Investment-Grade Bond Investors Brace for a Rising Tide of M&A

Investment-Grade Bond Investors Brace for a Rising Tide of M&A

(Bloomberg) -- The U.S. corporate bond market is bracing for a flood of supply from mergers and acquisitions in the second half of the year. Borrowers will have to pay up after a first-half deluge helped wreck spreads.

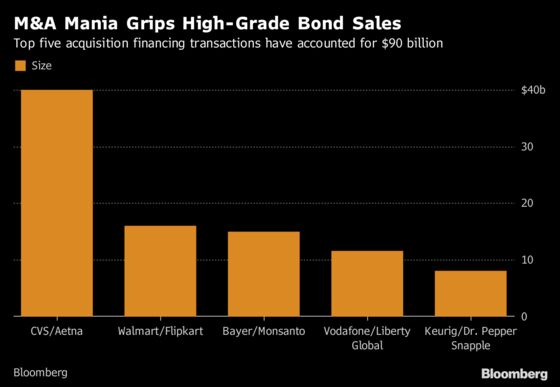

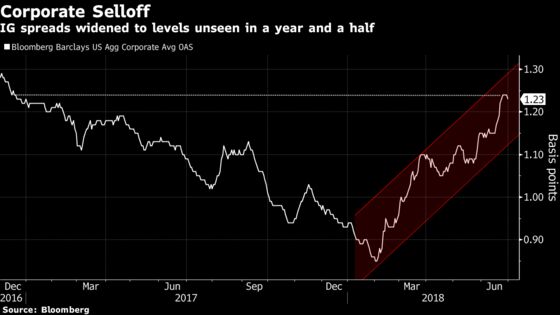

Sales of investment-grade bonds tied to M&A surged by 50 percent to $154 billion in the first half compared with the same period last year, driven by a slew of deals that included CVS Health Corp., Walmart Inc. and Bayer AG, according to data compiled by Bloomberg. That pickup in supply helped push spreads in the secondary market to the highest level in a year and a half.

The trend could continue for the next six months. There’s more than $1 trillion in pending M&A deals, according to Bloomberg Intelligence. Walt Disney Co. is said to be readying a $36 billion bridge loan to potentially buy Twenty-First Century Fox Inc. Conagra Brands Inc. agreed to buy Pinnacle Foods Inc., Microsoft Corp. is buying GitHub Inc., and the list goes on.

“There are some deals in the pipeline that people are watching very closely and that could certainly be impactful for the market,” said Jim Caron, a senior fixed-income portfolio manager at Morgan Stanley Investment Management. “Supply has been sort of the reason why spreads have been widening. That could be something that people get a little bit concerned about.”

Companies started showing more interest in M&A in June when AT&T won an antitrust ruling allowing the takeover of Time Warner Inc. Within a week, Bayer came forward with a $15 billion bond deal to finance its acquisition of Monsanto and two days later Walmart sold $16 billion to fund a stake in Flipkart. The supply helped boost the benchmark index of high-grade corporate bond spreads to the highest level since December 2016.

Even if more M&A adds to supply in the second half, there’s still a chance it won’t top the first half and add as much upward pressure on spreads.

There are several factors that make the investment-grade bond market attractive in the latter half of the year, said Krishna Memani, chief investment officer at OppenheimerFunds Inc. Spreads are “meaningfully higher,” companies will see the benefits of tax reform and the likelihood of Federal Reserve tightening may fade.

“Investment-grade spreads should be stable in worst case, tighten some in best case,” Memani said. “M&A is always a late cycle play, but it won’t be at the pace it has been of late.”

--With assistance from Brian Smith.

To contact the reporter on this story: Shelly Hagan in New York at shagan9@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Randall Jensen, Brendan Walsh

©2018 Bloomberg L.P.