders still questioned whether Jerome Powell’s Federal Reserve would truly stay the course, no matter how choppy the waters, minutes of the central bank’s June meeting should erase all doubt.

Fed officials said they realized the Treasury yield curve was rapidly heading toward inversion, according to the Federal Open Market Committee minutes released Thursday. Many saw downside risks from emerging markets, in part because of the tightening financial conditions in the U.S. They heard intensified concerns about tariffs and other trade restrictions, with some of their contacts indicating “that plans for capital spending had been scaled back or postponed as a result.”

And yet, no matter how strong the headwinds, it’s clearly full steam ahead for further rate increases. That’s a striking departure from as recently as 2016, when a few shocks left Janet Yellen’s Fed holding off on tightening policy again and again.

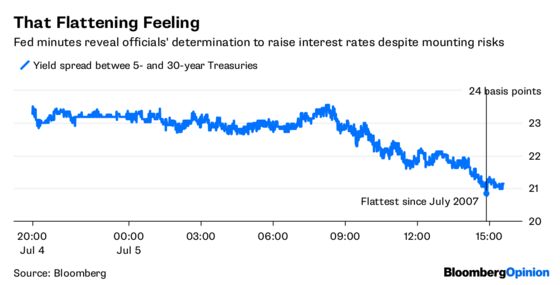

The Fed’s newfound resolve isn’t a complete shock to bond traders, given that the central bank’s projected path of increases nudged up last month. Still, the reaction in the Treasury market is telling. Namely, the yield curve continued to flatten, with the spread between five- and 30-year maturities narrowing to 21 basis points, the least in almost 11 years. While short-term yields are higher, the long-bond yields are the smallest since February. Traders have flocked to safety because of the same risks that the Fed is shrugging off.

The reaction of the 30-year bond should be a signal to Fed officials that their longer-term target for the fed funds rate, at just below 3 percent, is about right. They said “that it might soon be appropriate to modify the language in the postmeeting statement indicating that ‘the stance of monetary policy remains accommodative.’” With the yield curve where it is now, following through on just a couple more rate hikes would probably be enough to tip it below zero. That’s not normalizing — that’s tightening.

What’s more, Fed policy makers are uniform in their willingness to see this tightening cycle through without delay. Only a single participant (probably Neel Kashkari or another uber-dove) suggested slowing down, according to the minutes:

One participant remarked that, with inflation having run consistently below 2 percent in recent years and market-based measures of inflation compensation still low, postponing an increase in the target range for the federal funds rate would help push inflation expectations up to levels consistent with the Committee’s objective.

It’s true that market-based measures of inflation remain barely above 2 percent and down from their 2018 highs. But, again, it just doesn’t seem to matter for this Fed. Until the U.S. economy shows clear signs of faltering, no pause is coming. In the words of Barclays economists: “The Fed will only conclude that protectionism is a problem if and when employment slows or equity markets decline.” And even then, it’s an open question how severe the stock-market losses would have to be to force Powell to hit the brakes.

It’s a strange role reversal, with bond traders reacting cautiously to the latest headlines and economic data. The Fed, on the other hand, has a plan. And it’s certainly not going to allow some emerging-market turbulence or trade spats to get in the way.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.